At all costs. Germany shifts to LNG

Russia’s invasion of Ukraine, and the resulting collapse of the concept of an energy alliance between Berlin and Moscow, have become the catalysts for Germany to change its approach to building LNG import infrastructure. In order to become permanently independent of Russian supplies, Berlin has made an enormous financial effort to build its own terminals at record speed and on an unprecedented scale. The facilities planned will not only enable Germany to meet its economy’s demand for gas, but will also help it to maintain its role as the gas hub for Central Europe, which has been somewhat weakened recently. They will also allow it to continue to use gas as a transition fuel during the period of the country’s energy transition (Energiewende).

At the same time, the shift towards LNG poses certain challenges. For example, it creates the need to adjust the network to receive gas from new directions, and to find new suppliers of liquefied gas. The initiative to build LNG terminals on such a large scale has sparked major controversy in Germany because many observers view it as an unnecessary cost and a threat to Germany’s ambitious climate policy.

The war as the catalyst for change

Although prior to 2022 Germany had seen numerous private initiatives which involved the construction of LNG import infrastructure, for various reasons these failed to materialise.[1] The potential investors mainly complained about excessive competition from companies which imported gas via pipelines, unfavourable regulatory conditions, the uncertain market situation and the government’s increasingly ambitious climate policy. However, the most important obstacle was the lack of genuine political support (one that would go beyond declarations) for this type of project. Although a (small) portion of the political class did recognise the need to build LNG import infrastructure in order to diversify Germany’s gas supplies, it was unable to force through any genuine actions in this field. The main hindrance to carrying out this plan involved interests related to the policy of an energy alliance between Berlin and Moscow.

The genuine breakthrough in Germany’s attitude to building LNG terminals happened when Russia invaded Ukraine. Speaking in the Bundestag three days after the war’s outbreak, Chancellor Olaf Scholz announced his intention to launch initiatives to reduce Germany’s gas dependence on Russia, and revealed a plan involving the construction of two gas ports (in Brunsbüttel and Wilhelmshaven) which will come onstream around 2025. He also hinted that the state would support the implementation of these plans. Berlin’s initial intention was not to achieve full independence of Russian gas supplies: the goal was to diversify these supplies in the mid- and long-term perspective. It was the course of the war and the development of the political situation (in particular the increasing likelihood that Russian gas transmission would be halted, either at the initiative of the West or on the basis of a decision by Moscow) that the German government took emergency measures in spring 2022 to quickly make the country fully independent of Russia by constructing LNG import terminals with full support from the state.[2] The inauguration of the first facilities, less than a year after taking this decision, would not have been possible had Germany not applied a fast-track approach to enact a special law to reduce and simplify the numerous procedures, in a manner which was unprecedented in Germany. In particular these procedures involved assessing the investment’s impact on the environment, holding public consultations and issuing the necessary permissions.

