Racing against the next winter: Ukraine’s energy sector after the heating season

The past winter was the most difficult for Ukraine since the outbreak of the war. This was particularly evident in several major cities, including Kyiv, where residents faced not only prolonged power outages but, in some districts, also disruptions to heating. Once again, Russia failed to paralyse Ukraine’s power system, although it has been significantly weakened. In other parts of the energy sector, the situation appears more favourable. Ukraine has emerged from the heating season with larger gas reserves than in previous years following the outbreak of the war. Owing to well-diversified sources of supply for petrol and diesel fuel, in geographical terms, Russian attacks have not been able to disrupt deliveries.

The scale of destruction to the combined heat and power (CHP) system means that Ukraine is now in a race against time to repair or rebuild lost capacity before the winter of 2026/2027. A number of additional challenges are also posed by the war in Iran, particularly if the conflict becomes prolonged. A sharp increase in the prices of diesel fuel and natural gas would fuel inflation and contribute to higher defence spending. It would also make it more difficult to procure sufficient volumes of natural gas for injection into underground storage facilities. The most serious problem, however, may prove to be a shortage of missiles for Patriot air defence systems, which remain the only means of intercepting Russian ballistic missiles.

The scale of attacks and the challenges of repair and reconstruction

According to Ukraine’s Ministry of Energy, since the start of the full-scale war Russia has carried out nearly 6,000 attacks on the energy system.[1] Since October 2025, there has been an intensification of strikes on infrastructure related to electricity generation and transmission. Between 1 January and 24 February this year alone, facilities belonging to the transmission system operator Ukrenergo were targeted by 300 missiles and more than 7,000 drones. As in the 2022/2023 season and in the summer of 2024, prolonged power outages occurred, in some cases lasting more than 24 hours. The scale of the disruptions was not evenly distributed across the country: cities located on the left bank of the Dnieper, as well as Kyiv and Odesa, were the most severely affected, while in central and western Ukraine the outages were less acute.

During the 2025/2026 heating season, Russian forces succeeded for the first time on a larger scale in disrupting district heating systems in several major cities, such as Odesa and Kharkiv. Previously, such incidents had occurred, but were limited to front-line localities. Kyiv was particularly affected: on several occasions, outages lasting several days left around 6,000 multi-apartment buildings without heat supply, out of approximately 11,000 such buildings in the city, affecting an estimated 2 million residents.

At the beginning of February, the Darnytska combined heat and power plant was completely destroyed, as a result of which around 1,100 multi-apartment buildings were permanently deprived of heat supply. Two other major CHP plants in Kyiv – CHP No. 5 and CHP No. 6 – were also seriously damaged. This led to the suspension of hot water supply and restrictions on heating, with temperatures in many dwellings dropping to as low as 12°C. Moreover, interruptions in heat supply necessitated the draining of water from often ageing heating systems in buildings. This, in turn, generated significant technical difficulties – when refilled with hot water, pipes frequently burst, resulting in the flooding of entire risers.

An increasingly serious problem has been the recurrence of network failures, exacerbated not only by Russian attacks but also by an exceptionally harsh winter. These disruptions affected large parts of the country; for example, on 31 January of this year, cascading outages occurred across seven regions, as well as in Moldova. Localised failures – at the level of cities, districts, or individual buildings – were also frequent, and continued even after the cold spell had subsided. An example is the outages in parts of Kyiv on 22 March of this year.[2] For the power system, constant interruptions in electricity supply are a major challenge, as repeated switching on and off accelerates wear and tear on equipment. It can therefore be expected that this problem will intensify in the future.

Over the heating season, generating units with a combined capacity of around 9 GW – more than half of that available prior to the winter – are estimated to have been damaged or destroyed. Virtually every power plant (with the exception of nuclear facilities) was affected by strikes to varying degrees. According to the Minister of Energy, Denys Shmyhal, plans ahead of the next winter envisage the repair or reconstruction of 4 GW of generation capacity, as well as the construction of 1.5 GW of new capacity in decentralised facilities – comprising numerous small-scale energy sources (with capacities ranging from several to several dozen megawatts) distributed across the country.

