A struggle to survive. Ukraine’s economy in wartime

The ongoing war in Ukraine has had a disastrous impact on the country’s economy. Its GDP has fallen by approximately a third, and material losses due to the destruction of infrastructure have exceeded US$100 billion and are rising every day. The high inflation rate, the weakened currency and the very high unemployment rate are taking an increasing toll on Ukrainian society. The functioning of the country, including the disbursement of social benefits, salaries and pensions, depends almost entirely on foreign financial assistance. Even though international support for Ukraine has been growing, it remains insufficient, which has forced the government to radically increase public debt. Despite the observed positive trends, such as increased exports (in particular agricultural goods) and the stabilised fuels market, no substantial improvement in the economic situation should be expected before the end of the war. In fact, it seems more likely that it will deteriorate further, given that Russia will most likely continue its attacks on Ukrainian infrastructure, and the future of maritime food exports is open to question.

The macroeconomic situation

The war has led to the largest economic slump in the history of independent Ukraine. Compared to the same time periods in 2021, Ukraine’s GDP dropped by 19.1% in the first quarter of 2022 and by 37.2% in the second quarter. From January to September 2022 it fell by 30%. The National Bank of Ukraine (NBU) has forecast that Ukraine’s GDP will decline by 37.5% in the fourth quarter of the year, and by 33.4% for the whole year. Even though this forecast is slightly better than that assumed in the most pessimistic scenarios from the first months of the war (in June the World Bank predicted that Ukraine’s GDP would fall by 45%), the economic situation in the country remains extremely complicated. Although GDP is expected to rise in 2023, it is hard to say there will be a genuinely dynamic rebound: according to the Ukrainian government the economy will grow by 4.6%, whereas the World Bank forecasts growth of 3.3% and the European Bank for Reconstruction & Development predicts a growth in GDP of 8% in the most optimistic scenario.

The rising inflation rate is an increasing problem for Ukraine: in January 2022 it stood at 10%, by September it had already reached 24.6%, and it will reach 30% by the end of the year, according to the NBU’s forecast. The increased prices of food staples affect Ukrainians the most: prices of bread and baked goods rose by 36.6%, fish by 40.7% and vegetables by as much as 84.8%, due to the occupation of the Kherson oblast, which is the main producer of vegetables in Ukraine. Furthermore, fuel prices have also risen (by 66.2%), which has driven up transportation costs (by 41.1%). At the same time the minimum wage increased slightly at the beginning of October, from 6500 hryvnia (approximately US$178) to 6700 (approximately US$183); the budget for 2023 does not allow for their further revision. Average salaries and wages, which in January stood at 14,600 hryvnia (approximately US$435), are set to rise to 18,500 (approximately US$550) in 2023, according to the government’s forecast; however, even that will not solve the problem.

Another thorny issue is the very high unemployment rate. According to a survey conducted by “Rating” Group, up to 39% of Ukrainians who had jobs before the war have lost them. The NBU reports the unemployment rate at 35%, although industry experts cite estimates of 40%. A further challenge is the fact that a large section of the employed are receiving lower salaries and wages than they did before the Russian invasion of Ukraine, due to the worsening financial situation of individual companies. The Ukrainian currency is also being gradually weakened. After the war started the NBU froze the hryvnia exchange rate, which at that time was 29.25 hryvnia to the US dollar. Nevertheless, in July the exchange rate was corrected to 36.6 hryvnia to the dollar, and the real rate in exchange offices remains at around 41 to the dollar. The government predicts that towards the end of 2023 the exchange rate will rise to 50 hryvnia to the dollar.

Boosting the business sector is one of the priorities of Ukraine’s economic policy. Despite limited resources the Ukrainian government is continuing the programme of granting low-interest rate loans (between 5 and 9%). Since the beginning of the war, 13,500 loan agreements worth a total of 54 billion hryvnia (around US$1.5 billion) had been signed as of 10 October. Furthermore, the government is maintaining support for employers who would like to move their business activity from war-torn areas to safer regions of the country. According to data from 26 September, 1846 companies declared they wished to relocate and 558 companies resumed their activity in a new area. It is difficult to clearly assess the effects of these measures to date, although it seems that their impact has not been very significant: before the war there were over 370,000 registered companies, including 18,000 large and medium-sized ones.

