Attack on Iran: challenges for the oil market

The war between the United States and Israel and Iran, now entering its second week, is increasingly affecting neighbouring the Gulf states that export oil. The blockade of the Strait of Hormuz, which has been in place for several days, is limiting the availability of crude on global markets. Normally about 20 million barrels of oil and petroleum products pass through the strait each day, accounting for roughly 25% of global sales. As a result of the war and the blockade, Brent crude prices have so far (as of 6 March 2026) risen by about 18% compared with prices on 27 February, to more than $87 per barrel. At the same time, the prices of products imported from Gulf states are also rising, primarily jet fuel and diesel.

Asian countries, as the main importers from the conflict region, are faced with the most immediate challenge related to the oil and oil products price increases and a prolonged reduction in market supply. At the same time, these present also a challenge for the EU, which has been struggling with high energy prices and is trying to complete its shift away from importing fossil fuels from Russia. The developments are already pushing up prices on exchanges, which react to changes in supply and to the global situation. Any extension of the blockade of the Strait of Hormuz would have more serious consequences for both the oil and petrochemical markets and for entire economies. Russia’s oil and gas sector, meanwhile, may benefit from the problems in the Middle East.

The Strait of Hormuz and the global oil market

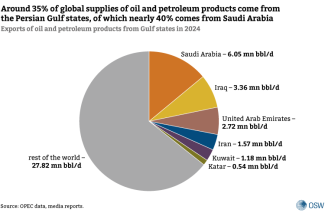

The Strait of Hormuz is a key export route for six oil-producing states in the Persian Gulf. Iran, Iraq, Saudi Arabia, the United Arab Emirates, Kuwait and Qatar hold about 55% of the world’s crude reserves. In 2024 these countries accounted for around 30% of global oil production and about 35% of its exports. Furthermore, they are important producers and exporters of naphtha, LPG, diesel, jet fuel and other petroleum products, accounting on average for more than 16% of global sales.

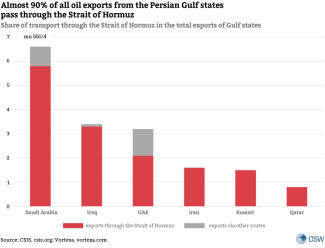

All the Gulf states depend either entirely or to a very large extent on the Strait of Hormuz for supplies to global markets. Before the war Saudi Arabia exported almost 90% of its oil and petroleum products through the strait, and the least dependent country, the United Arab Emirates, exported about two thirds through it.

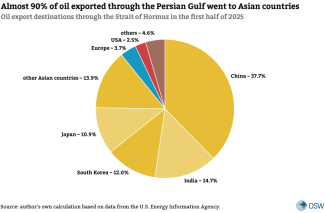

According to data from the Energy Information Agency, in the first half of 2025 the vast majority of crude oil exports from the region went to Asian countries, with the largest share going to China (around one third of total exports), followed by India, South Korea and Japan. Less than 4% of the crude exported via the Hormuz route went to European countries.

As a result, Asian countries have been affected first and the most strongly by the consequences of the closure of the Strait of Hormuz. Beyond crude oil prices, the cost of jet fuel has risen particularly sharply. On the Singapore exchange on 4 March it jumped by 140% compared with pre-war levels. Prices of diesel and LPG are also increasing. As supplies of crude oil have already begun to decline, China has called on domestic refineries to suspend exports of their products. Refineries in China, India and Singapore are reducing production, sometimes invoking force majeure clauses. Bangladesh has begun to cut deliveries to petrol stations, as it reportedly has petrol and diesel reserves for about two weeks.

