A dangerous resemblance. Moves to revise Germany’s China policy

Russia’s invasion of Ukraine has revived the ongoing discussion in Germany regarding the need to revise its policy towards China. Until recently, the course Berlin adopted towards Beijing and Moscow was not only convergent in many aspects, but also enjoyed a consensus among the Christian Democrats and the Social Democrats, who co-formed three government coalitions from 2005–2021. This resulted in the emergence of a dependence that was unfavourable for Germany. With Russia this involved the import of fuels and with China it involved supplies of components and also major investments carried out by German companies in China. Both states were viewed as priority partners, frequently at the cost of relations with other countries in Central and Eastern Europe and the Indo-Pacific, respectively. Berlin’s approach to Beijing and Moscow sparked disputes with its closest allies as well as dilemmas regarding Germany’s economic and security interests. In addition, cooperation with authoritarian regimes that violate human rights was a blot on Germany’s image in the context of its foreign policy.

Due to the scale of Germany’s economic dependence on China, it may be assumed that a potential conflict between the US and China and the associated disruption of supply chains would have even more serious consequences for Germany than the energy crisis following the Russian attack on Ukraine. Although the ongoing war is unlikely to provoke a sudden change in Berlin’s policy towards Beijing, it may accelerate the revision already underway. In this process, the biggest problem involves the evident divergence between the position adopted by the government – in particular those of its members who represent the Green Party – and that promoted by the business community, which is reluctant to change in this regard.

Pragmatism above all

Since the establishment of diplomatic relations in 1972, Germany’s policy towards China has mainly been shaped by the conviction that, in order to maintain cooperation, Berlin needs to come to terms with the different nature of its partner’s political system. At the same time, the economy continued to be the basis of the relations between the two countries because it was viewed as the least controversial sphere and as the starting point for expanding bilateral cooperation into other fields such as culture and science. As a consequence, Berlin accepted such elements of China’s political system as the “One China” policy, and respect for human rights was treated as a topic of secondary importance mainly raised during bilateral talks without the participation of journalists.

The meeting between Angela Merkel and the Dalai Lama in 2007 (this was the first ever meeting between a German chancellor and the Dalai Lama) and Chancellor Merkel’s absence from the 2008 Summer Olympics opening ceremony in Beijing were an attempt to abandon this practice. These decisions triggered a crisis in bilateral relations that put the German economy at risk (at a time when it had already been weakened by the financial crisis) and ended when the German ministry of Foreign Affairs (MFA) sent a letter to the Chinese leadership in which it confirmed that it viewed Tibet as a part of China.

In line with the assumptions adopted by consecutive German governments, Berlin’s dialogue with Beijing was intended to facilitate the pursuit of Germany’s interests worldwide. As a result of China’s increasing economic importance to Germany and its political influence, the “China first” principle was devised based on the intention to treat China as Germany’s key partner in the Indo-Pacific region. This involved, for example, attempts to avoid adopting a clear stance on regional territorial disputes. The almost yearly visits paid by German government heads to China and by representatives of the Chinese leadership to Germany almost since 2000 were symbols of intensive bilateral cooperation. In June 2011, these visits were transformed into regular intergovernmental consultations held biannually. As a consequence, China became the seventh country to be included in the small group of states participating in this mechanism (at present it has 11 members and in 2023 it will be joined by Japan).[1]

Germany’s economic dependence

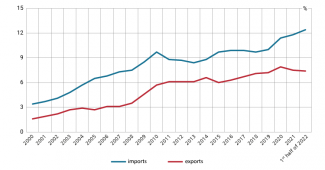

In the second decade of the 21st century, due to German companies’ growing interest in expanding their operations in China and the development of bilateral trade, Germany’s economic dependence on China increased. Although the COVID-19 pandemic showed that locating manufacturing activity in a country with an unstable political and economic situation generates a serious risk to efficient supply chains, it failed to reverse this trend. In the first half of 2022, the value of trade exchange between Germany and China stood at 148 billion euros (9.9% of Germany’s global trade) and increased by 50% compared with the corresponding period in 2019. Since 2016, China has been Germany’s biggest import partner and its second biggest export partner after the US. At the same time, China accounts for Germany’s biggest trade deficit – in 2021 it stood at almost 36 billion euros.

