The EU gas market: revolutionary changes and the spectre of another winter

The European Union survived last winter in a surprisingly effective way. Despite the ongoing gas crisis and Russia’s energy war with the West, there were neither painful shortages of gas or the need to ration it. This was the result of an exceptionally favourable set of circumstances: a warmer winter than usual in Europe and lower gas demand in China, and on the other hand, the actions taken by individual member states and the EU as a whole, as well as changes on the market.

2022 saw a revolutionary reshuffle in the directions and routes of gas supplies to the EU. Pipeline supplies from Russia, which used to be the largest source, fell by 56% year-on-year, while LNG supplies from the global market rose by 67%. Liquefied natural gas has become the most important source, and the EU has become the world’s fastest growing market for LNG, despite its long-term goals of achieving climate neutrality and reducing gas consumption. Unexpectedly, and contrary to the earlier assumptions of the European energy and climate policy, the construction of new gas infrastructure, including floating import terminals, has been stepped up. At the same time the EU’s demand for gas fell by a record 60 bcm (or over 13%) last year.

The market changes were supported by emergency regulations implemented at the EU level, such as the gas storage obligation and gas & energy saving targets. Some of the instruments agreed on (for example, concerning joint purchases of gas or the option of setting price limits on exchanges) involve allowing market interventions, which until recently would have been unimaginable in the EU.

As a consequence, storage facilities across the EU remained full to significant extent after the winter, and gas prices on EU exchanges have been falling since the beginning of 2023; in the second half of May they were below €30/MWh. This has had a calming effect on the markets and at least some of the decision-makers, and has provided the impetus for increasing consumption.

However, the sources of challenge and uncertainty have not disappeared, and according to all forecasts, the next winter may be much harder than the last one. Russia’s war with Ukraine continues, and tensions between Russia & the West continue unabated. Therefore, in all likelihood Russian gas supplies will be much lower this year than last year. At the same time, global competition for LNG is expected to intensify. As a result, the EU needs, on the one hand, to maintain its previous discipline and refine its crisis response instruments, while on the other ensuring the solidarity and cohesion of Union-wide actions. In particular, it seems necessary to develop a common EU policy on gas imports from Russia, something which does not yet exist.

The war and the reduced supplies from Russia

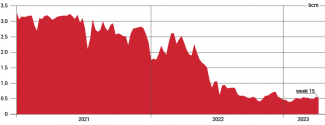

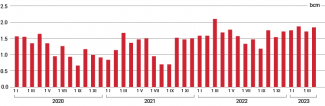

The rapid cut in Russian gas supplies was the key factor which aggravated the gas crisis in Europe and caused the unprecedented rises and volatility of prices on the exchanges. This was already visible in the second half of 2021, but it clearly accelerated after the outbreak of the full-scale armed conflict in Ukraine. On top of this, Russia used gas supplies as an instrument in the ongoing economic war with the West. In 2021, Gazprom stopped selling gas through exchanges, and as of the end of April 2022 it also reduced the volumes it had been delivering under the existing contracts. Initially, this move affected companies and EU countries which did not want to settle accounts in accordance with the requirement, implemented unilaterally by the Russian side, to pay for gas according to the rouble scheme. Those who accepted the scheme were also affected by it later on. In 2022, in addition to the cut in gas supplies via Ukraine, transmission via the Yamal-Europe and Nord Stream 1 gas pipelines was discontinued completely, while transport via the TurkStream route continues. Russia is currently only sending about a sixth of the fuel via gas pipelines to Europe that it did on average in the first half of 2021. However, since autumn 2022 the level of gas flows has remained relatively fixed. Preliminary estimates indicate that throughout last year they reached approximately 67 bcm, which means a decrease of around 56% compared to the previous year. On the other hand, supplies of Russian LNG increased by over 35%, to around 19 bcm.[1]

Chart 1. Russian gas transport to the EU via gas pipelines in 2021–2023

Source: European natural gas imports, Bruegel Datasets, bruegel.org.

Chart 2. Russian LNG imports via EU countries in 2020–2023

Source: ICIS, author’s own calculations.

As a result, total Russian gas exports to the EU reached around 86 bcm in 2022, and according to the International Energy Agency (IEA), they were at their lowest since the 1980s.