Germany’s LNG projects

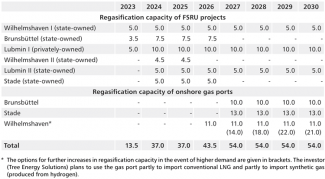

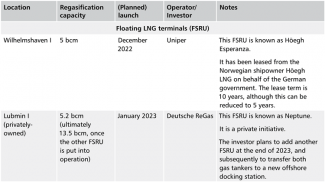

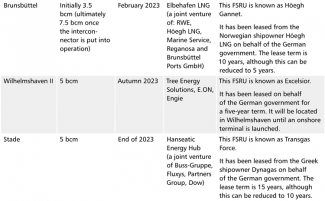

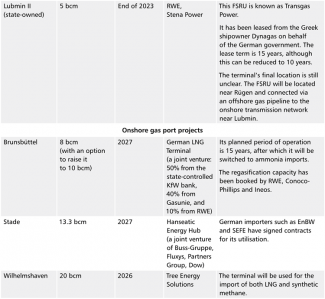

At present, Germany’s LNG import infrastructure projects include a total of seven so-called floating terminals, or Floating Storage and Regasification Units (FSRU), and three onshore gas ports (see Appendix). The German federal government has leased a total of five FRSUs, at Wilhelmshaven (two units), Brunsbüttel, Stade and Lubmin. The first (Wilhelmshaven I) was put into operation in December 2022, and the second (at Brunsbüttel) in February 2023; the other three units will be put into operation by the end of this year. These terminals will be leased for five, ten or fifteen years. Should the demand for regasification be less than expected, then in some circumstances these units can be returned to their owners sooner. In other instances, they can be used as standard gas tankers to transport LNG, or leased to a third party. The cost of both their lease and the necessary construction work at the quays will be borne by the German taxpayer, as will the costs of maintenance and insurance. Although in autumn 2022 the Bundestag approved the plan to earmark €9.8 billion for this purpose until 2038, the most recent forecasts regarding the initiative’s funding indicate that the required sum would be around as much as €10.5 billion. The Deutsche Energy Terminal GmbH company, which was incorporated in January 2023 and is controlled by the German state, is responsible for the coordination activities, management and funding of the ‘state-operated’ FSRUs. Aside from the five state-controlled FSRUs, the Deutsche ReGas company in Lubmin will implement a private project; this is being developed with support from the federal government and the government of Mecklenburg-Vorpommern. One FSRU (Lubmin I) has operated there since January 2023 thanks to this company’s efforts, and according to the investor’s announcements another one will be launched in the same location in December 2023.

Aside from the floating terminal projects, which are mainly intended to serve as a short- or mid-term solution, Germany plans to build three onshore gas ports. Their investors plan to put them into operation within three years; the terminal in Brunsbüttel will be the first such facility. Following the war’s outbreak, the state-controlled KfW bank acquired a 50% stake in this project (the federal budget will pay €744 million towards it).[3] Other projects which private investors will implement involve the facilities in Wilhelmshaven (in this case the project concerns a terminal which will be used for importing both standard LNG and liquefied synthetic methane) and those in Stade. All three terminals are expected to replace the FSRUs which have previously been operating in these locations.

The total regasification capacity of German terminals, once all of the planned facilities are put into operation, will rise from 13.5 bcm in 2023 to 54 bcm in 2027 (see Table 1). The construction of new LNG terminals in northern Germany on such a large scale, together with the increase in gas imports from Norway, the Netherlands and Belgium, and the expected permanent halt in Russian supplies, all equate to a fundamental shift in how the German gas transmission system operates. The modifications necessary to adjust it to the new dominant transmission routes have been taken into account in the updated Plan for gas network development.[4]

Table 1. Planned regasification capacity of German LNG terminals (in bcm)

Source: Federal Ministry for Economic Affairs and Climate Action.

The unprecedented scale

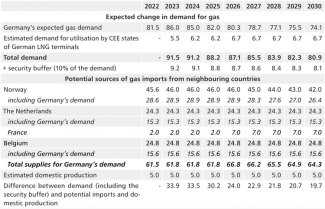

The unprecedented scale of the initiative to build LNG import infrastructure is widely discussed in German public debate at present. To justify the implementation of projects which have received direct or indirect support from the state, as well as their cost, at the beginning of March 2023 the Federal Ministry of Economic Affairs and Climate Action (BMWK) published a special report.[5] The document contains forecasts of Germany’s future demand for natural gas as well as estimates regarding the possibility of importing gas from sources other than Russia (Norway, the Netherlands, Belgium and France), and potential interest on the part of Central-Eastern European states in using German terminals, especially if Gazprom completely halts supplies to these countries. A 10% security buffer was added to the demand estimated on this basis, in order to take emergency situations into account such as seasonal hikes in gas consumption, potential malfunctions and even instances of sabotage targeting the existing gas infrastructure (including the gas pipelines running from Norway, which are currently of crucial importance to Germany). The figures presented in the report indicate that the gap that German terminals will need to fill will amount to 33.9 bcm in 2023, but will fall to 19.7 bcm by 2030 (the decrease results from the gradual reduction in gas consumption which Berlin expects).

Table 2. Gas demand forecasts and potential non-Russian sources of gas imports (in bcm)

Source: Federal Ministry for Economic Affairs and Climate Action.

