When trouble strikes, turn to the Kremlin: how the blockade of the Strait of Hormuz benefits Russia’s oil exports

The war in the Persian Gulf and the resulting disruption to global hydrocarbon markets have strengthened Russia’s position as an energy exporter. The blockade of the Strait of Hormuz gave rise to shortages of crude oil, refined fuels and LNG, forcing importers to seek alternative sources of supply. Moscow was among the main beneficiaries, with many buyers – particularly in Asia – turning to Russia. By expanding its customer base, Russia increased its exports while reducing its dependence on its two largest buyers, India and China. The US decision to ease sanctions further amplified these gains by easing importers’ concerns about the political costs of deepening trade ties with Moscow.

This stronger bargaining position represents a significant advantage for the Kremlin. The narrowing discount on Russian crude suggests that Russia has gained greater pricing power than it had before the crisis. The US decision to ease sanctions – even if only partially and temporarily – may also permanently reduce their effectiveness. Reimposing them effectively would require active enforcement against sanctions evasion, which in turn depends on political will in Washington. Although some Asian countries are likely to view imports from Russia as a form of insurance against future supply shocks and seek to maintain these trade flows, the prospect of the Strait of Hormuz reopening and additional volumes returning to the market could reverse the trends that have benefited Moscow.

US sanctions relief as the key driver

The war in the Persian Gulf and the blockade of the Strait of Hormuz disrupted global markets for crude oil, refined fuels and natural gas. According to available estimates, the inability to export hydrocarbons from the region reduced global supply by between 8 and 14 million barrels of crude oil per day (bbl/d), depending on the source and the stage of the conflict. This represented up to 15% of global oil trade. The supply shock affected Asian importers most severely. From March onwards, they began urgently seeking alternative suppliers to replace imports from the countries affected by the blockade: Iraq, Saudi Arabia, Kuwait and the United Arab Emirates.

From early 2023 to March 2026, around 80% of Russia’s crude oil exports went to just two markets: China and India. Other Asian countries refrained from purchasing significant volumes of Russian crude because of Western sanctions and instead relied on supplies from other producers, including the Arab states. However, the sharp rise in prices and the market disruption caused by the blockade of the Strait of Hormuz forced many Asian governments to reassess their approach. Energy security became the overriding concern, requiring them to secure alternative supplies immediately to avoid shortages and economic disruption.

According to media reports, the market disruption prompted several Asian countries to lobby for the suspension of US sanctions on Russian oil as a means of mitigating the effects of the crisis. On 13 March, the US Department of the Treasury introduced a one-month waiver covering Russian exports, allowing transactions with Russian entities involving the purchase of crude oil and refined petroleum products already loaded onto tankers. According to the US Treasury Secretary, the decision responded to requests from “around 10 affected countries” seeking relief from the crisis.[1] The waiver was extended twice before expiring on 17 June.

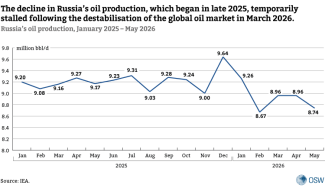

The measure did not lead to lower global oil prices, which continued to reflect a physical supply shortage. The US decision did not address this underlying problem, as the Russian barrels were already on the market and available to buyers willing to accept the risk of sanctions. Instead, the Treasury waiver primarily reduced the costs of circumventing sanctions, making Russian oil more attractive to traders. As a result, Russia regained the ability to export crude to a wider range of buyers, increasing its commercial flexibility while also helping to temporarily halt the decline in the country’s oil production.