The crisis and the rising gas prices

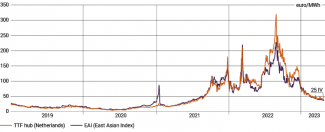

The drop in supplies from Russia resulted in a sharp reduction in the availability of natural gas in Europe and on the global market. This made the market less flexible. Uncertainty about the future of Russian gas exports was also associated with the risk of gas shortages, especially in winter. This, coupled with uncertainty about the weather and the availability of alternative sources, fuelled anxiety, deepened the crisis on both European and global markets, and provoked increasing competition for those limited volumes of uncontracted gas which were still available, which led to an increase in prices and their volatility. Record-breaking spikes occurred on European hubs. The further increases were largely linked to Russian moves: initially the outbreak of the war, and then to cutting the flows via successive routes, up until the suspension of exports via Nord Stream 1. The prices in monthly forward contracts reached their highest level (over €315/MWh) at the end of August 2022. As storage sites throughout Europe filled up and the volumes of Russian flows stabilised at the current low level, prices began to fall. Mild declines have been visible since the beginning of 2023. At the end of May 2023, the prices on the TTF exchange are below €25/MWh.

Chart 3. Dynamics of gas futures (monthly) prices on the TTF exchange (Netherlands) and East Asian LNG prices (East Asian Index) in 2019–2023

Source: ICIS.

The rapid changes on the European market influenced the situation on other global hubs. The Asian market followed the EU trends especially closely. As a result of the war and the deepening crisis, LNG prices in Asia fell below those in the EU for the first time in years; at the end of August 2022 they reached a record level of below €230/MWh. At the same time, as the situation on the markets has stabilised and the prices in recent weeks have been falling, the spread between European and Asian stock exchanges have been decreasing, which may lead to more intense competition in 2023.

European crisis management

The crisis, the record prices and the energy war with Russia made the member states and the European Commission take several emergency measures to manage the market in times of challenges and minimise the negative effects of the crisis. The moves and regulations implemented by the EU were largely temporary. They started with the REPowerEU document, which called for the Union to phase out its dependence on Russian oil & gas and accelerate the energy transition to this end.[2] In the case of the natural gas market, these actions were intended to have the following effects:

- phasing out imports of Russian gas and replacing them with imports from alternative sources & other energy carriers (including by stepping up the energy transition),

- increasing energy security by building up sufficient gas stocks,

- reducing consumption, and

- reducing price volatility & levels and their impact on the prices of other energy carriers & electricity.

Diversification

Diversification efforts across the member states and the EU as a whole were stepped up to an unprecedented scale in 2022. This was triggered by the real need to replace the declining supplies from Russia, and also by the fact that the governments had come to realise how dependent and vulnerable to weaponisation of gas supplies their countries were, and they no longer wanted to finance the aggressor state. In REPowerEU, the European Commission set out the goal of ending imports of Russian natural gas by 2027. EU countries and companies have been signing new contracts: for example, Italian companies struck deals with contractors in Algeria and Congo, Germany signed contracts for LNG supplies from the US and Qatar, as did Poland’s PGNiG with Norwegian and American companies, and Romanian companies with Azerbaijan’s SOCAR. At the same time, they were also building infrastructure to allow for increase in imports of non-Russian gas; these were mainly FSRU terminals, including new units commissioned in 2022 in the Netherlands, Finland and Germany.[3] Numerous long-forgotten projects were revived on this occasion, such as the Trans-Caspian Gas Pipeline, which is expected to allow the import of gas from Turkmenistan to the EU or Central European connections (their new version is the so-called Solidarity Ring).[4] Work has also started on strengthening energy cooperation with key partners at the EU level, for example with the US,[5] Norway, Azerbaijan and Egypt.

As a consequence of all these steps, the routes and sources of gas supplies (including LNG) to Europe – and also on the global scale – were reshuffled in 2022. Last year, Europe became the fastest growing market for liquefied gas imports, a trend which is expected to continue in 2023. At the same time, due to the limited increase in gas supply worldwide[6] and the challenge posed by the very high prices on the hubs, this has involved limiting access to global LNG for third countries (including Pakistan, Bangladesh and Thailand).[7]

