Israel’s Mediterranean gas: the potential for gas export to Europe and the dynamic of regional cooperation

Once gas extraction from the Karish gas field starts, which is scheduled for September 2022, Israel will have a gas surplus enabling it to export around 10 bcm of this fuel to the European Union states every year. To this end, it intends to use the infrastructure connecting its gas fields with LNG terminals in Egypt, in line with the provisions of a Memorandum of Understanding which Egypt, Israel and the EU signed in June 2022. For the time being, no contracts with gas recipients in Europe have been signed, and no details regarding the price of gas sold to the EU have been provided. The continued development of Israel’s gas fields and the expansion of its infrastructure (pipelines and floating LNG platforms) will further increase the country’s export potential. The Israeli government intends to keep prioritising the country’s domestic demand. Despite its increasing commercial significance, the importance of the sale of gas to foreign partners is mainly of a political nature, as it helps to foster the development of relations in the region. Aside from Egypt, Israel’s major partners in the energy sphere include Cyprus, Greece and Jordan. The role of the United Arab Emirates in this context is also increasing. Hezbollah may pose a threat to gas export plans, as it has been pursuing Iran’s interests, which in the context of gas issues are convergent with those of Russia, and ties between these two countries are growing ever closer.

Israeli gas for Europe

The EU’s interest in Israeli gas results from the need to quickly diversify its sources of gas in connection with Russia’s aggression against Ukraine and with the reduced volume of hydrocarbon imports from Russia (in 2021, aside from other hydrocarbons, the EU purchased 155 bcm of gas from Russia, which accounts for 40% of its annual consumption).[1] At the same time, the profitability of gas imports from Israel has increased due to the very high prices of gas recorded on European gas hubs since autumn 2021.

The export of Israeli gas to Europe will be possible once gas extraction from the Karish gas field is launched, which is scheduled for September 2022. As a consequence, Israel will have a gas surplus of up to 10 bcm/year in excess of its present domestic consumption and export obligations. Additional surplus may emerge once gas extraction from the Leviathan gas field increases from the present 12 bcm to 21 bcm annually. This depends on whether new infrastructure for transporting gas is built; this in turn may be facilitated by the construction of a floating LNG installation and/or new pipelines in the vicinity of this gas field. Furthermore, work is ongoing on the launch of gas extraction from the Olympus and Ishai fields. The latter field is adjacent to Cyprus’s Aphrodite field: negotiations regarding the parameters of its joint exploitation are under way (see Appendix). Moreover, in May 2022 (contrary to previous declarations) preparations were launched for the fourth round of tenders to prospect for new gas reserves. This decision was motivated by the need to support Europe in its efforts to diversify its sources of gas.[2]

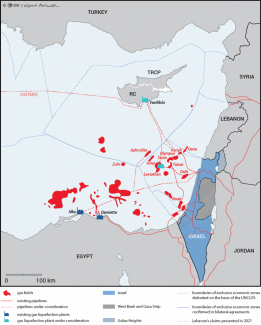

Efforts to procure Israeli gas were made by the European Commissioner for Energy Kadri Simson when she held talks with the Israeli minister Karine Elharrar (in an online conversation on 3 March, and in person during a meeting of the International Energy Agency on 23 March in Paris). As no other options are available at present, the gas intended for export to Europe would be liquefied in the Egyptian LNG terminals at Damietta[3] and Idku;[4] however, their combined capacity does not exceed 17 bmc. Gas is transmitted from Israel to the Egyptian system via the Ashkelon–El Arish pipeline, and also (since March 2022) via the Arab Gas Pipeline running through Jordan. Their combined capacity is a mere 7–10 bcm. In connection with the intention to raise gas exports to Europe via Egypt to a volume higher than what the present gas network permits, plans have been made to build new pipelines connecting the two states. This is envisaged in the Memorandum of Understanding signed by Israel and Egypt in November 2021 on examining the potential for exporting additional amounts of Israeli gas to Egypt.[5] Work has already commenced on a new onshore pipeline via North Sinai, and the construction of an offshore route between Israeli gas fields and the Egyptian LNG terminals is being considered (see map in the Appendix). Talks are ongoing at the level of a tri-partite EU-Egypt-Israel working group, and between ministries and companies, with the participation of representatives of potential recipient states, the list of which has not yet been revealed.[6]

