Relative stabilisation: Ukraine’s economy on the threshold of the fifth year of war

Ukraine’s effective resistance to the Russian invasion over the past four years would not have been possible without a properly functioning economy. Despite the intensity of the ongoing war, the Ukrainian economy has performed surprisingly well. Since 2023, it has recorded modest economic growth, although it remains significantly below the pre-war level, following a contraction of nearly 30% in GDP in 2022. Inflation and the hryvnia exchange rate remain under control despite some volatility. The relative stability of public finances rests primarily on support from Western partners, particularly the EU, as well as international financial institutions. Between 2022 and 2025, these partners transferred $168 billion to the Ukrainian budget, covering almost all state expenditure unrelated to defence. Ukraine’s economy has adapted to wartime conditions. If external assistance continues, there are no grounds to anticipate a more severe crisis in the near term, although robust economic growth is also unlikely.

Macro level: stable stagnation

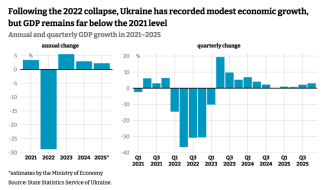

Ukraine’s economy remains far below its pre-invasion level. According to estimates by the Centre for Economic Strategy, in 2025 the country’s GDP was more than 20% lower than in 2021. Following the collapse triggered by Russia’s invasion in 2022, when GDP plunged by 28.8%, the economy began to recover.[1] The rebound in 2023 was relatively modest at 5.5% and growth slowed further in the following years. According to estimates by the Ministry of Economy, it reached 2.2% in 2025; however, this figure is likely to be overly optimistic. For example, assessments by the National Bank of Ukraine (NBU) suggest a slower pace of growth, at only 1.8%. On a quarterly basis, the largest increase was recorded in the fourth quarter of 2025 (+3%); however, this uptick was largely seasonal, resulting from an unusually late maize harvest.

Until the high-intensity phase of the war comes to an end, no significant improvement in the economic situation can be expected. Moreover, current forecasts may prove to be overly optimistic. Projections for 2026 are similar to last year’s performance. According to the NBU, the economy is expected to grow by 1.8%. The main constraint on growth is the electricity deficit caused by Russian strikes (see below), which continues to hinder business operations. Growth forecasts for the following years are only marginally more upbeat: 2.8% in 2027 and 3.7% in 2028. However, these figures can hardly be considered reliable, given the uncertainty surrounding the future trajectory of the war.

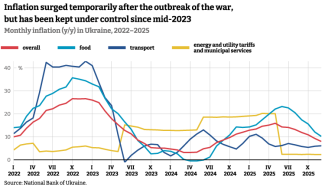

Following temporary price spikes in the initial months of Russia’s invasion, when annual inflation exceeded 26% at the end of 2022 and surpassed 30% for food, the situation began to stabilise from mid-2023. A brief surge in food prices in 2025 was offset by particularly strong vegetable harvests. From mid-year onwards, monthly inflation fell steadily, reaching 8% in December, a rate lower than that recorded prior to Russia’s invasion. The NBU expects inflation to fall further in 2026.

The industrial production index fell by 2.4% year-on-year in 2025, mainly due to disruptions to electricity supply in the autumn and labour shortages. The decline did not affect all sectors. For example, the production of fabricated metal products increased by 8.4%, while the production of pharmaceutical products soared by 18.9%. At the same time, output in the mining sector fell by 10.6%; in particular, hard coal production plunged by 31%. This was partly due to Russia’s occupation of mines near Pokrovsk and serious damage to thermal power plants reliant on coal as a fuel source.

By contrast, a significant increase was recorded in defence-related industrial production, particularly in the drone segment. According to data for the period from January to October,[2] its value exceeded 58 billion hryvnias ($1.3 billion), considerably higher than in 2024 (43 billion hryvnias) and 2023 (23.6 billion). Despite this growth, the unmanned aerial vehicle (UAV) production sector still plays a relatively minor role in the overall economy: in October 2025, it accounted for just 1.8% of total industrial output. By comparison, metallurgical production accounted for 11.4% of total industrial output, despite the loss of two major plants in Mariupol.

