Disappointing post-COVID-19 recovery. China on the path of a protracted slowdown

China’s economy started the year with a clear upturn after the ‘zero COVID’ strategy was lifted, but the macroeconomic data published in recent weeks has clearly fallen short of expectations. The situation has caused disquiet in Beijing and among those economists who expected the robust rebound to continue. In order to stimulate economic activity, the People’s Bank of China has made a slight cut to interest rates. Moreover, respected foreign media outlets have reported that the government is readying a stimulus package with investments in infrastructure as its core component. The aim of these slightly more expansionary monetary and fiscal policies is to bolster economic growth in the second half of the year, but their effectiveness will be limited. Low economic confidence among households and businesses remains a barrier to increased activity. China’s economy has entered a period of structural slowdown as it grapples with the cumulative costs of the rapid economic expansion over recent decades, deteriorating public sentiment and an unfavourable international environment. Beijing’s options for stimulating the economy are narrowing and the priorities are shifting: the imperative to boost GDP is giving way to economic security.

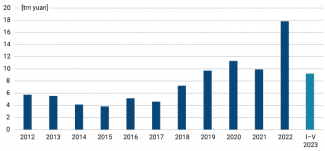

After China abruptly and unexpectedly ditched its ‘zero COVID’ strategy and went through a period of pandemic-related state dysfunction,[1] economic activity in the country started to pick up in the first months of this year. Beijing set a conservative GDP growth target of around 5% for 2023,[2] but both the government and foreign analysts actually expected the growth rate to be around one percentage point higher. In particular, they pinned their hopes on an upswing in consumption by households, which had reduced their spending and investments during the lockdown period. As a result, they had accumulated substantial savings (see Chart 1) which they could have spent on shopping or travel after the restrictions were lifted. Such an effect has been seen in other economies, including the US.

Chart 1. Rise in the value of household deposits between 2012 and 2023 relative to the end of the previous year

Source: data from the People’s Bank of China.

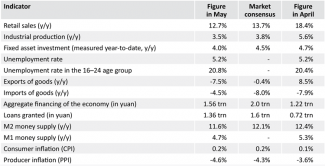

However, the key macroeconomic data for April, and particularly for May, turned out to be worse than what experts had forecast[3] (see Table). While retail sales rose by nearly 20% y/y in April and by more than 10% y/y the next month, it is difficult to make reliable assessments because of the low statistical base: the reference point for these figures is the period of suppressed economic activity resulting from numerous local lockdowns over the past year. In the two-year perspective, which allows us to eliminate the impact of this disruption, sales rose by just 2.5% y/y in May, the slowest rate since December. Similarly, industrial production grew 2.1% in May, slightly higher than the figure in April (1.3%), the month that saw the lowest growth rate since the outbreak of the pandemic. Before 2020, both sectors had reported significantly higher figures: near double digits for retail sales, and usually above 5% for industrial production. A low level of investment was also registered in May. Particularly noteworthy is the divergence between state-owned companies and those that are not directly controlled by the government. The former increased their outlays by 8.8% this year, while the latter reduced them by 0.1%.

Table. China’s key macroeconomic indicators in April and May 2023

Source: data from China’s statistics office, General Administration of Customs of the PRC, the People’s Bank of China and Reuters.

False hopes for a strong stimulus package

The disappointing data prompted a wave of revisions to forecasts for GDP growth this year (down to around 5.5%), alarmist articles in the international press, and calls for the government to shore up the economy. The People’s Bank of China responded in June with an interest rate cut of 10 basis points. Popular foreign media outlets reported that the government was preparing a stimulus package which would include the issuance of special treasury bonds worth 1 trillion yuan (about $140 billion) to finance investments in infrastructure, the first time this has been done since 2020. A relaxation of regulations restricting housing purchases was also mentioned among the potential solutions. This would represent a U-turn by the government in Beijing, which has sought to cool the real estate market through these restrictions in an effort to combat skyrocketing prices.