On 15 June 2022 in Cairo, representatives of the European Commission (Commissioner Simson, in the presence of President Ursula von der Leyen), Egypt (Minister Mohamed Shaker el-Markabi) and Israel (Minister Elharrar) signed a MoU on trade in natural gas, its transport and export to the EU. The parties pledged to work to ensure stable gas supplies. As a result of the implementation of the MoU, a plan will be devised for the effective utilisation of infrastructure enabling gas transmission to the EU, alongside a so-called road map guiding the formalisation processes necessary to realise the assumptions contained in the MoU (e.g. contracts detailing specific terms of supply). The document envisages that the EU will encourage European companies to invest in gas prospecting & extraction in Israel and Egypt. It also mentions research into the possible use of carbon capture & sequestration technology, as well as prospective funding of research activities focused on emissions reduction and decarbonisation. The parties acknowledged the need to encourage their public and private entities to cooperate in the field of hydrogen technology, green energy and energy efficiency. The memorandum can automatically be prolonged twice, each time for another three years, and does not affect the other export commitments of specific states.[7]

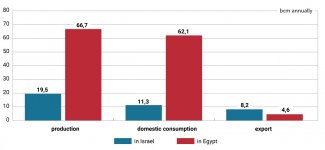

The EU views the planned launch of the import of Israeli gas in autumn 2022 as the first concrete result of the MoU’s signing. However, specific arrangements will need to be made beforehand, as the document does not put any binding legal and financial obligations on the parties, and does not specify any timeframe, volume, recipients or prices of the gas supplies. The fact that the agreement was signed during the seventh ministerial meeting of the East Mediterranean Gas Forum (EMGF, see below) increases its political significance, and confirms that the EU sees this format as an element of the process of development of cooperation between the region’s states. Likewise, the EC supports Egypt’s attempts to play the role of a regional gas hub, in particular when it comes to the use of LNG technology. Although so far Egypt has used its own gas (including from the Zohr gas field, estimated at 850 bcm) to cover its domestic needs, its potential for export is also rapidly increasing.[8] In addition, the MoU is expected to bring benefits to those EU member states that are EMGF participants: the signatories will facilitate the sale of gas produced by other Eastern Mediterranean states to Europe. In particular this might concern Cyprus, which plans to transport gas from its Aphrodite gas field[9] to liquefaction terminals in Egypt (the route should be ready in 2025). Construction of an export pipeline from Egypt to the Greek island of Crete is also being considered.[10]

Israel’s gas will be sold to the EU in line with the latter’s energy transformation goals that view gas as a transition fuel. During her visit to Israel and Egypt (13–15 June), von der Leyen stressed that the newly-built infrastructure should be adapted for the prospective transport of hydrogen in the future. The EU–Egypt Mediterranean Hydrogen Partnership, which covers a wide array of energy issues, is to be finalised during the COP 27 climate conference in Sharm el-Sheikh.[11] Egypt’s important role in the EU’s energy policy[12] has resulted from its rapid development in spheres such as gas extraction and liquefaction, renewable energy, inter-continental infrastructure and hydrogen technologies developed in collaboration with European partners.[13] Ultimately, the Middle East could become an important source of solar and wind energy (Egypt, Jordan and Saudi Arabia have the biggest potential in this respect), and potentially also of hydrogen for Europe, depending on technological advancement. In this context, Israel could contribute with technologies and serve as a land bridge.