Furthermore, Germany largely depends on China when it comes to the import of raw materials that are of major significance to the development of new technologies. These include lithium (75% of Germany’s imports) and rare earth elements (45%).[2] China’s share in the turnover recorded by some German companies – in particular in the automotive sector – is more than 33%.[3] Considering the fact that China accounts for a major share of profits generated by companies listed on the Frankfurt stock exchange, potential conflicts with Beijing pose a risk to the German financial system, as do China’s internal economic problems (see Appendix).

However, these trade figures do not reflect the quality-related spectrum of Germany’s economic dependence on China. The import of components is one element of this dependence. According to a report compiled by the Munich-based Institute for Economic Research (ifo), 46% of German industrial companies and 40% of companies trading in components purchase these components from China. This refers in particular to large companies (56%), of which 16% manufacture the components they need in their own manufacturing plants located in China. The automotive (75.8%), computer (71.6%), electrical (70.6%), textile (64.8%) and furniture (64%) industries are the most dependent on the purchase of components. Furthermore, China accounts for the production of 7% of components assembled in countries such as Poland and Slovakia and later used in final production processes in Germany.[4]

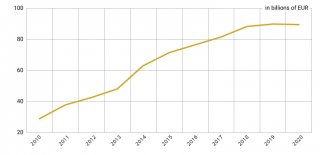

Another element of Germany’s dependence on China involves investments carried out by German companies in China. According to data contained in a report published by Rhodium Group, in 2021 these investments accounted for 46% of all European projects (carried out by the EU and the UK) in China, and in the last four years the average proportion was 44%. The authors of the report argue that the reasons behind this situation include the fact that German companies had entered the Chinese market earlier, and also the German government’s moves to encourage investors to launch subsequent projects in China. German investors mainly include large companies: in 2018–2021 the automotive companies Volkswagen, BMW and Daimler, and the chemical sector giant BASF accounted for 34% of European direct investments in China.[5]

Dangerous competition

China’s economic activity generates problems for Germany’s security policy. Research carried out by the Kiel Institute for the World Economy indicates that Chinese businesses take over German companies in order to acquire technology rather than to generate profit. These takeovers happen mostly in the automotive, medical technology, digitisation and robotics industries. These activities are elements of the “Made in China 2025” strategy that defines development goals in ten domestic high technology industries, the achievement of which is expected to increase these industries’ global competitiveness. Investments in foreign companies operating in these areas are one element of this strategy.[6]

Germany is a centre of interests for Chinese investors – in 2000–2021 it was ranked second in terms of the accumulated value of Chinese investments in Europe with 30.1 billion euros.[7] According to a report compiled by EY, in 2021 Germany saw at least 35 Chinese investments or takeovers worth a total of 2 billion euros (in 2020 there were 28 such initiatives worth a total of 0.4 billion euros). The three biggest projects carried out with the participation of Chinese businesses involved online platforms.[8]

A report compiled by the Federal Office for the Protection of the Constitution in 2021 lists China – alongside Russia – among the states with the most advanced spying activity in Germany. This activity focuses on acquiring information on the Bundeswehr and its armaments.[9] In addition, Chinese special services fight Chinese dissidents residing in Germany, and the Chinese diaspora is involved in spreading the Chinese state’s official propaganda. Furthermore, German counterintelligence argues that the activity of the 19 offices of the Confucius Institute that operate at German universities and funded by Beijing poses a risk to academic freedom. Another problem faced by Germany involves the fact that the Chinese armaments industry is using dual-use technology developed under projects implemented jointly by German and Chinese universities.

