Turkey’s LNG game amid the war in the Middle East

In 2025, Turkey increased its LNG imports by more than 32% year-on-year, enabling a genuine diversification of suppliers. The rise resulted from the availability of liquefied gas and growing domestic demand, driven by macroeconomic stabilisation. At the same time, it formed part of a deliberate strategy by Ankara, aimed at strengthening its position in renegotiations of gas contracts with Russia and responding to pressure from the Trump administration, which has made the improvement of bilateral relations conditional on reducing imports of Russian raw materials.

The increase in LNG import volumes forms part of Turkey’s long-term strategy, aimed at diversifying its gas supply sources, negotiating more favourable contractual terms, and transforming the country into a regional gas hub. However, the implementation of these objectives may face significant obstacles. Ankara continues to struggle with substantial infrastructural constraints – both in terms of transmission and storage capacity. Although these are being systematically expanded, they remain insufficient for large-scale gas re-export. The war with Iran may further complicate the situation by limiting LNG availability and delaying investments in Turkey’s re-export capacities.

Even more LNG

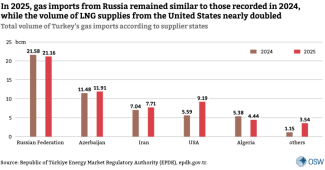

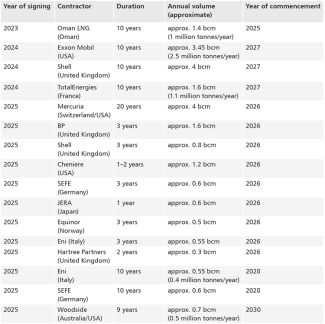

The most significant change in Turkey’s gas market in 2025 was the clear diversification of LNG suppliers. In that year, Ankara signed as many as 12 new short-term contracts for liquefied gas imports (see Table), compared with just three the previous year. In the coming years, these contracts (concluded for periods of one to three years) will allow for the import of approximately 15.8 bcm of LNG (with additional agreements entering into force, this figure is expected to rise to around 25 bcm by 2027). This will be sufficient to cover approximately 25% of annual gas demand (around 60 bcm last year). The increase in total imports in 2025 was driven almost entirely by the rise in LNG deliveries – pipeline imports grew by merely 4.2% compared with 2024, while LNG imports increased by as much as 32.3% (see Chart 1).

In 2025, Turkey also increased its spot LNG purchases. This mainly concerned imports from the United States, which rose significantly (see Chart 1) – from 5.59 buck in 2024 to 9.19 bcm in 2025, accounting for 10.7% and 15.9% of Turkey’s total gas imports, respectively.

Another change in Turkey’s gas market was the threefold increase in LNG supplies from other countries in 2025. Imports from these sources amounted to 1.15 bcm in 2024, compared with 3.5 bcm in 2025. In most cases, these are new suppliers, including Mozambique, Brazil, Senegal, Mauritania, Equatorial Guinea, and Nigeria. This demonstrates that Turkey is significantly diversifying its LNG procurement so as not to rely solely on the United States.

Despite the diversification of imports, the volume of gas supplied from Russia in 2025 remained at the same level as in 2024. According to data for 2025, Turkey purchased 21.16 bcm of Russian gas (a figure close to that of 2024 – see Chart 1).

Drivers of the shift

The sharp increase in LNG imports to Turkey is not merely the result of market conditions. Ankara deliberately seized the moment to gain significantly greater room for manoeuvre in renegotiating successive gas contracts with Moscow, while at the same time providing Washington with tangible evidence that it is ready to genuinely reduce imports of Russian raw materials – a condition the White House has set for improving bilateral relations.

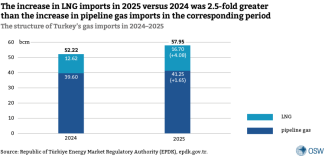

In the first instance, the increase in LNG imports was driven by market conditions. The growing availability of liquefied natural gas on the global market in 2025 enabled Turkey to opt flexibly for short-term purchase contracts. The decision to increase supplies also stemmed from rising domestic demand – a result of the stabilisation of the country’s financial situation and more intensive economic activity in both the private and public sectors.[1] Consequently, in 2025 Turkey imported 57.96 bcm of gas, compared with 52.2 bcm in 2024 (see Chart 2).

A key element behind the increase in LNG imports in 2025 was also Ankara’s strategic calculation vis-à-vis Moscow, aimed at revising the existing model of energy co-operation. Turkey deliberately took advantage of the growing availability of alternative gas sources to press Russia for more flexible contractual terms – including shorter contract durations and greater freedom regarding import volumes and take-or-pay mechanisms (a clause obliging the buyer to purchase a minimum quantity of the commodity or pay for unused volumes).