Gas as a catalyst for Israel’s regional integration

For more than a decade, Israel has viewed regional energy cooperation as an issue of fundamental importance. The size of the gas fields and the challenges connected with their commercialisation have triggered an unprecedented development of grassroots cooperation initiatives between the coastal states, covering economic and security issues (such as collaboration during natural disasters and regular joint military exercises). Initially, two trilateral formats prevailed: Cyprus–Greece–Egypt and Cyprus–Greece–Israel. At the seventh meeting of the latter format, held on 2 January 2020 in Athens, an agreement was signed to construct the EastMed gas pipeline, with a length of around 2000 km and a capacity of 20 bcm annually. It is projected to run from the Leviathan gas field via the Aphrodite gas field to Greece, and onward (via the Poseidon pipeline) to Italy and Europe. Thus far, the project’s role has mainly been political, as it has consolidated cooperation between the countries involved. The prospects for the investment’s implementation have been undermined by its high cost (€7 billion) and certain infrastructure-related challenges (in particular on the section from Cyprus to Greece), combined with low crude oil prices recorded at that time and increasing consumer preference for LNG & sustainable energy sources. However, the European Commission has included EastMed in its list of projects of common interest and continues to support its construction, because it could also be used to transport hydrogen in the future, among other reasons. The Edison and DEPA companies plan to complete the project in 2027. The EuroAsia Interconnector between the power grids of Greece, Cyprus and Israel is intended to be another important element of energy infrastructure (although Israel has not yet managed to complete the necessary formalities[14]).

Efforts to reduce the potential competition between these formats and to streamline the projects under development are being facilitated by the EMGF, which was established in January 2019 and soon afterwards transformed into an international organisation based in Cairo. It aims to build a regional gas market (which involves efforts to regulate supply, demand, infrastructure, pricing, etc.) while at the same time dealing with other energy issues, including renewable energy. Its members are Cyprus, Egypt, France, Greece, Israel, Italy, Jordan and Palestine, while the EU and the US have permanent observer status. The World Bank is providing the EMGF with substantive support, and a committee of representatives of private business has been formed.[15]

Gas extraction has consolidated Israel’s relations with the two neighbouring Arab states with which it had signed peace treaties. Israeli gas has been exported to the Jordanian market since March 2017, and to Egypt since January 2020. The process of consolidating regional energy cooperation is being facilitated by the dynamic resulting from the normalisation of relations between Israel and the United Arab Emirates. The UAE has actively invested in the Eastern Mediterranean states, including in the energy sector (for example, it has purchased a stake in Israel’s Tamar gas field; it is expected to provide funding for an Israeli-Jordanian ‘water for electricity’ project, and has launched investment partnerships with Cyprus, Greece, Egypt and Jordan).

Turkey remains on the margins of cooperation in the region. The new cooperation formats have taken on an anti-Turkish tone in response to Ankara’s confrontational stance (regarding the conflict over Cyprus[16] and the agreement Turkey signed with Libya in 2019 regulating their maritime border, which infringed upon other states’ interests). Due to Turkey’s difficult economic situation, President Recep Tayyip Erdoğan has adjusted his policy since 2021 in order to improve his country’s relations with Egypt, Israel and others. However, the Cyprus conflict and tensions with Greece prevent Turkey from joining the EMGF and expanding the infrastructure it would need to receive Israeli gas. Although Ankara does import small amounts of it in liquefied form via Egypt,[17] in the foreseeable future the EU will be Israel’s priority client for its gas surplus. At the same time, Turkey may join regional cooperation initiatives in the field of renewable energy sources.[18]