The situation involving the planned terminals and the government’s justification for their construction prompts several conclusions.

Firstly, the planned infrastructure will enable Germany to permanently abandon Russian gas without any negative consequences for the security of supplies, even if the planned initiatives are not carried out in full.[6] Following the outbreak of the war, Germany opened its own terminals, increased gas imports from Norway, the Netherlands and Belgium, and began to import gas from France (in the latter three cases Germany buys LNG which is transmitted via these countries’ infrastructure). However, launching all the planned FSRUs without delay may be of key importance over at least the next two years.

Secondly, the planned LNG import infrastructure will enable Germany to meet not only its domestic demand but also a significant portion of the demand reported by the Central-Eastern European region as a whole. In recent months, the narrative promoted by German government representatives has emphasised the need to consider the demand for gas imports reported by Germany’s landlocked neighbours (the Czech Republic, Slovakia, Austria, Moldova) and those countries which do not have their own LNG terminals (Ukraine), especially in the situation of a permanent halt in Russian supplies. Official statements regarding this issue seem to corroborate the fact that despite the decrease in its importance as a transit country following the halt of supplies from Russia, Germany is not going to abandon its role as a Central European gas hub. In 2022, Berlin and Prague held talks on the Czech Republic potentially using the terminal in Lubmin. The government’s report highlighted the fact that Germany has included Ukraine and Moldova in its plans, because according to estimates together these countries could potentially be interested in importing up to 5 bcm of LNG annually via the German terminals; this volume corresponds to the capacity of one FSRU. As regards the Czech Republic, Slovakia and Ukraine, Germany’s plans may be viewed as competing with the Polish FSRU project in the Gdańsk Bay, which includes the option of these countries using this unit for their own purposes.

Thirdly, the deliberately created capacity surplus in excess of expected demand also results from a fundamental paradigm shift in Berlin’s approach to energy security and to the state’s funding of the initiatives which are intended to guarantee this security. Prior to Russia’s invasion of Ukraine and the failure of the model involving an energy alliance between Berlin and Moscow, Germany’s political elites largely downplayed both the need to diversify supply sources and the crucial role of LNG import infrastructure in this context. As a consequence, these elites were not ready to shoulder the additional financial burden associated with this. It was only when the Zeitenwende happened that Berlin became willing to spend huge funds on the import infrastructure which would enable the diversification of supply sources. This was also when Germany began to promote energy independence, the security of supplies, and the efforts to increase the system’s resilience to shocks in the main narrative in public debate.

Fourthly, the unprecedented scale of the planned infrastructure corroborates the view that although it has lost its gas supplies from Russia, Germany does not intend to abandon the use of natural gas as a transition fuel during the energy transition. This is particularly evident in the electricity generation sector. In the context of the shutdown of Germany’s remaining nuclear power plants on 15 April 2023[7] and the planned acceleration of the phase-out of coal in the second half of the present decade (to be completed by the 2030s), natural gas will increasingly be viewed in the coming years as an important fuel which stabilises and complements energy generation from renewable sources. As a consequence, despite the expected drop in gas consumption in other sectors of the economy, Germany’s demand for gas will remain high in the coming years, and the expected decrease of around 15% by 2030 compared to 2023 (and of almost 25% compared to the pre-crisis year of 2021) which the BMWK expects should be viewed as highly uncertain, if not unlikely. In this context, at the end of the present decade the expected surplus may turn out to be much smaller than currently estimated.

The scale of the already completed and announced investments in LNG import infrastructure has sparked major controversy. Its most ardent opponents include Germany’s highly influential environmental organisations such as Deutsche Umwelthilfe, BUND, Naturschutzbund Deutschland and Greenpeace, which have considerable experience in fighting LNG import projects. They have mainly highlighted the potential negative impact the new infrastructure could have on the environment, and have criticised the import of shale gas from the US, which environmental activists view as a controversial type of fuel. Many experts dealing with energy policy also view the implementation of all of the announced projects as not only unnecessary (because of the expected significant capacity surplus) but also harmful, especially from the point of view of public finance (huge costs) and of efforts to achieve climate policy goals (the risk of hindering the transition towards green technology by creating incentives to continue to use natural gas for a longer period and in larger volumes than necessary). Some analysts also argue that capacity surplus will result in a situation in which German terminals will not be used in full; that could reduce the revenues earned from their operation, and by extension, Germany’s ability to refinance the investment. This, in turn, will generate major losses for the federal budget.