Problems with the budget

After the war began the Ukrainian parliament adopted a host of amendments to tax law which made conducting business substantially easier. These amendments were intended to prevent a further dramatic rise in unemployment and constraints on business activity, and included such measures as the lifting of customs and VAT on imports and excise on fuels. This has brought about a negative effect in terms of a fall in budget revenues: the Ministry of Finance estimated in June that it had received only 30% of the customs revenues and 70% of the tax revenues it got before the war. From the very beginning, a number of experts criticised the tax reductions as a populist move, and for this reason customs and VAT were reinstated as of 1 July (thanks to this the budget gained over 10 billion hryvnia in July alone), and the excise on fuels was restored as of 30 September.

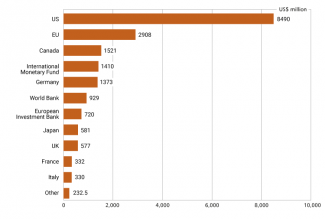

The economic crisis has caused huge budgetary problems. Government representatives have regularly stated that the estimated budget deficit is US$5 billion a month, although official data indicates that the deficit is lower in some months (for example it reached US$2 billion in September). The main financing for the deficit comes from assistance from Western countries and international financial institutions. According to the Ukrainian Ministry of Finance, since the beginning of the war Ukraine had received US$19.4 billion as of 4 October, most of which had been provided by the US (US$8.5 billion) and the EU (US$2.9 billion).

Chart 1. The largest foreign contributors to Ukraine’s budget (as of 4 October 2022)

Source: Ministry of Finance of Ukraine.

Initially, the support from Western countries was provided in the form of low-interest loans, and subsequently (to an increasing extent) in non-repayable grants. In total, the Ukrainian budget has received US$10.1 billion in subsidies (mainly from the US) and US$9.3 billion in loans. The major issue with foreign assistance is its irregularity, which makes it more difficult for the Ukrainian government to plan the country’s spending. Delays in disbursing the assistance present another challenge; for example in May the European Commission announced a micro-financial assistance package support worth €9 billion, but at the time of writing it has only transferred €1 billion (another instalment of €5 billion is scheduled to be transferred to the Ukrainian budget in the coming days).

Nevertheless, the scale of foreign assistance is not sufficient compared to the country’s needs. Ukraine has been forced to issue internal bonds, which are mainly being bought by the NBU. In effect this means ‘printing’ hryvnias: since the beginning of the war nearly US$15 billion have gone into Ukraine’s budget by this method. As a result, public debt reached 3.6 trillion hryvnia (approximately US$98.3 billion, i.e. 65% of the pre-war GDP) at the end of August. Since the end of January public debt has risen by 839 billion hryvnia (c. US$22.9 billion at the NBU’s current exchange rate), of which 638 billion hryvnia (c. US$17.4 billion) accounted for external debt and 201 billion hryvnia (c. US$5.5 billion) went on internal debt. Ukraine has been working to halt the repayment of the debt, and some of its actions have been partially effective. On 14 September the Ministry of Finance signed a memorandum with G7 creditors which stipulated that Ukraine would suspend the repayment of its debt until the end of 2023, as this will enable the country to save US$3.1 billion.

Foreign assistance will continue to be indispensable next year as well. The draft budget, which was adopted at first reading, allows for expenditure of 2.5 trillion hryvnia, of which only 1.3 trillion is planned to come from budget revenues. A third of the planned expenditure will be spent on military purposes (salaries and purchases of equipment for the army). Ukraine estimates that foreign assistance in 2023 will reach US$38–43 billion (depending on the adopted exchange rate), i.e. over US$3 billion a month; this will make it possible to cover almost half of the budget expenditure.

Positive trends in external trade

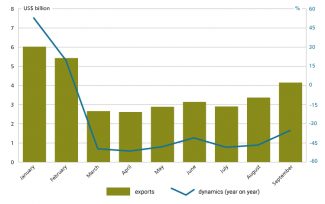

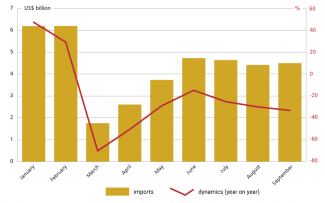

Russia’s invasion of Ukraine has led to a collapse in Ukraine’s foreign trade. This crisis has been caused above all by the blockade of Ukraine’s ports on the Black and Azov Seas, which accounted for approximately 70% of external trade before the war. Consequently, in March exports fell by 50% and imports by up to 71% compared to the same month in the previous year.

Chart 2. Exports of goods from Ukraine, and their dynamics in 2022

Source: State Statistics Service of Ukraine, Ministry of Economy of Ukraine.

Chart 3. Imports of goods into Ukraine, and their dynamics in 2022

Source: State Statistics Service of Ukraine, Ministry of Economy of Ukraine.