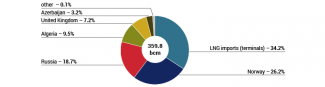

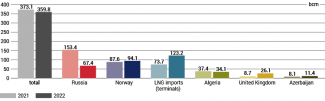

Norway became the largest exporter to the EU in 2022; deliveries from this country accounted for 26% of extra-EU imports, a rise of over 7% compared to the previous year. However, LNG has become the most important external source of gas on the EU market, now representing more than a third of external purchases. Imports of liquefied gas (including Russian) rose by over 67% y/y in 2022.[8] The US, which accounted for around 55% of non-Russian LNG imports to the EU, was the most important supplier of LNG.[9] US exports to Europe rose by 141% compared to 2021, according to the US Energy Information Administration. LNG deliveries from Qatar, Egypt, the United Kingdom and Azerbaijan also increased, albeit to a lesser extent. On the other hand, according to preliminary data, the volumes of gas supplied from North Africa decreased, and the EU’s own production also fell (by over 7%).[10]

Chart 4. Source of gas imports to the EU in 2022

Source: Bruegel Datasets (Azerbaijan – data from media reports).

Chart 5. Changes in gas imports via the EU from individual sources in 2021–2022

Source: Bruegel Datasets (Azerbaijan – data from media reports).

Falling demand

The revolutionary changes in gas supply have been coupled with unprecedented changes in demand on the EU market. Preliminary Eurostat data shows that gas consumption in the EU dropped by almost 60 bcm in 2022, i.e. by 13.2%, compared to the previous year.[11] This was probably the biggest drop ever. It was caused by a number of factors:[12] the first is high prices, which translated into both savings and the destruction of demand in industry, spreading energy poverty, and switching part of electricity production to alternative sources; for example, according to IEA estimates, the gas-to-oil switch in the European industrial sector allowed around 7 bcm to be saved.[13] The warmer winter, and consequently the lower demand for gas for heating and electricity production purposes, also had a great impact. According to the IEA’s data, consumption was at least 18 bcm lower as a result of this. Last but not least, renewable sources were used more intensely. Since solar and wind power plants gained an additional capacity of 50 GW as a result of new installations, this allowed about 11 bcm of gas to be saved, according to the IEA.

Gas consumption has fallen, both in response to market conditions and as a result of the implementation of emergency policy measures; these include the temporary target adopted by the EU of reducing demand in the heating season (from August 2022 to March 2023; the target has been extended to March 2024) by 15%. This target was even surpassed, as demand actually fell by almost 18%. Many EU countries reduced consumption by much more than the figure assumed for the whole of 2022: Finland by almost 48%, Sweden by over 42%, Lithuania and Latvia slightly below 30%. However, last year gas consumption did increase in some countries: in Ireland by over 2% and in Malta by 1.2%. Seven member states did not achieve the agreed consumption reduction level during the heating season.[14]

Filling up storage facilities

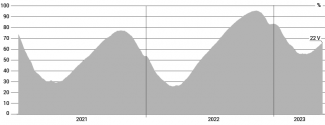

Despite the war and the challenges posed by the limited availability of natural gas, the member states managed to fill gas storage facilities in accordance with the EU-adopted emergency regulation, and also thanks to the measures taken to limit demand. A record-breaking 70 bcm of gas was needed for this,[15] as the levels in the storage sites were extremely low[16] after the previous heating season, and the storage facilities whose owner and/or main user had been Gazprom (including the EU’s second largest storage facility in Rehden) were practically emptied. Also in this case, last year’s target of 80% was exceeded; in November 2022, EU gas tanks were filled to an average of over 95%. This year, given the relatively mild winter and limited demand, the heating season in Europe ended with relatively large stocks: the gas storages were still over 55% full at the end of March.[17]

Chart 6. The European Union’s gas storage levels in 2021–2023

Source: GIE, AGSI+.

Prices and market interventions

The measures to reduce the high prices and their negative impact on EU gas consumers were taken at the level of individual member states, largely in accordance with the recommendations of the European Commission and the ‘toolbox’ originally published in autumn 2021. As a result, they took various, often uncoordinated forms: tax cuts and reliefs, limits of final gas & energy prices and subsidies (these were applied in many EU countries; for example, in Germany under a huge aid package worth €200 billion was implemented), subventions reducing energy bills for the most vulnerable customers, or measures limiting the impact of gas prices on electricity prices (by introducing caps on the prices of gas used for electricity production in Spain and Portugal). The great variety of instruments and the different levels of subsidies & support mitigated the social effects of the crisis, but also led to a change in the situation on national markets and a certain disturbance to the ‘level playing field’ and the overall operation of the common EU market. This was clearly seen in Spain and Portugal, where unlike the rest of the EU, the electricity sector ceased to respond to the price incentives to reduce gas consumption.

