Gains amid mounting challenges: the consequences of the war in Iran for Russia

The US-Israeli attack on Iran has had varied consequences for Russia. In political and strategic terms, the challenge posed by the Trump administration’s policy based on the use of force – targeting Moscow’s allies and exposing its inability to protect them – is accompanied by growing benefits resulting from Washington’s entanglement in a protracted conflict, which diverts US attention and resources away from Europe and the war in Ukraine.

In economic terms, short-term gains are becoming increasingly prominent. The blockade of the Strait of Hormuz and the resulting rise in global prices of energy commodities and mineral fertilisers have significantly boosted Russia’s budget revenues and eased US sanctions pressure. In addition, an opportunity has emerged to capture new markets while increasing exports to existing customers, which may lead to the establishment of new, more permanent trade links.

This has significantly alleviated pressure on Russia’s public finances, making it easier for the Kremlin to continue its invasion of Ukraine. These benefits have come just as the Russian economy has been shifting from stagnation to crisis, but they will not resolve its structural problems. The extent of the conflict’s impact on Russia will depend on its duration and its consequences for Iran, the region, and the wider world.

Strategic consequences: gains and challenges

In political and strategic terms, the US-Israeli attack on Iran has yielded a range of benefits for Russia, particularly in the short-term, which are likely to grow as the conflict drags on. At the same time, some of the consequences of the attack are unfavourable for Moscow, including in the strategic dimension, or have created new challenges and complications from its perspective.

Russia has primarily benefited from the diversion of US attention and resources to the war in the Middle East. This effectively precludes any shift by the Trump administration towards a more assertive policy towards Russia over Ukraine and opens the door to further reductions in deliveries of US weapons and military equipment to Ukraine. It could also prompt the White House to seek the Kremlin’s assistance in ending the conflict with Iran in exchange for further concessions, including with regard to Ukraine. President Trump’s telephone conversation with Vladimir Putin on 9 March indicated that this is a plausible scenario. According to Western media reports, Putin offered to halt intelligence sharing with Iran in exchange for similar restraint by Washington towards Ukraine.

Moreover, the war has led to serious friction between Washington and its allies, further weakening the cohesion of the Western world. Anti-American sentiment has intensified markedly, particularly among Western European public opinion. The image of the United States has also suffered among many countries worldwide, particularly in the Global South, a fact that Russia is seeking to capitalise on in its diplomatic and propaganda efforts.

However, the war in the Persian Gulf also has a number of adverse consequences for Russia. Above all, it has dashed the Kremlin’s earlier hopes, based on its assessment that the Trump administration’s policy was geared towards reducing the United States’ global engagement, particularly by avoiding large-scale military operations outside the Western Hemisphere and seeking a pragmatic modus vivendi with other major powers, especially Russia. Following a series of aggressive actions by Washington against states that form part of Russia’s network of anti-Western allies and/or clients (Venezuela, Cuba, and Iran), the Kremlin has concluded that it is dealing with an administration intent on restoring US global hegemony, including through the use of military force.

The Kremlin has been particularly concerned by the US armed forces’ demonstrated capability to carry out surprise strikes aimed at eliminating the political and military leadership of a targeted state, and by the Trump administration’s use of negotiations as a cover for such an attack. Moscow has also noted that the same officials who were negotiating with Iran are involved in talks with Russia regarding Ukraine.

Furthermore, the war in the Persian Gulf has exposed Moscow’s inability and lack of readiness to provide Iran, its close political and strategic partner, with meaningful support. Russia’s image has also been tarnished by its failure to act as a mediator in the conflict, a role that regional actors such as Pakistan and Turkey have assumed with some success. In addition, Russia’s previously close relations with the Gulf states have been strained, as these countries expected, and continue to expect, Moscow to side with them and to condemn Iranian attacks unequivocally.

Economic consequences: a boost for an economy sliding into crisis

The greatest benefit for Russia from the energy crisis triggered by the war in Iran is the rise in prices of exported fuels, particularly crude oil. According to estimates, if Brent crude remains at around $100 per barrel, the Russian budget will gain an additional $4–6 billion per month, doubling monthly revenues from the oil and gas sector compared with the first two months of this year. Under its budget assumptions for 2026, the Russian government projects that tax revenues from this sector will reach approximately $106 billion, 5% more than in 2025; this target will be met if current oil prices persist until the end of the year.

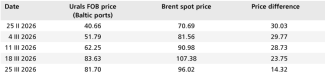

However, a scenario in which Russia earns significantly more is also conceivable, as the price gap between Russia’s Urals crude and other benchmarks continues to narrow, driven by a supply deficit on the market. Since 28 February, this gap has narrowed from $30 to around $14.

Table. FOB price of Russian Urals crude and the Brent benchmark price on the spot market from 25 February to 25 March 2026 (USD per barrel)

Source: authors’ own compilation based on Argus and EIA data.

Russian companies have also benefited from a roughly 30% increase in the prices of mineral fertilisers resulting from the blockade of the Strait of Hormuz (around one-third of global seaborne trade in mineral fertilisers, primarily nitrogen-based, passes through it in peacetime). Russia is the world’s largest exporter of these products (45 million tonnes in 2025). However, the Russian government is unlikely to allow companies to fully capitalise on these favourable conditions. The agriculture ministry has already introduced restrictions on the export of ammonium nitrate for the period from 21 March to 21 April to prevent any destabilisation of the domestic agri-food market.

