Chaos is a blessing: the attack on Iran and the future of sanctions on Russian oil

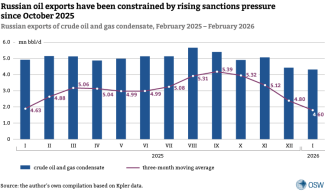

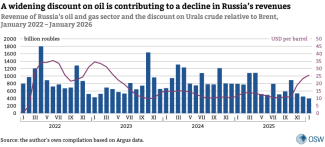

The fall in Russia’s oil and gas revenues observed since mid-2025, driven by falling global oil prices and a strong rouble, has deepened further owing to steep discounts applied to Russian crude in the final months of last year. These reflected heightened sanctions pressure from Western countries and their intensified diplomatic engagement with third countries, leading to a noticeable drop in supplies to India, a key buyer of Russian oil. The record-high discounts on Russian crude underscored the effectiveness of Western restrictions when implemented in a coordinated manner and under favourable market conditions, such as low global prices and the availability of alternative sources of supply.

However, the market uncertainty triggered by the US-Israeli attack on Iran has significant potential to reverse the trends working against Russia. The longer the Strait of Hormuz remains blocked, the deeper and more sustained the reduction in oil supply from the Persian Gulf is likely to be, thereby increasing the attractiveness of Russian exports as a key supplier for Asian buyers. A prolonged oil crisis would therefore have a positive impact on Russia’s oil and gas revenues by narrowing the discount on Russian crude and effectively undermining the effectiveness of sanctions instruments, as importers increasingly turn to Russian supplies in the absence of viable alternatives. This scenario also increases the likelihood that the political will among Western countries to impose further restrictions on Russia will gradually erode over time.

An interrupted blow – the prospect of rising prices

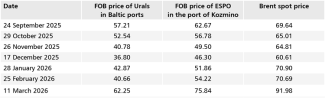

For exporters of Russian oil, the US-Israeli attack on Iran, which began on 28 February 2026, represents an exceptionally favourable development, primarily because it has intensified competition for the volumes of crude currently available on the market. Until recently, as oil prices remained low and the market was oversupplied, buyers and intermediaries showed little interest in purchasing Russian barrels because of the complications associated with their delivery. Under less favourable conditions – such as those created by the blockade of the Strait of Hormuz, which has severely hampered exports from the Gulf states – Russian crude has once again become attractive, offering a significant alternative for many buyers, particularly in Asia. The narrowing discount on Russian crude, which fell by $5 in the first week of March, and media reports of increased imports by India indicate a sudden rise in interest in Russian supplies.[1]

The rise in the price of Russian crude signals that the effects of the sanctions are beginning to erode, after their effectiveness increased markedly in the final months of 2025. Last October, the United States, the EU, and the United Kingdom introduced restrictions that significantly complicated Russia’s ability to sell oil (see Appendix) and reduced its revenues. Designations targeting key producers, notably the inclusion of Rosneft and Lukoil on US sanctions lists, extended the existing restrictions to cover the vast majority of Russia’s crude oil production. The reluctance among intermediaries and end buyers to handle cargoes from Russia affected seaborne exports, thereby driving down overall sales volumes.

At the same time, discounts on crude oil at Russian ports widened significantly. Between late October and late December 2025, prices fell sharply before recovering slightly in early 2026, in line with global price movements. Discounts on both grades of Russian oil sold at ports, Urals and ESPO, reached elevated levels not seen since 2023, standing at around $30 and $16 respectively, in late February 2026. This indicates that the restrictions imposed in October 2025 not only increased transport costs for tanker operators and intermediaries but also heightened concerns that end buyers could be targeted by secondary sanctions. As a result, they began demanding larger discounts to compensate for this risk.

The downward trend halted in early March following the US-Israeli attack on Iran, which pushed global crude oil prices higher and raised concerns about potential disruptions to supplies from the Persian Gulf. In response to tightening supply, Asian buyers once again turned to relatively accessible Russian crude, driving its price upwards. Reports have also emerged of individual transactions[2] in which prices were agreed at $4–5 per barrel above the Brent benchmark, reflecting the urgent need to secure supplies for Indian refineries.

Table. Daily FOB prices of Russian crude grades and the Brent benchmark on the spot market, 24 September 2025 – 11 March 2026 (in US$)

Source: the author’s own compilation based on Argus and EIA data.