Lebanon is playing an important part in the context of Israel’s gas exports to the EU. Its permanent domestic crisis has so far prevented it from exploiting its own gas fields. Israel is willing to make concessions to improve the investment climate, to stabilise Lebanon and ultimately to establish peaceful relations with Beirut. Despite all this, talks on the delimitation of a maritime boundary between the two states, which have been ongoing since 2010, have failed to bring any results so far. In response to the plans to extract gas from the Karish field, Beirut increased its claims by another 1400 km2 in addition to the initially declared 860 km2. The connection of an FSPO platform to this gas field in June 2022 provoked a reaction from Hezbollah, which threatened to shell this infrastructure with missiles and sent UAVs in its direction. The proposal currently being considered involves allocating the Qana gas field to Lebanon and the Karish gas field to Israel.[19] The parties intend to reach an agreement as early as September 2022. The government in Beirut seems to have adopted a more pragmatic stance on the issue than previously, and public opinion increasingly views Hezbollah’s actions as unfavourable to Lebanon’s national interest. However, this organisation, which to a large degree acts as an executor of Iran’s will and tightens ties with Russia, is continuing to step up its rhetoric and actions. As a consequence, it is becoming the biggest threat to the implementation of the plan to export Israeli gas to Europe.[20]

Gas for Europe and Israel’s energy policy

Israel’s energy policy should be viewed as another important context for the issue under discussion. If it sells around 10 bcm of gas to the EU annually, that would equate to doubling its gas export volume. In the media debate, proponents of the plan to increase the gas exports emphasise the economic and political opportunities this would offer, and stress the need to sell gas as long as there are clients interested in purchasing it in an era marked by a gradual move away from conventional energy sources. Sceptics, however, doubt whether interest in Israeli gas will be sufficiently long-lasting. Others argue that the most important goal is to maintain gas reserves so that rising domestic demand can be met in the next few decades.[21] According to the rules in place in Israel, 540 bcm of gas (around 60% of proven reserves) is intended for the domestic market, and thus cannot be included in its export plans. In addition, certain individual limitations have been introduced depending on the size of specific gas fields. A debate is ongoing on increasing the allowed export volume, at least in the case of gas obtained from new reserves.[22] However, it seems that the political elites have reached a consensus regarding the decision to launch gas export to Europe, and Israel’s ongoing political crisis should not jeopardise its implementation.

In these debates, important contributors include not only politicians, but also officials (including committees appointed by the energy ministry’s director general, the state comptroller’s office, the anti-trust office), local authorities, civil society, academics and experts, industry representatives and the courts.[23] Issues of particular controversy have included the following: the introduction of a corporate tax, a plan to break up monopolies that inflated gas prices, environmental issues, and securing resources for domestic consumption by introducing export restrictions. These have provoked debates in the media and among experts, as well as street protests. At present – although work on the basic legal framework for the operation of the gas production sector has been completed – discussions about the need to increase competition and to reduce prices on the domestic market are ongoing.[24] In addition, new infrastructure investments may provoke opposition from local communities and environmental organisations.[25]

It should be noted that gas export in Israel has thus far mainly been viewed as a tool for consolidating the country’s relations with its foreign partners. It was only recently that gas extraction began to be perceived in the context of the size of deposits in the sovereign wealth fund: of the 1.25 billion shekels (around €380m) paid into this fund in 2021, 700 million shekels (c. €212m) was contributed by the gas sector.[26] Meanwhile, Mediterranean gas has already enabled Israel to become self-sufficient in terms of energy, at least with regard to electricity generation: plans have been made to phase out the coal used for this purpose by 2025.[27] However, Israeli experts argue that in the context of the threats posed by potential missile and cyber attacks, genuine energy security can only be achieved on the basis of scattered renewable energy sources.[28] Although this sector’s development is being delayed by infrastructural, legal and bureaucratic barriers, efforts have recently been made to overcome them, and the state has huge potential in technology and research, including in the field of energy storage.[29]