Foreign exchange market – the hryvnia exchange rate remains broadly stable

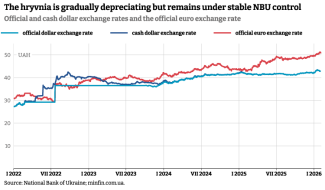

Following the outbreak of the war, the NBU temporarily introduced restrictions on the foreign exchange market, notably by fixing the hryvnia’s exchange rate against the dollar. However, it partially lifted this measure as early as October 2023, and the gap between the cash and official exchange rates has remained minimal ever since. The Ukrainian currency has gradually depreciated over this period. This trend has been less pronounced against the dollar, which weakened following Donald Trump’s return to office, but more evident against the euro, which has strengthened against the hryvnia to a record level.

The critical role of foreign financial support…

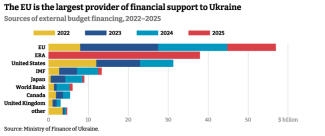

Maintaining Ukraine’s financial stability would not have been possible without assistance from Western countries and institutions. Since 2022, defence spending has accounted for more than half of total budget expenditure, effectively matching budget revenues, and has increased in value each year. These funds have financed, and to a large extent continue to support, the ongoing war effort. Foreign assistance in the form of loans and grants, has covered all other expenditure. By the end of 2025, Ukraine had received nearly $168 billion through this channel, with annual tranches increasing over time, reaching $41.7 billion in 2024 and $52.4 billion in 2025.

Initially, significant assistance was provided by individual countries, particularly Japan, Canada, and the United Kingdom, although the United States and the EU remained the principal actors. International financial institutions, such as the International Monetary Fund and the World Bank, also played an important role. In subsequent years, dedicated support instruments for Ukraine were introduced. In 2024, the EU launched the Ukraine Facility, through which the country had received €26.8 billion by the end of 2025. In the same year, the G7 established a $50 billion mechanism known as ERA (Extraordinary Revenue Acceleration Loans for Ukraine)[3], which became the main source of inflows in 2025.

A serious challenge arose when the United States withdrew from direct financing of the Ukrainian budget following Donald Trump’s assumption of office as president. Despite this, the vast majority of Ukraine’s needs for 2026–27 are likely to be covered following the EU’s decision to raise €90 billion in joint debt for Ukraine.[4] In addition, a decision to approve a new IMF programme worth $8.1 billion over four years is in its final stages.

…and growing problems with public debt

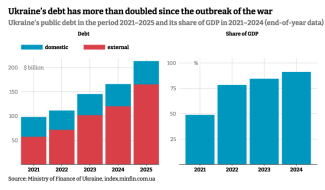

Foreign support for Ukraine is predominantly provided in the form of low-interest loans; only a small share (primarily from the United States) consists of non-repayable grants. As a result, public debt has more than doubled since the outbreak of the war, soaring from $98 billion in early 2022 (equivalent to around 49% of GDP) to $213 billion in early 2026. Although official figures are not yet available, all indications suggest that public debt has already exceeded 100% of GDP.

The costs of repaying and servicing public debt have been rising each year and are set to become an increasingly pressing challenge for the Ukrainian government. In the 2026 budget law, they constitute the second-largest category of expenditure after defence. According to the repayment schedule, Ukraine will have to allocate an average of $15 billion annually over the next decade to meet these obligations. In this context, an important consideration is that the repayment of the €90 billion EU loan will burden Ukraine only if Russia pays reparations – a scenario that appears highly unlikely under current circumstances.

Apart from foreign assistance, domestic sources of financing, primarily government bonds, have also played a significant (albeit considerably smaller) role. By 2025, however, this mechanism had largely run its course. While at the outbreak of the war the value of such securities on the domestic market stood at just over 1 trillion hryvnias, by early 2025 it had risen to 1.86 trillion – an increase of 86% in less than three years. By the end of 2025, it had reached 1.97 trillion hryvnias, meaning that growth slowed to less than 6% over the course of 12 months.