India’s pullback, China’s ‘support’

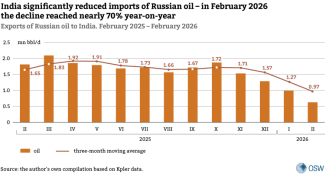

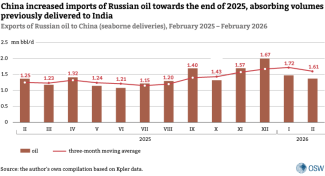

Another visible effect of sanctions pressure is a change in both the volume and the structure of Russian crude oil exports. The period from October 2025 to the end of February 2026 saw a decline in sales of Russian oil transported primarily by sea. Among the three main buyers of Russian crude (China, India, and Turkey, which together account for around 90% of Russia’s total exports), only China did not reduce its purchases during this period. Imports to India fell particularly sharply – by nearly 70% to around 650,000 barrels per day (bbl/d), close to levels last observed in mid-2022.

It should be noted that this reduction occurred under favourable market conditions. In 2025, OPEC+ decided to gradually phase out production cuts, which – together with increased crude oil output in non-cartel countries such as Brazil and Canada – contributed to the emergence of additional supply on the market, thereby easing competition among importers. India was thus able to increase imports from Saudi Arabia,[3] while also testing the feasibility of sourcing supplies from Venezuela.[4] In addition, the EU’s ban on imports of refined fuels produced from Russian crude oil, introduced in early 2026, further reshaped market conditions, forcing refineries in third countries, including India, to revise their import portfolios.

However, the change in India’s import structure was likely driven primarily by Western political pressure, which now appears to be weakening. Trade agreements that India was negotiating with the United States and the EU provided Western policymakers with leverage to press New Delhi to reduce its dependence on Russian oil – a demand forcefully articulated by the Trump administration. However, in response to the blockade of the Strait of Hormuz, Washington has partially revised its policy, allowing Indian refineries to temporarily purchase Russian crude oil already loaded onto tankers.[5]

The drop in deliveries to India (by around 1 million bbl/d) was partly offset by Chinese buyers absorbing a portion of these volumes. This allowed Russia to avoid a more severe collapse in exports, but forced it to offer significant discounts on its crude oil. The need to lower prices resulted from the stronger bargaining position of buyers and from rising logistical costs, as Russia’s Baltic ports had to handle a larger share of exports to China, rather than dispatching cargoes along the shorter route to India.

Internal dilemmas: production, logistics, and the budget

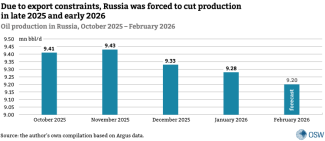

Persistent sanctions pressure has forced Russia to reduce domestic crude oil production, a development that is particularly significant given that, since April 2025, the country should have been increasing output in line with an OPEC+ decision to gradually phase out production cuts. In January 2026, Russian production fell for the second consecutive month to nearly 300,000 bbl/d below its OPEC+ quota.

Although the declines in production volumes have been modest, they primarily point to logistical difficulties resulting from the sanctions. The suspension of imports by key buyers, the ‘toxicity’ of Russian cargoes, and the need to redirect some shipments leaving Russia’s European ports away from India and towards China have reduced the pool of available tankers. Vessels undertaking these voyages must cover longer distances or operate as floating storage units, further limiting the availability of ships needed to sustain export flows.

The situation is further complicated by the ongoing addition of ‘shadow fleet’ tankers to the EU and UK sanctions lists[6] and the possibility that these vessels could be seized by Western countries. This has increased the risks associated with transporting Russian cargoes and has deterred intermediaries. Ukrainian attacks on ships and oil infrastructure, primarily in the Black Sea basin, have also exacerbated these logistical difficulties. Another issue is the build-up of domestic inventories. According to data provided by the analytics firm Kpler in mid-February, slightly more than 50% of Russia’s storage capacity, equivalent to around 16 million barrels, was filled at that time, although the actual capacity (including the system operated by Transneft, the state-owned pipeline operator) is larger.[7]

In late February, the Russian government signalled its concerns about constrained exports and low prices for Russian crude oil,[8] hinting at a possible downward revision of the annual oil export price assumed in the budget.[9] This would bring it closer to the forecast of the Central Bank of Russia, which anticipates an average price of $45 per barrel this year.[10] Russian officials confirmed reports of the impending revision by announcing the suspension of purchases and sales of foreign currency and gold under the so-called budget rule – precisely because the assumed oil price requires revision. This decision is aimed at shielding the National Wealth Fund from further depletion of its reserves. In March 2026, the Fund’s liquid assets totalled around $52 billion, or 1.7% of the country’s GDP. The government draws on the Fund to cover budget shortfalls when the oil export price falls below the baseline level. If the export price is indeed lowered, the government will face a dilemma: whether to finance spending through borrowing, namely domestic bond issuance, or to cut expenditure – an unprecedented step under wartime conditions.