The authorities have instructed the regions to prepare ‘resilience plans’, encompassing measures to safeguard the functioning of critical infrastructure during Russian attacks. These plans cover not only electricity infrastructure, but also facilities ensuring the supply of heat and water, as well as the operation of sewage systems. The estimated cost amounts to €5 billion and is expected to be covered by Ukraine’s international partners.[3]

Electricity imports as a lifeline from the EU

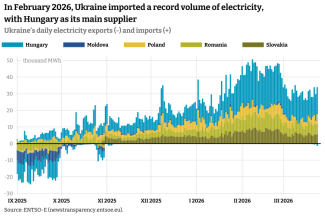

In the autumn, and particularly during the winter, the ability to import electricity from neighbouring EU member states and Moldova played an important role in Ukraine’s energy system. As late as September 2025, the country was exporting more electricity than it imported; however, following Russian strikes in October, this balance reversed, and from 11 November exports ceased altogether.

As the winter season approached and temperatures declined, electricity imports increased – from 415,000 MWh in November 2025 to 1.26 million MWh in February 2026. On some days in February, they approached the maximum capacity of cross-border interconnections. In the milder conditions of March, imports decreased but remained at a high level of around 25,000 MWh per day and were still significantly higher than in autumn 2025. Consequently, the situation improved and on 5 March Ukraine resumed electricity exports to Moldova, and on 21 March to Hungary and Romania, although volumes remain limited.

During the winter months, Hungary was the principal supplier of electricity to Ukraine (accounting for nearly 50% of Ukrainian imports in February), followed by Romania (19%), Slovakia (18%), and Poland (13%). Over this period, imports covered approximately 20% of Ukraine’s total electricity consumption.

The authorities in Budapest and Bratislava sought to exploit Ukraine’s high level of dependence, threatening to halt electricity exports while demanding the resumption of Russian oil supplies via the southern branch of the Druzhba pipeline, which had been suspended at the end of January following Russian shelling of the pumping station in Brody.[4] Despite this, no actual restrictions on electricity exports were implemented by either country. Only Slovakia terminated its agreement on the provision of emergency assistance to Ukraine.[5] However, according to the state-owned company Ukrenergo, this is expected to have only a limited impact on the stability of the power system, as such instances were rare and involved relatively small volumes.

The current import capacity of electricity interconnections with Ukraine stands at 2.45 GW; however, over the next two years the Ministry of Energy plans to increase it by a further 1.5 GW through the construction of new interconnectors with Romania, Poland, and Slovakia. In the longer term, a further expansion of 5 GW is envisaged.

The gas sector

In 2025, Russia launched large-scale attacks on infrastructure responsible for gas production and transmission. On at least two occasions, the strikes proved particularly severe: in February 2025, output temporarily declined by 40%, while at the beginning of October – following strikes on compressor and gas treatment stations in the Poltava region – it fell by 40–60%. Overall, in the past year Russia is estimated to have carried out 229 attacks on facilities belonging to companies within the Naftogaz energy group alone, with a further 25 recorded in the first two months of this year.

Owing to the very limited availability of public information, a comprehensive assessment of the scale of the damage is not possible. It appears, however, that the attacks have had a relatively limited impact on overall gas production. According to the consulting firm ExPro, output in 2025 amounted to 17.7 bcm, representing a decline of around 7% compared with the previous year. Nevertheless, the strikes have adversely affected the financial standing of extraction companies: their revenues fell from 181.4 billion hryvnias (approximately 4.1 billion dollars) in 2024 to 132.6 billion hryvnias (-27%), while net profit declined from 69 billion hryvnias to 14.3 billion hryvnias (-79%).[6] Even worse results were recorded by Ukrgazvydobuvannya, a subsidiary of the Naftogaz group responsible for around 70% of domestic gas production. Irrespective of the outbreak of the war, the company had in recent years consistently generated profits (52.7 billion hryvnias in 2024); however, it closed the past year with a loss of 5.5 billion hryvnias, most likely due to the need to procure equipment and spare parts required for the repair of damaged facilities.

Following the outbreak of the full-scale war, Ukraine imported only limited volumes of gas, owing to its existing reserves and reduced consumption. However, from spring 2025 – amid nearly depleted storage facilities and continued Russian strikes – it became necessary to resume large-scale imports.[7] According to data from OGTSU (the gas transmission system operator), net imports in 2025 amounted to 6.3 bcm, while between January and 25 March of this year they totalled 1.9 bcm.

In 2025, the main routes for fuel supplies were Hungary (45.4%), Poland (31.7%), and Slovakia (20.7%). The vast majority of volumes (5.5 bcm) were imported by Naftogaz, with 70% of procurement costs covered – through grants and loans – by international partners, including the EBRD and the EIB, as well as Norway and the United States.[8] An important role was also played by supplies of US LNG, which Naftogaz purchased via Orlen: in 2025, 600 mcm of the commodity reached Ukraine, while imports of 1 bcm are planned for this year.