Trade – rising import expenditure

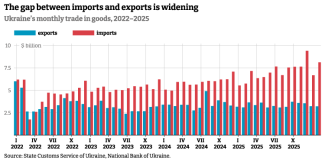

There was no improvement in goods exports in 2025. They amounted to $40.5 billion, slightly below the previous year’s figure of $41.7 billion. This figure is as much as 40% lower than the pre-war level recorded in 2021. Imports, however, tell a different story. Following a temporary collapse in the initial months after the invasion, they began to increase and, in 2025, exceeded the pre-war level, rising from $73 billion in 2021 to $85 billion in 2025. The widening trade deficit reflects the fact that many imported goods linked to the war effort – such as fuel, vehicles, and electronics (including components) used in arms production – have no domestic substitutes.

An important factor shaping trade flows, particularly exports, is the continued operation of Black Sea ports, which remain functional despite repeated Russian missile and drone attacks on infrastructure in Odesa, Chornomorsk, and Pivdenne. Moreover, investment projects continue to progress despite the damage, as illustrated by the construction of a new grain terminal with an annual throughput capacity of 5 million tonnes. Another positive factor is that there were virtually no blockades at land borders with the EU’s member states in 2025.

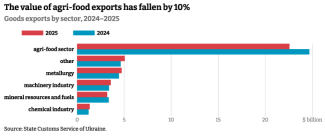

Relatively stable logistics did not prevent weaker performance in the agri-food sector, which accounted for 56% of Ukraine’s total exports in 2025. Food exports fell by 8.5% year-on-year, declining from $24.7 billion to $22.6 billion. The most pronounced decline occurred in grain exports, which fell by more than 20%, from $9.4 billion to $7.3 billion. This resulted from a confluence of factors. First, in June 2025, the European Commission decided not to extend the Autonomous Trade Measures (ATM), leading to the reintroduction of tariffs and quotas.[5] The revision of the Deep and Comprehensive Free Trade Area (DCFTA), adopted by the EU Council in October 2025 did not introduce any significant changes. Second, as US maize expanded its global presence,[6] it partially displaced Ukrainian production from the EU market, particularly in Spain. A further problem was the near-total loss of access to the Chinese market,[7] where domestic production increased and imports declined. Ukraine has partly succeeded in redirecting grain exports, primarily to Turkey, Egypt, and Algeria; however, the volumes have not yet been sufficient to offset the lost positions in the EU and China.

Exports of other goods from the agri-food sector increased, with sales of vegetable oils rising from $5.8 billion to $6.4 billion, and those of processed food products increasing marginally from $3.8 billion to $3.9 billion. Exports also increased across most other non-agricultural sectors. In particular, metallurgical production posted strong results, with foreign sales rising from $4.4 billion to $4.7 billion. As a result, concerns within the industry that the loss of coking coal mines in Pokrovsk would negatively affect exports have not materialised,[8] although export levels remain far below the $16 billion recorded in pre-war 2021.

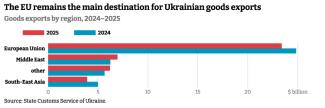

The fall in grain exports has affected the geographical structure of foreign sales. Although the EU remains the main market for Ukrainian goods, accounting for nearly 60% of total exports, the value of exports to the bloc fell from $24.8 billion in 2024 to $23.4 billion a year later.