Consequences for Europe

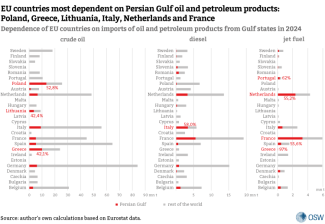

The situation in Europe is not as difficult. Supplies of oil and petroleum products from the six Persian Gulf states account for more than 12% of total EU imports (2024 data), although this dependence varies across individual countries. In the case of crude oil, Poland (52%) as well as Lithuania and Greece (around 42% of imports) are the most dependent on supplies from the Middle East, while many EU countries do not import crude from the region at all.

Beyond crude oil, the EU and the United Kingdom are heavily dependent on imports of jet fuel (more than 50% in 2025) and diesel (over 20%) from the Gulf. The volumes imported from the Middle East have increased in recent years due to the embargo on supplies from Russia and the decline in oil refining within the EU itself.

In the short term, Europeans can limit the current and potential future problems with oil and petroleum products due to their mandatory reserves of crude and fuels. EU countries are required to maintain stocks of oil and/or petroleum products equivalent to at least 90 days of their average imports or 61 days of consumption. In addition, spring brings a decline in demand for some products, including heating oil. However, prolonged difficulties in supplies of both crude oil and petroleum products from the Gulf will have clear and direct consequences for the EU market.

Rising prices of crude oil and products are already visible and are even being felt by end consumers. Alongside relatively moderate increases in crude oil prices (given the scale of the conflict), prices of jet fuel and diesel are reaching record highs on exchanges. Refining margins for jet fuel are currently almost 200% higher than a month ago. A longer closure of the route through the Strait of Hormuz would mean further volatility and price increases. Some countries, especially those most dependent on supplies from the region, would have to seek alternative sources. This situation may also prompt efforts to increase Europe’s own refining capacity and intensify attempts to accelerate the large-scale production of sustainable aviation fuel. At the same time, developments in the Middle East are already being used, for example by Hungary, as an argument for maintaining oil imports from Russia. They may also weaken the determination of some countries to implement already adopted commitments to completely phase out Russian hydrocarbons. This trend may be reinforced by the easing of US sanctions on Russian oil and its oil sector observed in recent days.

Response from the region’s countries to the closure of the Strait of Hormuz

Unlike with LNG exports, Gulf states – primarily Saudi Arabia and the United Arab Emirates – can redirect part of their exports of oil and petroleum products to alternative routes. Saudi Aramco operates a pipeline with a nominal capacity of 5 million barrels per day (most likely currently increased to 7 million bbl/d), running to the port of Yanbu on the Red Sea. Available capacity is estimated at around 5 million bbl/d and the Saudis have been increasing exports via this route for several days. In theory, it would allow most of their crude oil normally shipped via the Strait of Hormuz to be redirected.

The United Arab Emirates has a smaller pipeline (just under 2 million bbl/d) bypassing the Persian Gulf and running to the key terminal in Fujairah on the Gulf of Oman. In total, the spare capacity of these two routes could accommodate about 30-40% of the region’s crude exports previously shipped through the waters of the Persian Gulf. However, this involves more complex logistics and higher transport costs. In addition, both the Red Sea route and the Gulf of Oman are not currently fully secure, primarily due to possible attacks by the Houthis or Iran itself. This has been confirmed by strikes on Fujairah and by some suppliers to the terminal (mainly bunker fuel) invoking force majeure clauses. The limited capacity of alternative routes and storage facilities will most likely lead to production cuts by additional Gulf producers in the near future.

Another major regional exporter, Iraq, does not have a similar alternative. Only about 3–5% of its exports are carried through the pipeline from Kirkuk to Turkey. Furthermore, Iraq has the smallest storage capacity relative to domestic production among the countries in the region. As a result, on 3 March Baghdad announced production cuts at some of its oil fields. In total, output fell by 1.5 million barrels per day in the first days and the cuts mainly affect the country’s largest fields, Rumaila and West Qurna-2. The decline could double in the coming days if the export route is not reopened. In addition, attacks affecting extraction infrastructure are another reason for the reductions in production levels.