In parallel to the initiatives on the member-states level during 2022, work was underway on pan-European solutions intended to achieve two things: first, to increase purchasing power, and thus the possibility of negotiating attractive contracts by the dispersed recipients; and second, to make it possible to reduce prices and limit their volatility on wholesale markets, and to curb manipulation on the hubs. Despite major controversies inside the EU, the member states agreed, for example, to create two previously unthinkable instruments to ensure security of supply and enable de facto intervention in the operation of the common market. Since these were still being developed until the end of last year, their possible effects and operation in practice will only become apparent in 2023.

Firstly, the EU Energy Platform was created to enable the aggregation of EU demand and joint gas purchases. The aggregated volumes must correspond to 15% of the volume needed to fill the storage facilities (around 13.5 bcm across the EU). Above this level, voluntary aggregation of demand is possible.[18] The platform was inaugurated in April 2023. According to the results announced in the second half of May, the first tender was successful. It managed to procure more gas than reported demand, including for recipients in the countries most exposed to shortages, such as Bulgaria and Ukraine. However, the final supply contracts are to be negotiated and concluded outside the platform during bilateral talks.[19]

Secondly, overcoming the huge differences between the member states made it possible for them to agree on a market correction mechanism (MCM) designed to limit prices on the EU’s wholesale markets (hubs) in strictly defined cases. These will be imposed if the gas price of monthly futures on the TTF hub exceeds €180/MWh for three consecutive days while at the same time remaining at least €35 higher than the reference LNG price on global markets. Given the current situation and the MCM provisions (under which its operation can be suspended in the event of a negative impact on the operation of the EU gas market, including the security of supply and/or transmission of gas in the EU), it is not clear whether this limit will ever be applied.[20]

Questions about next winter and Russian gas imports

The numerous measures the EU has taken have been successful, but what really helped with surviving the last heating season without major sacrifices were the unexpected and independent from the EU circumstances: a relatively warm winter (the temperatures recorded in Europe were on average 1⁰C higher than usual, and even 2.5–4⁰C higher in the case of Central and Eastern Europe)[21] and the reduced demand for gas in Asia, primarily in China, as a result of pandemic restrictions. However, the coming winter will in all likelihood be more challenging.

Firstly, we cannot expect that the weather will be equally favourable and that temperatures will again be higher than in the previous seasons. The El Niño phenomenon is expected to intensify in the second half of the year,[22] so the coming winter in the northern hemisphere may be colder than usual (and the summer may be hotter). This would most likely raise demand for gas in Europe (and beyond) for heating purposes. Secondly, the economic recovery in China entails a higher demand for energy, including gas. Given the limited increase in the supply of natural gas on a global scale, competition will intensify, especially on the LNG market. Thirdly, the EU remains vulnerable to Russian gas manipulations. Russian gas supplies to the EU this year are likely to be significantly lower than last year: until the end of April 2022, Gazprom supplied gas in accordance with the contracts it had signed with EU contractors. If Russia maintains the level of exports to the EU at that of recent months, gas pipeline supplies in 2023 will amount to about 30 bcm, or about 60% (or almost 40 bcm) lower than a year ago. At the same time, since the current restrictions on exports from this country are mainly the result of Moscow’s policy, it cannot be ruled out that they will fall further (in the worst-case scenario, to zero). Russia may also increase supplies to some entities and/or countries who are willing to compromise with it on this issue, and to achieve benefits similar to those enjoyed by Hungarian and Serbian entities.

As a consequence, despite the persistently low prices and the calmer situation on the market, a large part of the existing ‘emergency’ instruments should be maintained, and countries & societies should be prepared to operate in a quasi-crisis mode. The European Commission has extended the target of reducing gas consumption by 15% until the end of March 2024, new gas sources are being sought, and negotiations of further contracts are being conducted in the light of the risks associated with another winter and the energy war with Russia. EU entities can also conclude contracts using the recently launched mechanism for joint gas purchases, which is primarily intended to facilitate the filling of EU storage facilities. One of the most important goals in current market conditions should be to avoid any slowdown of this process.