What are the potential sources of LNG imports?

Aside from doubts regarding the infrastructure currently being developed, another problem involves the sources of Germany’s current and future LNG imports. Long before the war, Germany’s key gas importers, such as RWE and Uniper, had decided to expand their operations in the field of global trade in liquefied gas, and their portfolios included contracts with suppliers from around 20 countries worldwide. Prior to 2022, the majority of the gas they bought was sold on the more lucrative Asian market (up to two-thirds of the total volume, in the case of Uniper), while the remaining volume was sold on the European market, including Germany. In this context, it is worth noting that due to the absence of gas ports in Germany this gas was imported via terminals located in the Netherlands, Belgium and France. Since the end of 2021, which marked the beginning of the energy crisis, Europe’s demand for LNG has increased and a significant portion of gas shipments, including those bought by German importers, has been re-directed to the European market, in particular the German market, which at that time offered much higher prices than the Asian market. As demand rose at the height of the crisis, the importers complemented their contractual gas shipments with gas purchased on the spot market.

Germany’s three terminals currently operating receive their gas from German importers RWE, Uniper and EnBW/VNG (this is the case for the ‘state-operated’ facilities in Wilhelmshaven and Brunsbüttel), as well as from foreign companies such as Total and MET Group (in the case of Lubmin). Aside from shipments carried out on the basis of the contracts signed, the terminals receive gas purchased on the spot market. In Q1 2023, direct LNG supplies via the three German FSRUs accounted in total for around 6% of Germany’s total imports. However, it should be noted that the terminal in Lubmin was put into operation in mid-January and the one in Brunsbüttel as late as February. Until mid-April 2023, as much as 75% of LNG supplies shipped to the three German facilities originated in the US. The remaining shipments contained LNG from the United Arab Emirates, Nigeria, Egypt, Angola and Trinidad & Tobago. The origin of the LNG shipped to Germany via gas ports located in the neighbouring countries is more difficult to establish. It cannot be ruled out that LNG from Russia continues to be shipped to Germany via this route.

In the situation of Berlin’s shift towards increased LNG imports, in 2022 Germany’s main importers launched efforts to expand their supplier portfolios to include new long-term contracts. In the second half of the year it was revealed that contracts had been signed between RWE and the American Sempra Infrastructure company (3 bcm annually starting from 2027), Uniper and the Australian Woodside company (1 bcm annually starting from 2023), and between EnBW and the American Venture Global company (2.7 bcm annually starting from 2026). In addition, the American ConocoPhillips company announced its agreement with QatarEnergy regarding the supplies of Qatari gas (2.7 bcm annually starting from 2026) to the gas port in Brunsbüttel. ConocoPhillips has booked access to this facility.

However, these contracts are far from sufficient to guarantee that the market gap caused by the halt in Russian supplies can be permanently filled. With regard to the concept of purchasing most of the gas required on the highly unstable spot market, this will generate numerous risks in the long term, mainly due to the unstable availability of gas and its price fluctuation. Germany’s main importers are continuing to negotiate new long-term contracts with potential exporters from countries such as the US, Australia, Qatar, the United Arab Emirates, Oman, Egypt and Senegal. These negotiations have the backing of Germany’s top politicians including Chancellor Olaf Scholz and Vice-Chancellor Robert Habeck, who raise the issue of LNG supplies to Germany when meeting the leaders of these states. Moreover, the delegations include the CEOs of German companies interested in purchasing LNG.