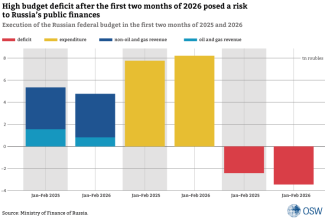

Consequently, the war in Iran has pushed back the prospect of revising the Russian budget. The budget law set the federal budget deficit for 2026 at 1.6% of GDP (around $41 billion), but after just two months it had already exceeded 90% of the amount projected for the entire year (3.45 trillion roubles versus 3.8 trillion roubles; see chart). It thus became clear that implementing the budget law as adopted would be impossible, forcing the government to seek savings. According to media reports, the finance ministry proposed spending cuts and a reduction in the baseline oil price set in the budget, which would allow the government to preserve the reserves accumulated in the National Wealth Fund (NWF) and curb the growth of public debt. However, following the spike in oil prices, this latter measure has been postponed until 2027.

From Russia’s perspective, another important benefit arising from the conflict in Iran is the reduced effectiveness of the Western sanctions regime resulting from a physical deficit of crude oil on the global market. This has forced importers to seek alternative sources of supply, including from Russia. Moreover, the easing of US sanctions policy – in the form of temporary waivers for trade in Russian oil – has increased the likelihood of a lasting erosion of these restrictions. Since the Trump administration took office in Washington, the United States has significantly reduced coordination of its sanctions policy with its European partners, including in areas such as pursuing vessels of the so-called shadow fleet and lowering the price cap.

Should Washington maintain this course, a protracted crisis will provide political justification for further steps to weaken sanctions against Russia. The Kremlin is also reinforcing this trend through propaganda efforts, using the current crisis to portray Russian exports as a stable source of hydrocarbons while seeking to drive a wedge between Western countries and to halt the process of phasing out Russian supplies.

If the blockade of exports from the Persian Gulf persists, Russian oil supplies will cease to be treated solely as ‘emergency’ imports and may begin to fall under long-term contractual arrangements. In response to the current crisis, countries such as Thailand and Vietnam have already expressed interest in Russian crude. Concluding such contracts would allow Russia to partially overcome an unfavourable development driven by sanctions and Western efforts to phase out imports from Russia – namely, its dependence on two main buyers: China and India.

Similar benefits could also emerge in the gas sector. The suspension of LNG supplies from Qatar has opened up new prospects for Russian gas exports (in March, a preliminary agreement was signed between Novatek and an importer from Vietnam), which will help sustain the operation of Russia’s gas sector as a whole despite Western sanctions. Supply constraints resulting from the war in the Persian Gulf have also provided an incentive for China to increase imports of Russian gas, which could bring Beijing closer to an initial decision to commence construction of a new pipeline from Russia – Power of Siberia 2.

Rising oil prices will not resolve Russia’s economic problems

In 2025, Russia’s economic growth slowed to 1%, down from 4.9% in 2024, and preliminary estimates indicate that the country’s GDP contracted by 2.1% year-on-year in January 2026. Moreover, last year – owing to sanctions, weak demand, rising production costs, and high borrowing costs – the share of loss-making companies in Russia rose to 30%; in recent years, a higher figure (31%) was reported only in the pandemic year of 2020. Negative financial results were recorded primarily by companies in the coal sector (over 65% of them), the oil and gas sector (nearly 50%, including Lukoil, with losses exceeding $12 billion), and in finance and insurance (45%).

The war in the Persian Gulf has disrupted global logistics and increased inflationary risks, significantly driving up prices and extending delivery times. This is particularly important for Russia, as over the past four years countries such as the United Arab Emirates, Turkey, and Iran have become key hubs for Russian trade, particularly for imports of high-tech goods and consumer products. Rising inflationary pressure is negatively affecting non-energy sectors of the Russian economy and exacerbating their existing problems, contributing to a further slowdown in economic activity.

The head of the Central Bank of Russia (CBR), Elvira Nabiullina, acknowledged that due to external factors (primarily the war in the Persian Gulf), the key interest rate was reduced on 20 March by only 50 basis points to 15%, rather than the 100 basis points previously under consideration. She also indicated that any further easing of monetary policy would depend on developments in the Middle East. Other government officials have likewise spoken with considerable caution about the benefits for Russia arising from the war in the Persian Gulf and their durability.

In addition, during the ongoing war in the Persian Gulf, the price of gold has fallen by nearly 15%, negatively affecting Russia’s reserves. As the country remains cut off from Western currencies, gold represents a key asset in which these reserves are invested, accounting for around 40% of the CBR’s total foreign exchange and gold reserves, valued at approximately $800 billion (of which around $300 billion remains frozen in accounts in Western countries). As early as February this year, the value of the CBR’s gold holdings fell by more than $74 billion. Gold also plays an important role in safeguarding public finances, accounting for roughly half of the government’s reserves held in the NWF.

Despite its positive effects on public finances in 2026, the war in the Persian Gulf and its consequences will not provide a lasting solution to Russia’s economic challenges. The Kremlin’s priority is to use the additional revenues to reduce the deficit and rebuild government reserves. The Russian government is aware that favourable conditions on energy markets could change rapidly as a result of either the end of the war or a global recession triggered by the energy crisis. The current inflow of funds is unlikely to enable the Kremlin to return to a policy of supporting the economy through public spending, as was the case in 2022–24, particularly as under current conditions, this development is translating primarily into inflation rather than growth in civilian production.