Moreover, China has been involved in activities that undermine the rules of free trade and the democratic state model promoted by Germany, which makes it a systemic rival. Due to export loans offered by the state and the fact that Chinese businesses fail to observe investment standards, Chinese companies are more likely to obtain contracts in Asian, African and South American countries. Unlike in the EU, a specific company may receive financial assistance regardless of whether its target investment state meets the democratic, environmental and profitability standards in the context of the planned projects. Furthermore, it is through loans that China is expanding its influence in the EU’s immediate neighbourhood. According to a report compiled by UniCredit, in 2020 Chinese loans accounted for as much as 3.4% of the GDP of Bosnia and Herzegovina, for 7% in Serbia, 7.5% in North Macedonia and 20.7% in Montenegro.[10] Beijing’s attempts to achieve military and economic domination in the Indo-Pacific region pose a threat to the security of local maritime trade routes used for transporting German-made goods.

Concealing inconvenient decisions

Amid growing economic dependence on China, Germany has increasingly faced a dilemma whether to maintain good relations with its largest trading partner or to protect its own economic and security interests. In order to respond to the changing situation, Berlin is implementing mechanisms to restrict the activity of Chinese businesses in selected areas. These restrictions simultaneously cover a bigger group of states, which is intended to show that they are not directed solely at Beijing. One example of this modus operandi involved the cancellation of the initial decision to allow Huawei and ZTE to take part in the construction of the German 5G network, which had provoked a crisis between Germany and the US.[11] Finally, as a result of cross-party opposition to the government’s initial plans, in April 2021 the Bundestag decided to amend the initial wording of the law on 5G to make it more restrictive; according to the new regulations there was likely sufficient risk to public order and security from the network’s critical components for these companies to be excluded from the project.

A similar practice was used regarding the legislation on foreign direct investments. In response to the Midea Group purchasing a majority stake in the Germany’s Kuka (a manufacturer of industrial robots) and the risk of possible further Chinese takeovers in the German high technology sector, starting from 2017 the then Federal Ministry for Economic Affairs and Energy introduced three amendments to the regulations on auditing foreign investments. For example the list of sectors subject to this audit was expanded and a requirement was imposed for companies operating in critical sectors (such as energy infrastructure) to report instances of non-EU and non-EFTA companies taking over at least 10% of their shares.

Another method used by Berlin involves dealing with controversial issues as part of the EU’s policy. On the one hand, this enables Germany to avoid being accused of pushing through its own interests, and on the other – it dilutes responsibility for decisions that could potentially undermine its relations with Beijing. In 2020, during the final days of Germany’s EU Council presidency, as a result of Berlin’s efforts an investment agreement was signed between the EU and China, despite reservations communicated by some EU member states. In May 2022, the EU withheld the ratification of this agreement when, in response to EU sanctions imposed against four individuals and one public institution, who had been involved in human rights violations in Xinjiang, China introduced much tougher personal restrictions targeted at several dozen individuals and institutions from the EU, including German MEPs and think tanks.

China recently introduced restrictions in its trade with Lithuania in response to the opening of the Taiwanese Representative Office in Vilnius; this is another example of problems related to Germany’s economic dependence on China. From Berlin’s perspective, this move jeopardised the supplies of high-tech subassemblies manufactured in Lithuania by German companies, which are then exported to China.[12] In response to this, the EU filed a case against China at the WTO and approved a Lithuanian aid package worth 130 million euros targeted at companies that had suffered losses due to Chinese restrictions.

A slow strategy revision

So far, the SPD-Green-FDP government has not taken steps to radically change Germany’s policy towards China. However, at the level of its representatives’ declarations and rhetoric, a certain readiness is noticeable to revise the rules that until recently determined Germany’s relations with China. A passage from the 2021 coalition agreement regarding China is more confrontational in nature than a similar fragment of the agreement signed by the CDU/CSU and the SPD back in 2017.