At least some of these talks have encountered major obstacles because the parties have divergent views on many issues. This has resulted in the negotiations being unduly prolonged or have even led to impasses. The most glaring example of these problems have been the talks between RWE and Uniper (on the one hand) and QatarEnergy (on the other), which have been ongoing since spring 2022. Although Scholz and Habeck intervened with the Emir of Qatar, so far the companies have failed to reach an agreement. The proposed duration of the contracts is the main problem. German companies prefer to avoid signing multiannual contracts because of Germany’s climate policy, which envisages that the country will achieve carbon neutrality by 2045. This would require a major reduction in natural gas consumption as early as the 2030s and its almost complete abandonment in the mid-2040s. Moreover, the present legal regulations ban the import of LNG to Germany starting from 2043. This is why the importers usually prefer shorter and more flexible contracts (with a 10- or 15-year term), while longer contracts are in the exporters’ interest; for example, in the case of Qatar the preferred contract duration is as long as 20 years. Other problems affecting the negotiations include price setting mechanisms and the options for gas resale.

The hydrogen perspective

Another interesting aspect of the plans to construct the three onshore gas ports is their future potential to import hydrogen and hydrogen-based products. As regards the facilities in Brunsbüttel and Stade, the investors intend to switch to importing low-carbon ammonia in the future. This ammonia could be picked up directly by specific industrial facilities (in particular chemical industry plants), or processed on the spot to obtain hydrogen which in turn would be fed to the hydrogen transmission network that Germany plans to build. The terminal in Wilhelmshaven, for its part, has been conceived as a facility capable of receiving synthetic methane which Tree Energy Solutions (this gas port’s investor) plans to manufacture in other regions of the world and to import it to Europe. In the case of this facility, the LNG import option is viewed as a temporary supplement to the main concept.

Both the investors and German government representatives frequently refer to the possibility that these gas ports could be used to import hydrogen (and its derivatives) in the future. They view it as one of the arguments proving that the planned infrastructure could be of use in the long term. The German authorities have presented elements of this infrastructure to the public as ‘hydrogen-ready’ facilities which are capable of switching from LNG imports to hydrogen imports in the future. On the one hand, this could fit in with the process whereby the economy switches from fossil fuels to low-carbon energy carriers, which is one of the stages of the energy transition, and would pave the way for the long-term utilisation of these terminals. On the other hand, this option could serve as an infrastructural response to Germany’s permanent dependence on hydrogen imports; Berlin is aware that Germany will be unable to meet its expected demand from domestic production alone. According to estimates, Germany’s hydrogen imports will account for around two-thirds of its consumption; it will mainly be imported by land via gas pipelines, and also by sea from other continents.

However, the prospect of using gas ports in the future to import hydrogen or hydrogen-based products such as ammonia or methanol has sparked major controversy. It is clear that due to the different chemical properties of these products, the LNG import infrastructure cannot be automatically switched over to transport liquid hydrogen and ammonia. A major portion of this infrastructure’s components would need to be modernised, requiring significant funding. Experts have emphasised that in order to reduce the cost of adjusting the infrastructure so it can receive other products, the investors should take these adjustment works into account now when planning their initiatives.

Doubts surrounding the LNG import projects

At present, it is unclear whether all of the planned terminals will be built in line with their initial parameters. This mainly concerns the three onshore gas ports, regarding which no final investment decisions have yet been taken. It seems that at least the construction of the facility in Brunsbüttel, in which the state holds a 50% stake, is certain. Moreover, in the case of this facility, the regasification capacity has already been booked: the terminal will be operated by RWE, the American ConocoPhillips company and the British Ineos company. The gas port in Stade will most likely be built, as German importers such as EnBW and SEFE have already signed contracts regarding its utilisation. The future of the TES project in Wilhelmshaven is uncertain because no importers have yet declared their interest in importing LNG via this facility.

As regards the floating terminals, aside from the three already operational, it is certain that at the end of 2023 the FSRUs in Stade and in Wilhelmshaven, which have been leased on behalf of the German government, will be inaugurated. However, for the time being the location of the remaining unit Berlin wants to lease is still unclear. Initially plans were made to locate it near Lubmin, but the solution selected for this facility, involving connecting it to an offshore platform as part of the LNG hub near Rügen, has provoked opposition from the local communities. As a consequence, the investor (RWE), the German federal government and the government of Mecklenburg-Vorpommern are continuing to search for an alternative location. This will most likely delay the terminal’s launch, which had initially been scheduled for the end of 2023. As a consequence, it is unclear whether Deutsche ReGas will install another FSRU in Lubmin. According to the company’s initial plans, first the other FSRU and ultimately both FSRUs are to be connected to an offshore platform which RWE and the German government plan to build.