Conclusions: the Hormuz blockade increases the likelihood of sanctions relief

The extent of the benefits for Russia will depend primarily on the duration of the crisis in the Persian Gulf. In the short term, Russian exporters will act as an ‘emergency’ supplier, selling off crude oil already stored on tankers and in domestic inventories. This will primarily help ease long-standing logistical constraints and avoid production cuts after months of mounting pressure. However, it will not translate into a significant increase in Russia’s oil export revenues if prices rise only briefly – especially if shipping in the Persian Gulf is fully restored in the near term and crude oil from Gulf producers returns to the market.

The export difficulties faced by Russia since October 2025, and their negative impact on revenues in the oil and gas sector, illustrate the country’s vulnerability to external pressure and shocks that it cannot withstand on its own. Its post-2022 dependence on a limited number of importers – with two or three Asian countries accounting for the bulk of Russian crude purchases – represents a structural weakness of Russia’s export model. At the same time, the widening discount indicates that sanctions pressure is producing results, particularly when coordinated across multiple Western jurisdictions and supported by enforcement tools deployed at sufficient scale.

A prolonged blockade of the Persian Gulf – lasting at least a month and acting as a positive external shock for Russia – would generate long-term benefits for Moscow by weakening sanctions pressure. Faced with a significant reduction in supply and depleting inventories in Asian countries, importers would be forced to source Russian crude oil on a regular basis despite the existing restrictions. Combined with elevated prices, this would narrow the discount, thereby boosting Russia’s export revenues and deferring the need to revise budget assumptions. Moreover, the growing risk of more sustained production cuts by the Gulf states – owing to their limited export capacity and depleted on-site storage – would reduce competition for Russian barrels. Physical damage to oil infrastructure in the Persian Gulf and the need for repairs would further affect global crude oil supply. The longer these disruptions persist, the greater the benefits for Russian exports.

Persistently high prices would also encourage Western policymakers to reassess the sanctions instruments targeting Russia, as indicated by the US decision to grant India temporary permission to purchase Russian crude oil already loaded onto tankers. In the shorter term, Western resolve to introduce new restrictions is likely to weaken, which may be accompanied by calls to ease the sanctions regime in order to mitigate the effects of the crisis.

The Kremlin will seek to exploit the uncertain environment for propaganda purposes, portraying Russian exports as a stable source of hydrocarbons, particularly for Asian countries. The physical absence of competing volumes from the Persian Gulf will strengthen the bargaining position of Russian suppliers vis-à-vis importers and lend credibility to the political narrative advanced by Russian policymakers. It should also be noted that any retreat by Western countries from the active use of sanctions against Russia would call into question the West’s political will to sustain economic confrontation with that country.

APPENDIX

Table. Restrictions imposed on Russian oil exports by the EU, the US, and the United Kingdom, January 2025 – February 2026

[1] K.N. Das, N. Verma, ‘Russia prepared to divert oil to India as Middle East conflict disrupts flows, source says’, Reuters, 4 March 2026, reuters.com.

[2] N. Verma, J. Renshaw, S. Holland, ‘Indian refiners buying prompt Russian oil as Iran war hits supplies, sources say’, Reuters, 5 March 2026, reuters.com.

[3] R. Sharma, Y. Chin, ‘Saudi Oil Surge to India Narrows Gap With Top Supplier Russia’, Bloomberg, 20 February 2026, bloomberg.com.

[4] M. Parraga, S. Khan, A. Somasekhar, ‘Venezuela readies larger oil cargoes for export, targets India’, Reuters, 24 February 2026, reuters.com.

[5] Y. Chin, R. Sharma, D. Wallbank, ‘US Grants Temporary Waiver for India to Import Russian Oil’, Bloomberg, 6 March 2026, bloomberg.com.

[6] According to data from the KSE Institute, 621 tankers are currently listed by the sanctions coalition.

[7] R. Bousso, ‘Suffocating Western pressure may finally force Russian oil output cuts’, Reuters, 16 February 2026, reuters.com.

[8] ‘Russia Weighs Cutting 2026 GDP Forecast After Oil Price Slump’, Bloomberg, 25 February 2026, bloomberg.com.

[9] ‘ЦБ РФ снизил прогноз по цене на нефть на 2026 год до $45 за баррель с $55’, Интерфакс, 13 February 2026, interfax.ru.

[10] ‘Минфин приостановит операции с валютой в марте’, Ведомости, 4 March 2026, vedomosti.ru.