The new government intends to base its policy on China on two pillars. The first one is collaboration within the EU. In the document, the coalition partners followed the example set by the European Commission and listed three dimensions of Germany’s relations with China: cooperation based on respect for human rights and international law, competition based on “fair play”, and systemic rivalry. In addition, the new strategy devised by the German MFA is to be put in the framework of a joint EU policy. The second pillar is the alliance with the US. During her visit to New York in August 2022, Germany’s Foreign Minister Annalena Baerbock (Greens) reiterated her intention to “seek a more specific trans-Atlantic agreement regarding the policy towards China”.

Another manifestation of Berlin’s increased readiness to confront Beijing involves the fact that the coalition agreement lists problematic issues in bilateral relations – these include the reduction of strategic dependences and the resolution of territorial disputes in the South China Sea and the East China Sea based on the law of the sea and also of tensions in the Taiwan Strait on the basis of a peace agreement. Furthermore, the document explicitly mentions the issue of human rights violations happening in China, in particular in Xinjiang, and Germany’s support for the observance of the “one country, two systems” principle in Hong Kong.

A change in Germany’s policy towards China includes the decision to abandon the “China first” principle, which is evident in the fact that a separate paragraph of the agreement has been devoted to the Indo-Pacific region. The government’s plans on the region are convergent with the goals and tools mentioned in the strategy published in 2019. The initiatives include increased collaboration between the EU and ASEAN, as well as intensified bilateral parliamentary cooperation with Australia, New Zealand, Japan and South Korea. In 2023, Germany also intends to develop its strategic partnership with India. Japan has a special place in the policy of the coalition partners, which is why it was the destination of the first visit to Asia paid by Chancellor Olaf Scholz and the Foreign Minister, Mrs Baerbock.

In response to expectations from the United States regarding increased allied involvement in stabilisation efforts in the Indo-Pacific region, the German government is continuing the actions launched by the CDU/CSU and SPD cabinet which in 2021 decided to send the Bayern frigate to the region. In 2022, Germany decided to dispatch six Eurofighter jets, four transport aircraft and three tanker aircraft to take part in the Rapid Pacific 2022 exercise. In 2023, it plans to send Bundeswehr soldiers to participate in drills in Australia, and in 2024 it will send several warships to the Indo-Pacific. The G7 states (Germany is holding the G7 presidency in 2022) intend to make a facility worth US$ 600 billion available for the implementation of infrastructural projects in the region’s states until 2027; this is an attempt to create an assistance mechanism targeted at developing states that would be an attractive alternative to what China offers.

Another strategy to reduce Germany’s dependence on China is being devised by the government under the supervision of the MFA. The Federal Ministry for Economic Affairs and Climate Action headed by Vice Chancellor Robert Habeck (Greens) is also involved preparing this document. According to information reported by the media, Mr Habeck intends to reduce the guarantee mechanisms offered to German companies for their foreign investments. Due to the fact that security guarantees are extended every couple of years, the new mechanism would not only cover new projects, but also the initiatives currently being implemented. The ministry’s plans would mainly affect companies interested in doing business in China–at present guarantees offered to projects carried out in China are worth 11.3 billion euros (38% of the value of all allocated guarantees). This is intended to encourage businesses to boost diversification of their investment activity. Another development suggesting that the ministry is increasingly reluctant to issue guarantees is its refusal to grant these guarantees to Volkswagen. It was due to the fact that the company runs a manufacturing plant in Xinjiang, where the rights of Uyghurs[13] and Kazakhs are violated on a massive scale.

The government’s actions to date indicate that it is the Greens who are playing the main role in the process of modifying Germany’s policy towards China. Already during the election campaign they were most active in emphasising the need to alter Germany’s policy towards China and Russia and to become independent of them in the sphere of energy and economic affairs. The Green Party’s plans may be thwarted by the German Chancellery which is mainly responsible for shaping foreign policy and is still reluctant to see revolutions in Berlin’s relations with Beijing. In October 2022, Chancellor Scholz stressed the need to continue Germany’s economic cooperation with China and to concurrently diversify the investment and trade activity carried out by German companies. “Detaching oneself” from subsequent states would only lead to an end of globalisation which, according to the Chancellor, “has brought great prosperity to the world”.