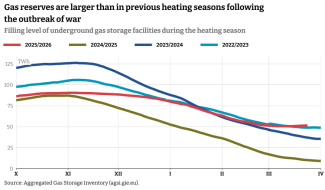

Ukraine entered the 2025/2026 heating season with reserves slightly higher than in the previous year, although at the same time significantly lower than in the two preceding seasons following the onset of the full-scale war. Owing to persistently high import levels throughout the winter, withdrawals from storage were lower than in previous years. The reduced consumption of gas was also influenced by the fact that part of the heat-generating infrastructure using this fuel had been damaged or destroyed.

Due to the lack of available data on gas consumption, its precise scale is difficult to assess. As of 18 March, storage facilities were filled to 16%, a markedly higher level than a year earlier, when it stood at just 3.5%, and also higher than at the end of the 2022/2023 and 2023/2024 seasons. Moreover, data from the AGSI platform indicate that from 13 March Ukrtransgaz ceased withdrawals from storage and began refilling, whereas in the previous season this process commenced a month later.

The fuel sector: total dependence on imports

In April 2022, the country’s only operational refinery, located in Kremenchuk, was seriously damaged, forcing Ukraine to meet almost its entire demand for fuels through imports. The facility was subsequently targeted on multiple occasions and most likely ceased operations definitively in June 2025. The refinery had processed domestically extracted crude oil, and its closure exposed a problem concerning the utilisation of this resource, which has been partially addressed through exports. According to data from the State Customs Service, between October 2025 and February 2026 Ukraine exported more than 260,000 tonnes of crude oil, primarily to Slovakia, as well as smaller volumes to Romania and Hungary.

Since the outset of the war, Russian forces have been destroying fuel storage infrastructure across the country, effectively preventing the accumulation of larger reserves. Despite temporary difficulties, traders adapted to the new market conditions as early as 2022 and were able to ensure continuity of supply.

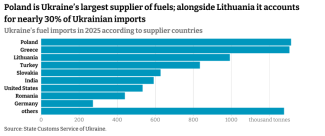

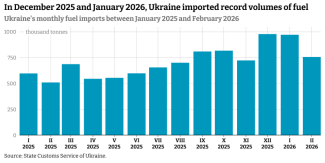

Overall, imports of petrol and diesel fuel in 2025 amounted to 8.2 million tonnes, representing an increase of 8.3% compared with the previous year. In geographical terms, Ukraine’s fuel supply is highly diversified; however, a leading role is played by products from Orlen refineries in Poland and Lithuania, which accounted for 28.2% of total Ukrainian imports in 2025. In the context of the fuel market, it should be noted that threats by Slovakia and Hungary to suspend deliveries to Ukraine carry limited practical significance, as even if implemented they would concern relatively small volumes that could readily be replaced by supplies from alternative sources.

Fuel imports increased significantly during the winter – in December 2025 and January 2026, monthly deliveries amounted to nearly 1 million tonnes, while in February, although they declined to 756,000 tonnes, they were still almost 50% higher than in the corresponding month of the previous year. It appears that the main driver of this sharp rise in imports over the last quarter was power outages, which led to increased consumption of fuels used in electricity generators.

Negative consequences of the war in Iran

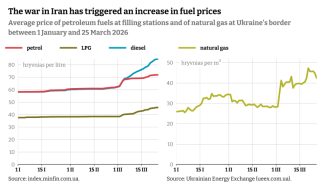

The US–Israeli strike on Iran launched on 28 February led to an increase in energy commodity prices on global markets. The most significant increases concerned diesel fuel, the price of which at Ukrainian filling stations on 25 March was 35% higher than at the beginning of the month. Price increases were also recorded for petrol (up 14.3%) and LPG (up 18.9%); however, the sharpest rise concerned the price of imported natural gas, which surged by as much as 49% between 1 March and 25 March – from 28,000 hryvnias to 42,000 hryvnias per 1,000 cubic metres.

Such sharp increases prompted the authorities in Kyiv to introduce compensatory measures – valid until May this year – to partially offset household expenditure on energy costs. These are set at 15% of spending on diesel, 10% on petrol, and 5% on LPG. According to preliminary estimates, the measure will cost the state budget at least 5 billion hryvnias. Although higher prices for imported fuels will have a positive effect on the revenue side of the budget – owing to increased VAT and excise receipts – expenditure on the defence effort will rise much more substantially. This applies in particular to diesel fuel used by the military. If high prices persist over a longer period, they will further exacerbate the already significant difficulties in financing the armed forces, especially as the budget provides insufficient funds for this purpose.[9]

Moreover, persistently high fuel prices will inevitably lead to an increase in inflation, which had largely been brought under control by the end of 2025 (8% year-on-year). They will also have a negative impact on the agricultural sector, which – like the military and the railway system – relies primarily on diesel to power machinery, while the spring sowing campaign is already under way. For smaller enterprises with limited financial capacity, the purchase of nitrogen fertilisers may also prove problematic, as global prices have risen owing to the blockade of the Strait of Hormuz. At the same time, elevated natural gas prices will make it more difficult to secure the funds needed to build up sufficient reserves in underground storage facilities ahead of the next heating season; in this regard, the challenge may lie not only in the cost of imports, but also in the physical availability of the commodity.