China and India: the anchors of Russia’s oil exports

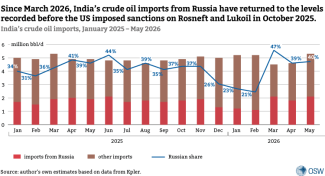

In volume terms, the increase in demand for Russian crude has been most pronounced in China and India, reflecting their importance as Russia’s two largest export markets. Indian imports, however, continue to be influenced by the threat of US sanctions. The sharp increase in purchases followed a series of US sanctions waivers allowing trade in Russian oil, preceded by a US Treasury Department licence issued on 5 March that exclusively authorised India to import Russian crude. In March, deliveries to India nearly doubled month on month, reversing the earlier downward trend driven by political pressure from Washington.[2] It is also worth noting that Indian refineries continued to import Russian oil even during the brief period in April this year when the sanctions waivers lapsed.[3] This may suggest, among other things, that the credibility of US sanctions has weakened as a result of inconsistent signals from Washington.

The lifting of US sanctions had a much smaller impact on China's willingness to import Russian crude. To a large extent, this trade remains independent of the sanctions regime because it is relatively insulated from Western market participants. Chinese imports of Russian crude increased at the end of 2025 and reached a record high in January 2026 as cargoes originally intended for India were redirected following a decline in Indian purchases under US political pressure. Although Russian deliveries to China declined between February and April, they continued to account for a significant share of the country's total crude imports.

The decline in imports in April reflected a broader fall in China’s domestic demand for crude oil. Faced with high prices, Beijing slowed the pace of replenishing its reserves and reduced fuel exports. Against this backdrop, Russian crude strengthened its position as a key component of China’s crude oil imports.[4] From Beijing’s perspective, this is an unfavourable trend. Previously, Chinese importers had enjoyed greater bargaining power because Russia had limited options for exporting its crude. As a result, Chinese refineries could purchase heavily discounted Russian crude, much like the oil they imported from Iran.

A broader return to Southeast Asia

The expansion of Russia’s customer base into new markets has been equally important for its oil exports. Although these buyers do not import volumes comparable to those of China or India, the emergence of new customers has significantly strengthened Russia’s bargaining position in negotiations with all its trading partners.

In March, Russian crude reached the Philippines for the first time in more than four years. Philippine President Ferdinand Marcos said that Manila was ‘exploring’ the possibility of signing long-term contracts with Russian suppliers.[5] Several other countries in Southeast Asia, including Thailand, Sri Lanka, Indonesia, Singapore and Vietnam, also announced plans to begin or expand imports of Russian crude.[6] At the same time, Russian exports to Egypt rose sharply. A similar trend was evident in exports of refined petroleum products. In April, Singapore doubled its imports of Russian fuel oil due to the absence of shipments from the Persian Gulf,[7] while Brazil steadily increased its purchases of Russian diesel between March and April.[8] By contrast, Turkey reduced its imports of Russian crude in response to rising prices.[9]

For some of the countries mentioned above, resuming imports from Russia means restoring trade ties that were severed after 2022 as a result of US sanctions. In Southeast Asia, Russian crude has primarily served as an emergency source of supply because transporting it is significantly more expensive than importing crude oil from the Middle East. Nevertheless, governments in the region may seek to protect themselves against similar supply shocks in the future by negotiating long-term contracts with Russian exporters and treating such deliveries as a means of strengthening their energy security. The fact that countries including the Philippines and Thailand have initiated government-level contacts with Russia on this issue suggests that this scenario is plausible.

Conclusions: long-term gains for Russia, but with lingering uncertainties

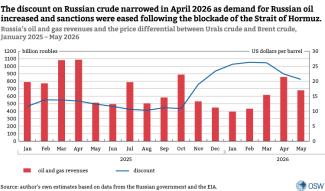

Although higher global oil prices have contributed to increasing Russia’s budget revenues,[10] this effect is temporary. Over time, markets tend to rebalance, bringing prices back down. By contrast, Russia’s stronger bargaining position, resulting from the expansion of its customer base in Asia, could have more enduring effects by supporting higher budget revenues over the long term. Buyers’ willingness to accept higher prices has narrowed the discount on Russian crude, boosting government revenues. This trend is reflected in official Russian government data, which show that the gap between the tax reference price for Russian crude and the price of the benchmark Brent grade narrowed by nearly US$6 per barrel between March and May this year.