Scholz’s intention to continue the activities launched by his predecessors may be corroborated by his imminent first visit to China where, according to media reports, he will be accompanied by the CEOs of Germany’s biggest companies. His attitude partly results from divergent views within the SPD regarding Germany’s cooperation with China. On the one hand, some prominent party members (e.g. the party’s co-leader Lars Klingbeil and foreign policy expert Nils Schmid) are calling for a revision of Germany’s stance on Beijing modelled on Ostpolitik. On the other hand, in August 2022 a group of SPD representatives signed a letter advocating a quick cease-fire between Ukraine and Russia,[14] in which China was listed among “neutral states” able to act as mediators in peace talks.

Efforts to convince business

Beijing’s restrictive policy in combatting COVID-19[15] and the barriers limiting the access which foreign businesses have to the local market have not weakened the interest of German companies in doing business in China – 52% of companies operating in the manufacturing sector and 49% of businesses dealing with wholesale trade do not intend to reduce their presence in China (45% and 44% of the surveyed companies, respectively stated they do intend to reduce their presence, and 4% and 7% of these companies wish to expand their activity in China).[16] German company executives openly admit that they are not going to withdraw from the Chinese market and argue that attempts to separate the Chinese economy from Western economies are an “illusion”.[17] They emphasise the need to maintain good relations with China in the context of the challenges facing the global financial and energy sector.[18] Small concessions made by Beijing encourage German companies to stay in the Chinese market and to expand their presence there. The granting of a Chinese business licence to BMW was an important event that enabled the company to increase its stake in the Chinese joint venture it co-forms from 50% to 75%.

Nevertheless, there are voices in German business communities suggesting that the atmosphere surrounding Berlin’s economic cooperation with Beijing is slowly changing. In 2019, the Federation of German Industries (BDI) published a report which it discussed cooperation with China in the context of the combination of partnership, systemic rivalry and economic competition discussed earlier in this text. In addition, the BDI presented its 54 recommendations for the federal government and the EU, which included a proposal to adjust the tools used to support exports in order to increase the competitiveness of companies from the EU and Germany in their rivalry with China, and to create an EU alternative to the Chinese Belt and Road Initiative.[19]

The increasingly unfavourable conditions for doing business in China have posed a problem in particular to German small and medium-sized companies. In 2020, the German Mechanical Engineering Industry Association (VDMA) that comprises 3,500 companies criticised the lack of equal opportunities for German companies doing business in China when compared to Chinese businesses operating in Europe.[20] The head of VDMA’s foreign trade department Ulrich Ackerman warned against the end of Chinese market prosperity and suggested that it would be necessary to “prepare for the opening of alternative growth markets in Asia sufficiently early”.[21] Regulations enabling the government in Beijing to acquire technical expertise from foreign companies operating in China are a further problem.[22]

From the government’s point of view, its most difficult task will be to convince German companies – in particular the largest ones – to gradually reduce their presence in China. Berlin’s stance on this issue may be influenced by public opinion–due to concerns about the energy crisis and price increases, any decision that could jeopardise the state’s economic stability may have a negative impact on the approval rating of the coalition made up of the SPD, the Greens and the FDP. This could in turn be reflected in these parties’ results in regional elections.

An opportunity for friend-shoring

Due to the ongoing energy crisis, the economic slowdown, reluctance on the part of Germany’s biggest companies and the absence of a clear vision of Germany’s relations with China, it is unlikely there will be a rapid shift in Germany’s China policy. Germany could be forced to make such a move if there is escalating tension between China and the US, e.g. caused by China launching an attack against Taiwan. However, this does not mean that the ongoing evolution of Germany’s approach to China will stop. Its pace will mainly depend on four factors: US pressure on Germany, China’s activity in the Indo-Pacific region, China’s decreased investment activity, and competition from the Chinese economy and the threat that poses to Germany.