A shortage of PAC-3 missiles for Patriot air defence systems is likely to be the most significant adverse consequence of the war in Iran for Ukraine. Production capacity is very limited, and in the first two weeks of the Middle Eastern conflict more missiles were expended than manufacturers are able to produce in an entire year (620).[10] Moreover, priority in deliveries is likely to be given to the United States armed forces, which will seek to replenish their own stockpiles. Meanwhile, PAC-3 missiles – of which Ukraine has received approximately 650 since 2022 – remain the only means of intercepting Russian ballistic missiles. In the case of other missiles and drones, the Ukrainian armed forces have learned to counter them – albeit not always effectively – using a range of methods: from mobile units equipped with machine guns, through interceptor drones, to fighter aircraft.

Outlook

Ukraine has managed to withstand the most difficult period of the winter. Since mid-March, there have been days without any restrictions on access to electricity for the population, while outages following Russian strikes have lasted only a few hours and have not affected the entire country. All indications suggest that this trend will continue in the coming months; however, in the summer – particularly in July and August, when some nuclear power units will undergo scheduled maintenance – outages may occur, especially if high temperatures persist and electricity demand for cooling increases. It is, however, considerably more difficult to assess whether Ukraine will be able to rebuild the destroyed thermal generation facilities, above all the Darnytska combined heat and power plant in Kyiv.

A key factor shaping preparations for the next heating season will be the intensity of Russian strikes on energy infrastructure. Despite the onset of warmer weather, Russia has not ceased its attacks, which complicates the implementation of the necessary repair works. The effectiveness of air defence will be equally important. The Ukrainian armed forces have been relatively successful in intercepting cruise missiles and unmanned aerial vehicles. Moreover, even when Russian drones reach their targets, they are generally incapable of destroying larger facilities due to the limited explosive payload they can carry, and the damage they inflict can usually be repaired within several to a dozen hours.

Russia may also temporarily refrain from large-scale strikes, only to resume them in the autumn with renewed intensity, targeting repaired facilities that would no longer be possible to restore before winter. The most serious challenge may prove to be a shortage of missiles for Patriot systems, which – in the worst case scenario – could result in the destruction of key electricity and heat generation facilities. If the next winter were to be as severe as the last, this could bring Ukraine to the brink of a severe systemic crisis.

[1] А. Муравський, ‘За чотири роки Росія 5796 разів атакувала енергосистему України – Шмигаль’, Економічна правда, 24 February 2026, epravda.com.ua.

[2] В. Волокіта, ‘Аварія на обладнанні: частина Києва та області залишилася без світла’, Економічна правда, 22 March 2026, epravda.com.ua.

[3] А. Муравський, ‘Відновлення генерації: уряд планує цього року залучити ще п’ять мільярдів євро’, Економічна правда, 10 March 2026, epravda.com.ua.

[4] A. Sadecki, T. Iwański, ‘A dispute with Ukraine fuels Orbán’s election campaign’, OSW, 6 March 2026, osw.waw.pl.

[5] Д. Петровський, К. Черновол, ‘Словаччина зупиняє екстрені поставки електроенергії Україні, – Фіцо’, Уніан, 23 February 2026, unian.ua.

[6] ‘Прибуток газовидобувної галузі України впав упʼятеро у 2025 році — дослідження’, Vkursi, 17 March 2026, vkursi.pro.

[7] S. Matuszak, ‘On the eve of a heating season: Russia targets weak links in Ukraine’s energy systems’, OSW, 17 October 2025, osw.waw.pl.

[8] В. Грабовський, ‘Яким був 2025 рік для нафтогазової галузі України. Підсумки року’, НГУ, oil-gas.com.ua.

[9] S. Matuszak, ‘Ukraine: an unrealistic budget for 2026’, OSW, 17 December 2025, osw.waw.pl.

[10] J. Tarociński, ‘Operation Epic Fury and the US military presence in Europe’, OSW, 10 March 2026, osw.waw.pl.