The scale of monetary easing has been modest so far, and it is also unlikely that there will be deep cuts in the cost of money in the coming months. The People’s Bank of China’s room for manoeuvre is limited by the low level of interest rates and the relatively restrictive policies of the world’s major central banks.[4] Most importantly, however, further minor rate cuts will not induce the Chinese people to tap into the excess savings they accumulated during the pandemic; nor will such cuts boost demand for credit, because the high cost of money is not the key factor that discourages consumption and investment. the path to faster economic growth in China is being blocked by low economic confidence – specifically, a lack of faith in a better future among households and entrepreneurs, and their growing fear of running into personal financial problems.[5] However, the government in Beijing can influence credit supply through alternative channels to standard monetary policy tools, such as recommendations for banks and control over large state-owned companies, but for the time being their effectiveness remains limited.

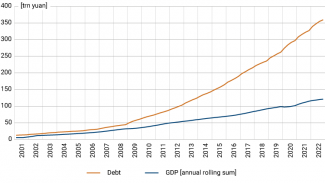

Faced with the ineffectiveness of monetary easing, the government must resort to fiscal expansion (increased public spending) in order to stimulate economic activity. Funding for investments in infrastructure from the issuance of special treasury bonds will sustain growth in the second half of the year, but it will also exacerbate the existing imbalances, as it will prop up the construction sector but not the economy as a whole. In recent years, all of China’s major stimulus programmes have been primarily geared towards stimulating activity through investments in the construction of real estate and infrastructure as well as the development of industry, which has led to rising debt, higher housing prices and overcapacity. The surge in debt over the past 15 years, from around 140% to over 300% of GDP for the non-financial sector as a whole[6] (see Chart 2), and the vivid memory of the programme that was carried out in 2008–10, which slipped out of Beijing’s control, have cooled expectations for a robust expansion.[7]

The very low inflation figures also attest to the modest recovery in the Chinese economy. Near-zero growth in consumer prices (CPI) along with a deeply negative change in producer prices (PPI) suggest that the economy was in deflation in the second quarter.[8] The falling prices in the economy have been driving down nominal incomes and causing a real increase in the value of debt, which further discourages new borrowing.

Chart 2. China’s GDP and the debt of the non-financial sector between 2001 and 2022

Source: data from the Bank for International Settlements and China’s statistics office.

Due to the low base effect, annual GDP growth will accelerate significantly in the second quarter compared to that recorded in the first three months (4.5%). In a speech at the World Economic Forum in Tianjin in June, Premier Li Qiang asserted that the 5% growth target for this year would be achieved. The goal set by the government is sufficiently conservative to be met without significant fiscal or monetary stimulation, not least due to the aforementioned low base. The disappointing recovery of the Chinese economy and its structural slowdown are currently helping to curb the global inflationary pressures faced by other countries, because China’s demand for raw materials is weaker than expected. However, the situation could change if Beijing decides to strongly stimulate the economy through investments in infrastructure while experiencing unsatisfactory consumption growth, which does not carry an equally pro-inflationary global impact.

The room for manoeuvre keeps shrinking

Faced with faltering growth, the Chinese government has less and less room for manoeuvre so it can boost growth without exacerbating the economy’s structural problems. According to media reports, the value of this year’s stimulus package is expected to reach a mere 1 trillion yuan (c. $140 billion), or less than 1% of the country’s GDP. By comparison, the stimulus after the global financial crisis, which helped China maintain its growth between 2008 and 2012, was worth more than 9 trillion yuan, or nearly 30% of its GDP at the time.[9]