In order to become self-reliant, Ukraine was forced to quickly set up alternative routes for transporting goods and to find other sources of products which it used to import from Russia and Belarus before the war, in particular fuels. Up to now Russia and Belarus accounted for 71% of the fuels Ukraine imported. In order to change this, Ukraine has started making more use of its Danube ports (above all those transporting food) and border crossings with EU countries (mainly Poland and Romania). Thanks to this measure, exports via road transport have risen from 444,000 tonnes in March to 1.4 million tonnes in September, and exports of goods transported by rail rose from 2.4 million tonnes to 2.8 million tonnes. However, these changes are linked to many logistical challenges (different rail gauges, low capacity of Ukrainian roads) which have not yet been fully addressed.

The key to boosting external trade has been the partial unblocking of three Black Sea ports (exclusively for agricultural goods) as part of the ‘grains corridor’. This was made possible thanks to the agreement signed on 22 July in Istanbul by Ukraine, Turkey and the UN. As a result, external trade in goods rose from US$2.9 billion in July to US$3.4 billion in August and US$4.1 billion in September. Even though this is an undoubted success, it should be borne in mind that compared to the same month in 2021, exports in September were still 35% lower and imports 33% lower.

The destruction of infrastructure

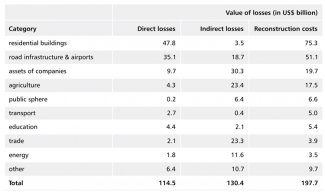

The war has led to enormous losses in infrastructure. Since the beginning of Russia’s invasion of Ukraine, as part of the ‘Russia will pay’ project, the KSE Institute (an analytical centre at the Kyiv School of Economics), with the support of the Office of the President of Ukraine and the ministries of economy and infrastructure, has been involved in monitoring and documenting the damage. Publicly available information is being used to assess the destruction, among other tools, including a special internet site where everybody can report the damage or destruction of buildings.

As of 5 September, the KSE estimates direct losses at US$114.5 billion – US$4.1 billion more than the worth indicated in the KSE report from 8 August. The bulk of this amount (over 72%) consists of residential buildings (US$47.8 billion) and transport infrastructure (US$35.1 billion: see Appendix). Due to the war the following buildings have been damaged: 131,000 residential buildings, 422 industrial facilities, nearly 2500 schools and universities, 188,000 cars, 9500 buses, almost 500 trams and trolley buses, over 500 public administration buildings, and nearly 1000 medical buildings.

It is worth noticing that the direct losses have not risen significantly over the last four months: at the end of May the KSE estimated them at US$105.5 billion. This situation may stem from a certain stabilisation on the majority of the war fronts, and the limited number of air raids and missile attacks in the interior of Ukraine. An important problem is posed by difficulties in assessing damages in areas controlled by Russia, mainly in the Luhansk and Donetsk oblasts. At the same time, losses and related estimates of reconstruction costs can be expected to rise in the near future, since the report was prepared before the liberation of a major part of the Kharkiv oblast including the towns of Kupiansk and Izyum by the Ukrainian army (a total of around 8000 km²). The assessment does not cover the effects of the missile strikes on 10 and 11 October, in the aftermath of which energy facilities were destroyed or damaged in 11 oblasts in Ukraine, including Kyiv.

The outlook

As long as intensive military operations are underway, the economic situation in Ukraine should not be expected to improve. In the forecasts for 2023 a slight growth of GDP is predicted, even though Ukrainian government representatives admit they cannot rule out a recession (depending on how the military situation develops). There is still a risk that the country will be paralysed due to the destruction of its critical infrastructure, as exemplified by the mass-scale missile attacks on 10 and 11 October. These led to what was only a temporary destabilisation of the electricity grid, but emergency power cuts will have a negative impact on the production of those companies still in operation in the industry sector. It is difficult to gauge whether the increase in exports that has been observed over the last two months can be sustained in the longer term: this will depend above all on the maintenance of the grains corridor (the agreement establishing it expires in November) which Russia may block.

The functioning of the country will entirely depend on financial assistance from Western countries and international institutions, both during wartime and for many months following the end of the war. The EU is taking action in order to establish a mechanism that will make it possible to transfer €1.5 billion to Ukraine’s budget each month. Furthermore, according to media reports, the US intends to provide support worth US$1.5 billion monthly to Ukraine as long as the war continues. It remains unclear what impact the elections to the US Congress in November will have, as the Democrats may lose the majority in Congress. The assistance to Ukraine enjoys bipartisan support; however, there are circles in the Republican party which have been reluctant to commit further funds to the country.

APPENDIX

Table. The KSE’s estimates regarding the destruction of Ukraine’s infrastructure (as of 5 September)

Source: KSE Institute.