Iran itself also has limited alternative export options. The Goreh–Jask pipeline runs to the Gulf of Oman, but it has so far been used only once on a test basis and it is unclear whether it is suitable for sustained use. Moreover, its capacity (around 1 million bbl/d, most likely not fully available) would allow only part of Iran’s pre-war export volumes to be redirected. The challenge in assessing Iran’s alternative export options is compounded by the lack of easily available information about the condition of its oil sector, including its export infrastructure, following the US and Israeli attacks, including on Kharg Island, which is crucial for exports through the Strait of Hormuz.

Iranian attacks are also affecting regional refining capacity, including the largest refinery complex in the Middle East, Ras Tanura in Saudi Arabia. This is also reducing regional production capacity in this segment of the market.

Prospects

In addition to the ongoing blockade of the Strait of Hormuz, the fact that the energy infrastructure of Gulf states, as well as tankers outside the strait itself, have become targets of Iranian attacks is a further challenge for production and the short-term outlook for exports from the region. These actions suggest that Iran is seeking to increase the cost of the conflict for its neighbours and to push them to work towards de-escalating it. As the closure of the Strait of Hormuz continues, these attacks will fuel market anxiety and increase the risk of the reduced availability of infrastructure and, consequently, of supplies of crude oil and petroleum products from the region in the longer term. More lasting damage or prolonged shutdowns of production will make it harder to resume output even after the war ends. All this will increase market volatility and place upward pressure on prices, while also prompting key actors and major importers to take steps to restore transport through the Strait of Hormuz.

The United States, China, France and others have already taken these steps. On the one hand, they involve pressure – primarily from Beijing – on Iran to allow shipping and trade to continue. On the other, they include US proposals to provide guarantees for insurers and/or to ensure naval escorts for tankers. These efforts may be supported by the expected depletion of Iran’s military capabilities, which should lead to a reduction in the scale of attacks.

The impact on the market conditions is also moderated by the fact that an oversupply of oil had been forecast for 2026, including by the International Energy Agency (IEA). This was expected to result from the limited pace of global demand growth due to economic conditions and from increasing production in the Middle East and North America. According to the IEA, global oil inventories are at their highest level since 2021. In addition, for at least several weeks, as the United States was building up military forces in the region, markets had been preparing for war, which was reflected in the rise in oil prices in anticipation of the outbreak of the conflict. Finally, refinery demand for crude is currently falling, perhaps even faster than production capacity in the Middle East, as a result of damages in Gulf states and production cuts in Asian countries.

These factors may partly explain the relatively limited increase in crude oil prices in the first days of the conflict. During the oil crisis in the 1970s prices rose fourfold, while following the start of the Russian invasion of Ukraine Brent crude prices exceeded $120 per barrel. However, if the conflict in the Persian Gulf drags on, the situation could change rapidly. According to Qatar’s energy minister, further production cuts in the region can be expected in the coming days and oil prices could reach $150 within a few weeks. The seriousness of the problem is compounded by the fact that the closure of the Strait of Hormuz blocks access not only to currently exported volumes of crude but also to what are arguably the most important global spare production capacities, mainly in Saudi Arabia, which normally allow production to adjust to changes in demand on the global markets.

Both the current challenges and the prospect of a prolonged crisis on the oil market (as well as on the gas market) favour Russia’s energy interests. Russia would have the prospect of increasing both the volumes and the value of its exports, which are currently limited by sanctions. This is reflected in India’s declaration that it is willing to purchase Russian oil and LNG, the temporary easing of US sanctions on crude supplies to India, and voices emerging in Europe calling for a revision of the current policy on Russian fossil fuels. Some argue not only for slowing the phase-out of their imports but also for increasing them and, for example, easing EU sanctions. In addition, the war in the Gulf creates an opportunity for Moscow to once again use its energy supplies as a political tool. This is illustrated, for example, by Vladimir Putin’s suggestion that Russia could consider redirecting its gas exports from Europe to more promising and faster growing markets.