The government in Beijing has so far refrained from significantly stimulating the real estate market, a key sector of the economy which accounts for around 25% of the country’s GDP and around 60–70% of its household assets. Following years of rapid price growth aided by strong speculative investment demand, housing prices in major cities have reached such heights that they are now a major barrier to increasing fertility and consumption. In addition, the debts incurred by property developers have risen dangerously. As mentioned above, in 2020 the government once again decided to cool down the real estate sector by limiting access to finance for companies in the industry and restricting the ability of potential buyers to purchase multiple housing units. The change of attitude on the part of the government and, consequently, the Chinese population has led to a steep decline in activity in the real estate industry[10] and a marked slowdown of the economy as a whole, as well as worsening sentiment among homeowners. Therefore, for the past few months, the government has been striving to stabilise this sector: it has agreed to lower mandatory contributions, facilitated access to housing funds and partially lifted restrictions on the purchases of investment properties. Nevertheless, housing sales by the country’s top 100 developers fell by more than 28% in June compared to last year, according to data from the China Real Estate Information Corporation. The government has been seeking to boost activity, but is resisting a return to a buying frenzy. Chairman Xi Jinping has insisted that ‘housing is for living, not speculation’. The anticipated slight relaxation of regulations restricting housing purchases will not change the attitude of potential investors.

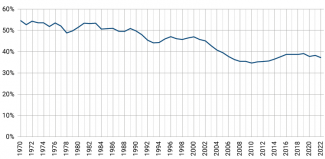

According to available information, the government in Beijing has no plans to employ a more expansionary fiscal policy to address low consumption. For nearly 20 years now, Chinese household consumption has remained below 40% of the country’s GDP (see Chart 3), compared to around 60% in Poland and over 70% in the US. This means that the Chinese economy is remarkably unbalanced, as it relies to an extraordinary degree on investment as well as exports. Meanwhile, the latest data indicates that private entities have been curtailing their investments, while foreign demand for Chinese-made goods has been weakening after four years of strong growth. The expected rebound in domestic consumption following the U-turn on the ‘zero COVID’ strategy has proved short-lived, which is reflected in low retail sales, sluggish growth in consumer prices and falling imports. Relatively slow growth in incomes (and even declines in many cases)[11], falling property valuations and record-high youth unemployment are contributing to the deteriorating public sentiment.[12]

Chart 3. Share of household consumption expenditure in China’s GDP between 1970 and 2022

Source: data from China’s statistics office.

Despite the current difficulties and the structural nature of the consumption problem, there are no indications at present that the government is planning to resolve it by implementing a more expansionary fiscal policy. For example, consumption could be stimulated through a reform of the social security system. The lack of an extensive network that would provide public services at a satisfactory level means that the Chinese population is obliged to save a significant proportion of their relatively low income to spend it on health care, retirement and their children’s education. However, devoting a significant percentage of resources to these purposes would run counter to the vision of a strong economy as espoused by Xi Jinping, who has publicly opposed building a ‘welfare state’ similar to Western solutions which, in his words, ‘promote laziness’.[13] Contrary to years of public statements, the government probably sees consumption as less beneficial than investments and manufacturing, as it does not directly lead to the creation of new assets – a tangible and durable effect of economic growth which testifies (sometimes superficially) to the prosperity and strength of the state. This is illustrated by the fact that previous stimulus programmes did not have any significant direct impact on the financial situation of domestic households.

The outlook: China’s economy in a structural slowdown

The Chinese economy is in the midst of a cyclical upswing within a structural slowdown. The economy has temporarily improved following the U-turn on the ‘zero COVID’ strategy, the adoption of measures to stabilise the real estate market, and the (now suspended) 2021 campaign against the consumer technology and education sectors. However, the overlapping costs of the rapid economic expansion of recent decades,[14] the fading effectiveness of the existing economic model, the deteriorating public sentiment and the unfavourable international environment are leading to a permanent slowdown in growth. The stimulus package in the form envisaged may give a slight boost to activity in the short term, but it will not solve the fundamental problems of the economy or permanently raise GDP growth to the levels that were seen in the past decade. The longer the Chinese government postpones the necessary reforms, the higher their economic and social costs will be.