If the current trend continues, with Russia maintaining exports to a broader range of Southeast Asian countries, the price of Russian crude could converge more closely with those of other global benchmark grades even after market conditions fully normalise. Some buyers may come to view Russian supplies as a form of insurance against future supply shocks. Russia’s ability to maintain exports throughout the crisis also strengthens the Kremlin’s political position by reinforcing its longstanding narrative that Russia is a reliable supplier of hydrocarbons. At the same time, these newly established and consolidated trade relationships could also be used to secure political concessions.

The emergence of new buyers of Russian crude between March and June was also partly driven by their growing willingness to overlook sanctions, as well as by increasing political pressure to ease them, as reflected in Washington’s policy. Even if the US waivers were intended to be temporary and remain in place only until the market rebalanced, they weakened the sanctions regime and undermined its overall effectiveness. Restoring its full impact will require not only the reimposition of sanctions but also clear messaging from Washington and active enforcement against sanctions violators. The extent to which the sanctions regime is implemented will therefore directly affect whether Russia retains the long-term benefits of the trade relationships it established during the crisis. If sanctions are tightened again, renewed political pressure on buyers to stop importing Russian crude can be expected.

The continuation of the trends that have benefited Russia, such as a further narrowing of the discount on its crude, will depend on a range of factors over which Moscow has only limited control. Even if the Strait of Hormuz is reopened and shipping returns fully to pre-war levels, global oil prices could remain above their pre-conflict levels, partly because demand will be driven by the need to replenish depleted strategic reserves. However, the speed at which Gulf producers restore the volumes lost during the conflict will ultimately determine the extent to which prices decline. As supply normalises, the price of Russian crude will also come under downward pressure.

Moreover, the full reopening of the Strait of Hormuz could bring about significant changes in the global oil market that prove unfavourable to Russia. Russian crude may face competition from additional volumes from the Persian Gulf, which are likely to be more attractive to many Asian buyers, primarily because of shorter delivery times. The United Arab Emirates’ withdrawal from OPEC+ and the prospect of a permanent lifting of US sanctions on Iranian oil point to intensifying competition in the market, which could undermine Russia’s position as a leading crude oil supplier.

[1] F. Hussein, ‘US won’t renew Iranian and Russian oil waivers, Bessent says’, Associated Press, 24 April 2026, apnews.com.

[2] F. Rudnik, ‘Chaos is a blessing: the attack on Iran and the future of sanctions on Russian oil’, OSW Commentary, no. 715, 13 March 2026, osw.waw.pl.

[3] N. Verma, S. Aniyeri, ‘India buying Russian oil irrespective of US sanctions waivers, Indian official says’, Reuters, 18 May 2026, reuters.com.

[4] For the discount on Russian crude exported to China, see the chart in: China-Russia Dashboard: a special relationship in facts and figures, osw.waw.pl.

[5] ‘PBBM says PH working to secure fuel supply from Russia’, Presidential Communications Office, 25 March 2026, pco.gov.ph.

[6] ‘East Asian Countries Eye Russian Oil Imports Amid Global Energy Shock’, The Moscow Times, 13 March 2026, themoscowtimes.com.

[7] C. Hodgson, A. Hancock, O. Walker, ‘Singapore turns to Russian fuel oil as war restricts Middle Eastern supplies’, Financial Times, 23 April 2026, ft.com.

[8] R.S. Santos, ‘Russia Now Supplies 81% of Brazil’s Diesel Amid Iran War’, The Rio Times, 12 May 2026, riotimesonline.com.

[9] ‘Turkey curbs Russian Urals imports as prices rise, Asian demand strengthens’, Reuters, 27 May 2026, reuters.com.

[10] I. Wiśniewska, ‘Russia’s economy: heading towards recession?’, OSW, 14 May 2026, osw.waw.pl.