In services, the IT sector delivered a strong performance, with exports reaching $6.66 billion in 2025. This consolidated its leading position, accounting for over 40% of total service exports. Although its 3.3% growth was modest compared with 2024, it exhibited positive quarterly dynamics: in the final three months of 2025, exports were 7.6% higher year-on-year.[9]

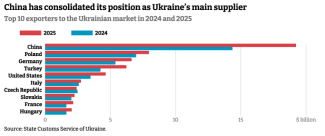

The largest share of Ukraine’s imports originates from EU countries. In 2025, these imports increased by nearly 11%, reaching $39.6 billion. Despite this, their share fell from 50.4% in 2024 to 46.6% a year later. This reflected the growing role of China, which has long been a leading supplier of goods to Ukraine. In 2025, it further strengthened its position, as Ukraine’s imports increased by 34%, rising from $14.4 billion to $19.2 billion. This means that nearly one quarter of Ukraine’s total imports now originate from this country. China remains a key supplier of a range of goods with varying degrees of relevance to wartime needs, particularly unmanned aerial vehicles ($1.4 billion in 2025) and their components, including batteries, transceivers, and various types of electronics. Such a high level of dependence may raise concerns about the stability of supply should China introduce restrictions on the export of these goods to Ukraine. However, these concerns appear to be overstated, as Ukraine has managed to establish a network of intermediaries, ensuring that most of these goods are not imported directly from China.[10]

In 2025, Poland remained Ukraine’s second-largest source of imports overall and the leading supplier among the EU’s member states. It plays a key role as a supplier of strategic energy commodities, including fuels, natural gas, coke, and electricity. Germany, ranking third overall, is a major exporter of motor vehicles, pharmaceuticals, and various types of machinery, including agricultural equipment.

The largest category of imports (valued at $7.7 billion, according to Ukraine’s Customs Service) is the unspecified category of ‘other goods’. Prior to the war, it was of marginal importance, but it expanded rapidly following the invasion. It most likely includes goods related to military and defence purposes. The main suppliers of products classified under this category were Turkey ($2.1 billion) and Bulgaria ($1.4 billion).

Energy sector – balancing on the edge

In the autumn of 2025, Russia launched another wave of intensive attacks on Ukraine’s energy sector, primarily targeting facilities responsible for electricity generation and transmission.[11] In the absence of detailed data, it appears that virtually all major power plants in the country (with the exception of nuclear facilities) have been damaged or destroyed. High-voltage substations have also been regularly targeted. As a result, both emergency and scheduled power outages have been reintroduced.

Although the situation at the national level does not appear worse than during the first wartime winter of 2022/23, individual cities are facing some of their most difficult conditions since the beginning of the war. This applies in particular to Kyiv, where the Darnytska combined heat and power plant was destroyed last January, with two other facilities of this type sustained serious damage. As a result, more than 1,000 apartment blocks (around 10% of such buildings in the city) are expected to remain without heating until the end of winter. Similarly difficult conditions persist in several other major urban centres, including Kharkiv, Kryvyi Rih, and Odesa.

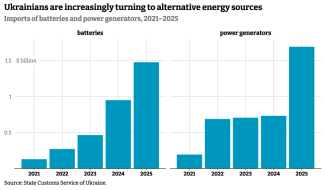

Russian attacks have negatively affected business conditions. According to a January survey by the European Business Association, 80% of companies reported experiencing the impact of power outages. At the same time, 90% of businesses reported having their own alternative energy sources,[12] indicating that they have adapted to persistent electricity supply shortages. This is corroborated by data showing a steady increase in imports of energy storage systems, which tripled between 2023 and 2025. In January alone, batteries worth nearly $250 million were imported into the country. According to some estimates, the total capacity of batteries owned by businesses and households has reached 3 GW,[13] equivalent to the output of three large nuclear power units. A similar trend can be observed with respect to power generators.

The widespread availability of generators and batteries has not resolved all challenges, particularly for larger enterprises. For smaller but energy-intensive businesses, such as bakeries and pizzerias, the high cost of electricity supplied by on-site generators poses a significant burden. According to estimates by the Institute for Economic Research, power outages in January alone reduced the country’s GDP by 1.4%.[14]

In the coming months, the main challenge will be to reconstruct damaged and destroyed energy infrastructure, particularly facilities involved in heat generation. On 20 February, Ukraine secured commitments from six countries to supply equipment from decommissioned power plants and combined heat and power plants, which will be transported to and installed in the country. The EU has also pledged an additional €600 million[15] to support the reconstruction of the Ukrainian energy sector ahead of the next winter.