GDP growth is no longer the main objective of Chinese economic policy or one of the primary criteria for promotion in the party hierarchy. Today, guaranteeing China’s security and stability is of paramount importance. In the area of the economy, this implies efforts to build a strong, modern industrial base to ensure self-sufficiency in the key sectors that are or could become the targets of US sanctions. At the same time, the government in Beijing wants to maintain its influence on its foreign partners by maintaining close economic ties with them. Xi Jinping has explicitly stated that the Chinese Communist Party (CCP) “cannot blindly pursue rapid growth regardless of objective laws and conditions” and must focus on “improving the quality of economic growth, promoting sustainable and healthy economic development, and pursuing genuine rather than inflated GDP growth”.[15] However, this does not mean that the government can completely ignore the issue of the level of economic activity: it has to be mindful of the difficult situation of those who are entering the labour market as well as the relatively slow growth of people’s incomes. An effort to balance the priorities of those in power and the financial interests of the elite and ordinary Chinese is a major challenge for the government in Beijing. The declining morale of the population, which stems from the deteriorating economic situation and prospects, is driving a change in the CCP’s strategy. The previous social contract, which involved a guarantee of rising prosperity in exchange for placing all political power in the hands of the party, is being replaced by the promotion of nationalist sentiment and the exercise of ideological control over society.

[1] See M. Bogusz, ‘China after its abrupt U-turn on the ‘zero COVID’ strategy’, OSW, 16 January 2023, osw.waw.pl.

[2] We should bear in mind the low credibility of the real GDP growth rate published by the Chinese statistical office. The main measure of the country’s economic health is a tool for the government’s internal and external propaganda, and is subject to manipulation. The indicator itself is quantitative rather than qualitative: the higher figures do not mean that the situation has improved.

[3] The so-called market consensus is determined on the basis of surveys conducted among analysts by Reuters and Bloomberg.

[4] In June, the yuan’s exchange rate against the dollar rose to above 7.2, its highest level in seven months. Compared to the broader CFETS basket of currencies, the Chinese currency is at its weakest since April 2021. Its depreciation benefits the economy in the short term as it boosts the competitiveness of domestic exporters; in the long term, however, it exacerbates the economy’s structural problems as it reduces the purchasing power of consumers. Furthermore, a sharp drop in the currency’s value could destabilise China’s financial system by encouraging capital flight from the country and hindering the process of yuan’s internationalisation.

[5] ‘Urban Depositor Survey Report (Q2 2023)’, the People’s Bank of China, 29 June 2023, pbc.gov.cn/en.

[6] This includes the government sector, non-financial corporations and households. Calculations based on data from the Bank for International Settlements.

[7] The factors of particular concern include the high debt of some local governments and affiliated entities (the so-called local-government financial vehicles), opaque networks of mutual loan guarantees, and unreported liabilities.

[8] This should be reflected in the negative value of the GDP deflator for this period.

[9] C. Wong, ‘The Fiscal Stimulus Programme and Public Governance Issues in China’, OECD Journal on Budgeting 3/2011, oecd.org.

[10] See J. Jakóbowski, ‘Bojkot kredytobiorców w Chinach i lokalne kryzysy bankowe’, OSW, 21 July 2022, osw.waw.pl.

[11] Those who have decided to cut salaries or even suspend payments include local governments that are struggling with high debts.

[12] In May, unemployment rate in the 16–24 age group was the highest on record in the few years in which data on this issue has been published. The news caused such public concern that the statistics office decided to release data on the nominal scale of the problem. The group of unemployed people aged 16 to 24 reportedly numbers around 6 million (33 million people in this age group are economically active; there are 96 million people aged 16 to 24 in China). The unemployment rate calculated by the Chinese statistics office is not directly comparable to similar rates published by institutions from developed countries as China defines an unemployed person in a different way and its statistics do not include domestic migrants who have returned from the cities where they used to work to their homes in the countryside. In addition, the media have reported numerous cases of graduates signing fictitious work contracts, as they need to demonstrate employment in order to receive their university degrees.

[13] ‘Full Text: Xi Jinping's Speech on Boosting Common Prosperity’, Caixin Global, 19 October 2021, caixinglobal.com.

[14] Some of the main costs of China’s rapid economic growth include high debt, internal and external imbalances in the economy, the inefficient allocation of capital resulting in lower productivity, very high housing prices, environmental pollution and low fertility rates.

[15] Xi Jinping, ‘Understanding the New Development Stage, Applying the New Development Philosophy, and Creating a New Development Dynamic’, Qiushi Journal, 8 July 2021, en.qstheory.cn.