Thus, in December 2025 BOTAŞ extended its key contracts with Gazprom for pipeline gas supplies by only one year (until the end of 2026), maintaining volumes at around 21–22 bcm. The decision to adopt such a short time horizon – rather than traditional long-term commitments – sent a clear signal that Ankara does not wish to tie its hands with rigid agreements. At the same time, it demonstrated to Moscow that Turkey has viable alternatives to Russian gas.

Lastly, the shift in Turkey’s energy policy was also a direct consequence of pressure from the Trump administration, which has made the resolution of bilateral issues conditional on Turkey reducing its imports of Russian raw materials.[2] As early as September 2025, during the Gastech trade fair in Milan, BOTAŞ signed eight LNG contracts, which was intended as an initial signal from Ankara to Washington of its readiness to adjust its energy policy.

A problematic LNG hub

The sharp increase in Turkey’s LNG imports reflects its ambition to attain the status of a regional gas hub, importing natural gas from various sources and re-exporting it, primarily to European markets. In the long term, these ambitions appear achievable; however, at present the country lacks sufficient technical capacity to act as a large-scale re-exporter and largely remains a transit route.

The principal barrier remains limited transmission infrastructure between Turkey and Europe. The technical capacity of the key Malkoçlar–Strandzha interconnector (the reverse flow of the Trans-Balkan pipeline) is approximately 4 bcm annually. In 2025, 1.5–1.8 bcm had already been utilised (mainly for exports to Bulgaria), leaving only about 2 bcm of spare capacity – far too little for large-scale re-export of LNG surpluses. The Marmara Ereğlisi terminal (with regasification capacity of approximately 13 bcm annually) is constrained by this bottleneck, which currently prevents significant gas flows to Europe. In December 2025, Turkey’s energy minister announced plans to increase the capacity of this interconnector to 10 bcm annually; however, this will require substantial investment in gas interconnections as well as long-term gas demand guarantees from European customers – without which the expansion would not be economically viable.

Another challenge is that Turkey faces a shortage of storage capacity, which in practice precludes price arbitrage and the long-term storage of surplus gas for re-export. The current total capacity of underground gas storage facilities (Silivri and Tuz Gölü) amounts to 6.3 bcm, and plans to increase it to 14 bcm will not be completed until 2028.

This problem becomes particularly evident when compared with regasification infrastructure. Although the current capacity of LNG terminals and FSRU units amounts to around 51.3 bcm per year, their physical storage capacity remains marginal – only about 0.3–0.6 bcm in FSRUs and the aforementioned 6.3 bcm in underground storage. With LNG imports of 15.8 bcm in 2026 and rising domestic production from the Sakarya field (estimated by the Turkish side at around 7.3 bcm in 2026), Turkey currently lacks the buffer that would allow it to manage surpluses flexibly.

Iran: another disruption to the plans

Despite these challenges, Turkey will continue to pursue its ambition of becoming a regional gas hub, although these plans are likely to be delayed by the war with Iran. The current surplus of LNG imports provides Ankara with a safety buffer in the event of a disruption or reduction in gas supplies from Iran as a result of US and Israeli military action – in 2025, Turkey imported approximately 7.7 bcm from that country (around 13% of its total gas imports).

However, this surplus does not eliminate all risks. Although most LNG comes from secure sources (the United States, Australia, Norway, Algeria, and Oman), some contracts (including those with Shell, TotalEnergies, and Mercuria) involve, to varying degrees, supplies from the Persian Gulf region. A prolonged blockade of the Strait of Hormuz could lead to delays in their delivery. The situation is further exacerbated by the fact that gas available on the spot market is currently being urgently redirected to customers in East Asia, where prices are reaching record levels. Consequently, Turkey has much more limited opportunities to purchase additional supplies at attractive prices.

This indicates that, even with a diversified portfolio of contracts, Ankara may face difficulties inmaintaining full purchasing flexibility and generating LNG surpluses in the coming months, which – alongside existing infrastructural constraints – will delay its plans to become a regional gas hub.

Moreover, Russia will likely seek to take advantage of this situation to exert pressure on Turkey and push it into signing a new long-term gas agreement. The Kremlin is well aware that, amid a crisis in the Middle East, Ankara may seek stable and predictable supplies. This, in turn, will pose a challenge to Turkey’s efforts to reduce its gas dependence on Moscow, as well as to its policy towards Washington.

Table. Contracts for the purchase of LNG signed by Turkey, 2023–2025

2025 saw a significant increase in the number of contracts for LNG signed by Turkey

Map. Pipeline network and terminals in Turkey

Source: Republic of Türkiye – Ministry of Energy and Natural Resources, enerji.gov.tr; Energy Community, energy-community.org.; BOTAŞ, botas.gov.tr.

[1] See A. Michalski, ‘Turbulent stabilisation: Turkish economy under Şimşek’s supervision’, OSW, 9 July 2025, osw.waw.pl.

[2] See idem, ‘Turkey and the US: a costly normalisation’, OSW, 30 September 2025, osw.waw.pl.