It is also important to increase the availability of alternative energy & heat sources within the next two years, and to further diversify gas suppliers. This should involve counteracting the slowdown in implementing the necessary regulations and the construction of the necessary transmission (this especially concerns south-eastern Europe, but also applies to north-western Europe along the west-east axis), storage (for example, by increasing the capacity of the Chiren tank in Bulgaria) and import infrastructure. The option of generating electricity in the EU using fuels other than gas (including renewable, but also coal and nuclear sources, which are controversial and/or unwanted in many EU countries) should not be forgotten either.

Finally, it will be crucial not only to prevent the weaponisation of gas supplies, but also to maintain cohesion and solidarity among EU member states, by developing and implementing a common and unambiguous policy regarding the import of Russian gas – both via pipelines and in the form of LNG. In the optimal scenario, this would not only limit Moscow’s ability to play off the interests of individual states and EU entities against each other, consequently weakening the unity of the EU, but would also further reduce the Kremlin’s influence on the common market (including prices) and Russia’s export income.

[1] The figures in this paragraph are quoted from B. McWilliams, G. Sgaravatti, G. Zachmann, European natural gas imports, Bruegel Datasets, 17 May 2023, bruegel.org.

[2] For more detail, see A. Łoskot-Strachota, ‘The EU gas market and policy and the war in Ukraine’, OSW Commentary, no. 430, 11 March 2022, osw.waw.pl.

[3] See M. Kędzierski, ‘At all costs. Germany shifts to LNG’, OSW Commentary, no. 510, 28 April 2023, osw.waw.pl.

[4] See K. Całus, K. Dębiec, I. Gizińska, Ł. Kobeszko, A. Łoskot-Strachota, A. Sadecki, ‘Solidarity Ring: a step towards increasing Azerbaijani gas supplies to Central Europe’, OSW, 11 May 2023, osw.waw.pl.

[5] A. Łoskot-Strachota, ‘The EU’s strategic energy partnership with the US after a year of war’, OSW, 6 April 2023, osw.waw.pl.

[6] According to the IEA, LNG supply rose by 5.5% in 2022; see Gas Market Report, Q1 2023, including Gas Market Highlights 2022, February 2023, iea.org.

[7] According to IEA data, demand for gas in these countries fell in 2022 by 18%, 17% and 10% y/y, respectively.

[8] Calculation based on European natural gas imports, op. cit.

[9] That is, around 56 bcm; author’s own calculations based on data from the US Energy Information Administration: U.S. Natural Gas Exports and Re-Exports by Country, 28 April 2023, eia.gov.

[10] See Natural gas supply statistics, Eurostat, April 2023, ec.europa.eu.

[11] Based on Supply, transformation and consumption of gas – monthly data, Eurostat, 23 May 2023, ec.europa.eu and the author’s own calculations.

[12] For more detail, see A. Łoskot-Strachota, ‘EU: record drop in gas demand in 2022’, OSW, 23 March 2023, osw.waw.pl.

[13] The estimates quoted here and below are based on P. Zeniewski, G. Molnar, P. Hugues, ‘Europe’s energy crisis: What factors drove the record fall in natural gas demand in 2022?’, IEA, 14 March 2023, iea.org.

[14] These were Malta, Ireland, Slovakia, Spain, Poland, Slovenia and Belgium. See ‘EU gas consumption decreased by 17.7%’, Eurostat, 19 April 2023, ec.europa.eu.

[15] See G. Molnar’s post on LinkedIn, February 2023, linkedin.com.

[16] They were around 25% full at the end of March 2022.

[17] Data as on the website Gas Infrastructure Europe, Aggregated Gas Storage Inventory, agsi.gie.eu.

[18] See A. Łoskot-Strachota, ‘The EU steps up work on joint gas purchases’, OSW, 26 January 2023, osw.waw.pl.

[19] ‘EU Energy Platform: EU attracted over 13.4 bcm of gas in first joint gas purchasing tender’, European Commission, 16 May 2023, energy.ec.europa.eu.

[20] See A. Łoskot-Strachota, ‘UE: trudna zgoda w sprawie limitów cen gazu’, OSW, 23 December 2022, osw.waw.pl.

[21] See Europe in 2022. Temperature, Climate Change Service, The Copernicus Programme, climate.copernicus.eu.

[22] See, for example, C. Elton, ‘There’s a 90% chance El Niño will hit this summer. What does it mean for extreme weather?’, Euronews Green, 16 May 2023, euronews.com/green.