Outlook

As long as the high-intensity phase of the war continues, it is difficult to expect any significant change in the trends observed since 2023. The Ukrainian economy has largely adapted to operating under these conditions, a shift facilitated by a substantial flow of Western funding to support the functioning of the state, as well as by innovative solutions implemented by businesses. At present, there are no indications of a deeper crisis, uncontrolled inflation, or a collapse of the national currency. However, under wartime conditions, there is no basis for more rapid economic growth, except in narrow sectors such as the production of unmanned aerial vehicles and electronic warfare systems. These industries remain too small to act as a driving force for the economy as a whole.

The principal challenge in the coming months will be to prepare major cities for the next heating season. Unlike previous waves of Russian attacks, those ongoing since last autumn have caused significant damage not only to electricity generation facilities but also to heat production infrastructure in several major cities, particularly in Kyiv. All indications suggest that Ukraine has weathered the most critical period of freezing temperatures, but it now needs to repair or even rebuild its heat-generating infrastructure. Given that such investments cannot be implemented rapidly, Ukraine is effectively entering a race against time.

[1] The ongoing war may raise concerns regarding the reliability of Ukrainian data. In some cases (for example, much of the data relating to the energy sector), such data are no longer publicly available. However, in the vast majority of cases, they continue to be published with the same level of detail and accessibility as prior to Russia’s aggression. This applies to institutions such as the National Bank of Ukraine, the State Statistics Service, the State Customs Service, and the Ministry of Finance.

[2] No more recent data are available.

[3] M. Jędrysiak, S. Matuszak, I. Wiśniewska, ‘The G7 Summit: $50 billion has been promised to Ukraine’, OSW, 18 June 2024, osw.waw.pl.

[4] Ł. Maślanka, S. Matuszak, I. Wiśniewska, ‘A bitter compromise over the EU’s financial assistance to Ukraine’, OSW, 19 December 2025, osw.waw.pl.

[5] S. Matuszak, ‘Ukraine–EU: finalisation of the DCFTA revision’, OSW, 7 October 2025, osw.waw.pl.

[6] А. Муравський, ‘США витісняє українську кукурудзу зі світових ринків’, Економічна правда, 12 February 2026, epravda.com.ua.

[7] ‘Нічого особистого: як Китай замістив майже весь агроімпорт з України’, Latifundist, 21 February 2025, latifundist.com.

[8] S. Matuszak, ‘The prospect of losing Pokrovsk – a blow to Ukraine’s metallurgical sector’, OSW, 20 December 2024, osw.waw.pl.

[9] ‘Gradual Market Stabilization: What Tech Services Exports Looked Like in 2025’, Lviv IT Cluster, 20 February 2026, itcluster.lviv.ua.

[10] K. Nieczypor, S. Matuszak, ‘Game of drones: the production and use of Ukrainian battlefield unmanned aerial vehicles’, OSW Commentary, no. 694, 14 October 2025, osw.waw.pl.

[11] S. Matuszak, ‘On the eve of a heating season: Russia targets weak links in Ukraine’s energy system’, OSW, 17 October 2025, osw.waw.pl.

[12] Ю. Тарасовський, ‘Вплив відключень електроенергії відчули 80% компаній, більшість адаптувалися – опитування EBA’, Forbes, 21 January 2026, forbes.ua.

[13] А. Сахно, ‘Українці накупили Ecoflow потужністю з атомний реактор’, Delo, 5 February 2026, delo.ua.

[14] Місячний Економічний Моніторинг України, no. 253, Інститут економічних досліджень та політичних консультацій, 18 February 2026, ier.com.ua.

[15] А. Кириченко, ‘Україна отримає виведене з експлуатації обладнання 6 європейських ТЕЦ та ТЕС’, Економічна правда, 20 February 2026, epravda.com.ua.