It cannot be ruled out that the currently devised government strategies will focus on the protection of economic interests and on attempts to avoid antagonising Beijing as much as possible. At the same time, the mechanisms contained in these strategies will encourage German companies to relocate their operations from China and – in an attempt to diversify supply chains – to reroute their investments to other states in the region, and to reduce their dependence on the import of raw materials from China. Over the last several months, the economic affairs ministry (and other authorities), announced their plans to strengthen economic and trade partnership with those states that share democratic values (so-called friend-shoring). These intentions are reflected in the government’s decisions.

As part of its G7 presidency, Germany is continuing the “G7 Trade Track” initiative launched by the United Kingdom. It has listed the following issues as its priorities: the intention to boost multilateralism; to ensure free trade based on agreements and fair social standards being taken into account; environmental concerns and human rights; and building open, fair, stable and sustainable supply chains. Alongside this, Germany is seeking alternative sources of raw materials to replace those from China, and is creating conditions for doing business in which German companies could operate in countries that subscribe to liberal values (see the economic and energy agreement signed with Canada in August 2022).[23]

The initiatives carried out by the German government to date indicate that it is able to become more involved in the creation of the “democracy platform” – an economic and political model that envisages the need to reduce Germany’s relations with authoritarian regimes to a necessary minimum while integrating political and economic activities carried out by democratic states.[24] If Germany decides to embark on this, it would have a certain impact on Central Europe which would then become a potential destination for the relocation of German investments from China.

APPENDIX

Chart 1. China’s share in Germany’s exports and imports

Source: German Federal Statistical Office, German Economic Institute.

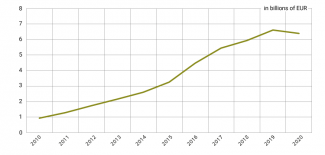

Chart 2. The value of German investment in China

Source: author’s own calculations based on data compiled by the Bundesbank.

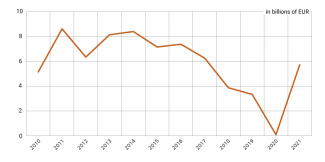

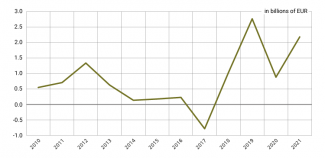

Chart 3. Germany’s net capital investment in China

Source: author’s own calculations based on data compiled by the Bundesbank.

Chart 4. The value of Chinese direct investment in Germany

Source: author’s own calculations based on data compiled by the Bundesbank.

Chart 5. Chinese net capital investment in Germany

Source: author’s own calculations based on data compiled by the Bundesbank.

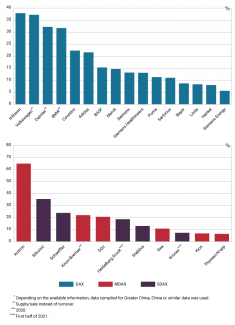

Charts 6 and 7. China’s share* in the turnover of companies included in the DAX, MDAX and SDAX stock market indexes in 2021.

Source: U. Sommer, ‘Das große China-Risiko – Einige Dax-Konzerne könnten Konflikte wie mit Russland kaum verkraften’, Handelsblatt, 21 March 2022, handelsblatt.com.

[1] To avoid the impression that Germany is bypassing other states of the region, in May 2011 intergovernmental consultations were launched with India. As a consequence, India became the second non-European state – after Israel – to be included in this mechanism.

[2] L. Flach, F. Teti, I. Gourevich, L. Scheckenhofer, L. Grandum, Wie abhängig ist Deutschland vom Reich der Mittevon Rohstoffimporten? Eine Analyse für die Produktion von Schlüsseltechnologien, ifo Institut, June 2022, ifo.de.

[3] See S. Płóciennik, ‘Germany and the crisis of globalisation: adjustment strategies’, OSW Commentary, no. 446, 17 May 2022, osw.waw.pl.