Germany’s plans to build LNG terminals and the importers’ decision to sign new long-term LNG supply contracts will enable Berlin to abandon Russian gas supplies fully and permanently, and will reduce the market’s potential for resuming imports from Russia – although it should be remembered that this latter option cannot be ruled out in the future. It should be expected that in the longer term, should relations between the EU/Germany and Russia normalise, a section of the German economic and political elite may seek to resume trade with Moscow, including the import of energy carriers, albeit on a smaller scale than prior to 2022. From Berlin’s perspective, such a move could be a potential political bargaining chip.

Moreover, in the context of Germany’s ongoing energy transition, which envisages that in the long term the importance of traditional fossil fuels will decrease in favour of new energy carriers, it should be expected that supporters of the plan to resume trade relations with Russia will seek to link these relations to the Energiewende, and to rely more on imports of low-emission hydrogen, ammonia and synthetic fuels, etc.

APPENDIX

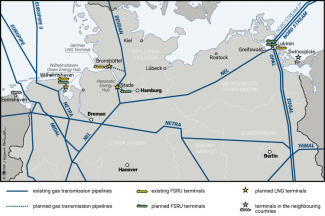

Map. Location of German LNG terminals

Source: Federal Ministry for Economic Affairs and Climate Action.

Table. Germany’s LNG import infrastructure projects

Source: the author’s own analysis, compiled on the basis of figures published by the Federal Ministry for Economic Affairs & Climate Action, and information published by the investors.

[1] M. Kędzierski, ‘Niemieckie terminale LNG – stan i perspektywy’, Komentarze OSW, no. 362, 10 November 2020, osw.waw.pl.

[2] Idem, ‘An abundance of gas ports. The emergency diversification of gas supplies in Germany’, OSW Commentary, no. 447, 20 May 2022, osw.waw.pl.

[3] Idem, ‘Niemcy: wsparcie państwa dla budowy terminalu LNG w Brunsbüttel’, OSW, 10 March 2022, osw.waw.pl; see also ‘Bund beteiligt sich an Flüssiggas-Terminal in Brunsbüttel’, Presse- und Informationsamt der Bundesregierung, 7 March 2022, bundesregierung.de.

[4] M. Kędzierski, ‘Germany plans to adjust its gas network to a rapid increase in LNG imports’, OSW, 7 April 2023, osw.waw.pl; see also ‘NEP Gas 2022-2032: Ein Meilenstein auf dem Weg zur Diversifizierung der Importquellen und der dauerhaften Unabhängigkeit von russischem Gas’, German Association of Gas Transmission Network Operators, 31 March 2023, fnb-gas.de.

[5] Bericht des Bundeswirtschafts- und Klimaschutzministeriums zu Planungen und Kapazitäten der schwimmenden und festen Flüssigerdgasterminals, Federal Ministry for Economic Affairs and Climate Action, 3 March 2023, bmwk.de.

[6] For example, according to the German Institute for Economic Research, for Germany to meet its import demand it would be sufficient to build the currently planned floating terminal projects, because onshore terminals are not needed in this context. The institute’s analysis indicates that in the mid-term perspective, in order to meet the German economy’s declining demand for natural gas it would be sufficient for Berlin to import this gas from Norway and to import LNG via the existing gas ports in the Netherlands, Belgium and France. For more see F. Holz, C. von Hirschhausen, R. Sogalla, L. Barner, B. Steigerwald, C. Kemfert, ‘Deutschlands Gasversorgung ein Jahr nach russischem Angriff auf Ukraine gesichert, kein weiterer Ausbau von LNG-Terminals nötig’, DIW Aktuell, no. 86, 22 February 2023, diw.de.

[7] M. Kędzierski, ‘It is official: Germany abandons nuclear energy’, OSW, 21 April 2023, osw.waw.pl.