[4] A. Baur, L. Flach, Deutsch-chinesische Handelsbeziehungen: Wie abhängig ist Deutschland vom Reich der Mitte?, ifo Institut, 13 April 2022, ifo.de.

[5] A. Kratz, N. Barkin, L. Dudley, ‘The Chosen Few: A Fresh Look at European FDI in China’, Rhodium Group, 14 September 2022, rhg.com.

[6] J. Matthes, Unternehmensübernahmen und Technologietransfer durch China, Institut der deutschen Wirtschaft, 14 July 2020, iwkoeln.de.

[7] The United Kingdom was ranked first – 79.6 billion euros. See A. Kratz, M.J. Zenglein, G. Sebastian, M. Witzke, Chinese FDI in Europe: 2021 Update, Mercator Institute for China Studies, Rhodium Group, 27 April 2022, rhg.com.

[8] Chinesische Unternehmenskäufe in Europa, EY, March 2022, ey.com/de_de.

[9] Verfassungsschutzbericht 2021, Bundesministerium des Innern und für Heimat, 7 June 2022, bmi.bund.de.

[10] Western Balkans: The burden of China’s lending to governments, UniCredit, 27 April 2021, research.unicredit.eu.

[11] See K. Popławski, ‘Germany is open to Huawei’s participation in 5G’, OSW, 23 October 2019, osw.waw.pl.

[12] See S. Płóciennik, ‘Germany and the trade conflict between Lithuania and China’, OSW Commentary, no. 424, 4 February 2022, osw.waw.pl.

[13] M. Greive, D. Heide, J. Olk, ‘Bundesregierung stößt Kurswechsel in der China-Politik an’, Handelsblatt, 26 August 2022, handelsblatt.com.

[14] J. Gotkowska, ‘Niemieckie dylematy dotyczące dostaw broni dla Ukrainy’, OSW, 7 September 2022, osw.waw.pl.

[15] M. Bogusz, ‘China: the consequences of the ‘zero COVID’ strategy’, OSW Commentary, no. 463, 27 July 2022, osw.waw.pl.

[16] In the retail sector alone most companies (55%) intend to reduce their activity in China, 1% intend to increase, and 44% are not planning any change. See A. Baur, L. Flach, Deutsch-chinesische Handelsbeziehungen…, op. cit.

[17] In an interview for the Die Welt daily, the CEO of Mercedes-Benz Ola Källenius said: “If someone thinks that the Chinese economy can be separated from the European or American economy, it’s a complete illusion. This would have catastrophic consequences for the global economy that would be incomparable with the war in Ukraine. As an export-oriented company, we always try to remind people of the huge benefits offered by an open, global economy”. See U. Poschardt, D. Zwick, ‘Unsere Wirtschaft ohne China? „Das ist eine völlige Illusion”’, Die Welt, 7 September 2022, welt.de.

[18] S. Hage, S. Klusmann, ‘»Ohne die Geschäfte mit China würde die Inflation noch weiter explodieren«’, Der Spiegel, 30 June 2022, spiegel.de.

[19] ‘Partner and Systemic Competitor – How Do We Deal with China’s State-Controlled Economy?’, BDI, January 2019, english.bdi.eu.

[20] H. Dieter, Die ungewisse Zukunft der deutsch-chinesischen Beziehungen, Stiftung Wissenschaft und Politik, 9 December 2021, swp-berlin.org.

[21] ‘China als Handelspartner und Konkurrent: Abkehr von der „Win-Win-Situation”’, marketing-BÖRSE, 17 December 2020, marketing-boerse.de.

[22] P. Kulitz, ‘Deutsch-Chinesisches Dialogforum. Publikation 2022’, deutsch-chinesisches-dialogforum.de.

[23] See M. Kędzierski, L. Gibadło, ‘Scholz i Habeck w Kanadzie – wizyta z energetyką w tle’, OSW, 27 August 2022, osw.waw.pl.

[24] See S. Płóciennik, ‘Germany and the crisis of globalisation: adjustment strategies’, op. cit.