Summary

The launch of gas extraction from the Karish gas field and the signing of the trilateral agreement between Israel, Egypt and the EU have made it significantly more likely that Israel will commence the export of up to 10 bcm of gas to Europe annually in 2022. In the context of both the present crisis on the EU gas market and the energy transition process, the EU strives to encourage various states & companies to expand energy infrastructure in the region. At the same time, the plan to increase the volume of gas transmission to 20 bcm and more over the next few years (taking the combined potential of Cyprus, Egypt and Israel into account) would require investments (for example, an LNG platform in the vicinity of the Leviathan gas field, and also new pipelines: an onshore pipeline connecting Israel with Egypt, an offshore pipeline running from the Aphrodite gas field to Egypt, and EastMed). If Israel can act as a gas supplier and participant in EU-Middle East energy projects, this will be conducive to improving its relations with the EU. Moreover, this cooperation enjoys the support of the United States.[30] However, it does collide with the interests of Russia and Iran.[31] The export of gas to the EU could be another factor worsening Israel’s relations with Russia in the context of the latter’s aggression against Ukraine.[32] One factor that could jeopardise the implementation of these plans could involve an escalation of Israel’s confrontation with Iran, while Moscow is strengthening its relations with Tehran. Actions by Hezbollah represent a possible manifestation of this Iranian-Russian threat. The risk of attacks by it will likely decrease if negotiations on delimitation of the Israeli-Lebanese border are successful. A further potential threat may arise from possible protests by Israeli citizens against the construction of new gas extraction and transmission infrastructure.

APPENDIX

- Israel and gas[33]

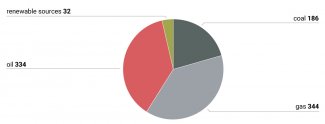

Chart 1. Israel: sources of energy in 2020 (in TJ)

Table. Proven Mediterranean gas fields

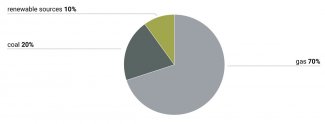

Chart 2. The share of gas in electricity generation

- Israel and Egypt as gas producers[34]

Chart 3. Gas production, domestic consumption and export

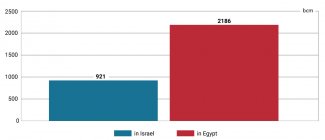

Chart 4. Proven gas reserves

- Map. Israeli gas in the Mediterranean Sea

Sources: Author’s analysis, on the basis of ‘Israel natural gas transmission system’, Israel Natural Gas Line, 2020, ingl.co.il; ‘Delek hopes to start gas exports to Egypt by the end of June’, TEKMOR Monitor, 3 June 2019, tekmormonitor.blogspot.com; ‘Export’, Israel’s Ministry of Energy, energy-sea.gov.il.

[1] I. van Halm, ‘How can the EU end its dependence on Russian gas?’, Energy Monitor, 11 May 2022, energymonitor.ai.

[2] Y. Katz, D. Brinn, ‘How Israel is using gas exports to boost its diplomatic standing’, The Jerusalem Post, 19 June 2022, jpost.com; ‘Launch of Fourth Offshore Bid Round for New Natural Gas Exploration Licenses in the EEZ of the State of Israel’, Israel’s Ministry of Energy, 30 May 2022, gov.il.

[3] Re-opened in 2021. The Spanish company SEGAS is its operator, and the stakeholders are the Italian company ENI (a 50% stake), the Egyptian Natural Gas Holding Company (EGAS, 40%) and the Egyptian General Petroleum Corporation (EGPC, 10%).

[4] Egyptian LNG is the operator, and the stakeholders are Shell (a 35.5% stake), Petronas (35.5%), EGPC (12%), EGAS (12%) and TotalEnergies (5%).

[5] G. Mitchell, ‘Exporting Israel’s gas to Europe: An initial but momentous step – opinion’, The Jerusalem Post, 21 June 2022, jpost.com; ‘A joint Memorandum of Understanding was signed, to promote a joint examination of exporting additional amounts of natural gas in light of the global efforts to reduce greenhouse gas emissions’, Israel’s Ministry of Energy, 25 November 2021, gov.il.

[6] Y. Katz, D. Brinn, ‘How Israel…’, op. cit.

[7] EU Egypt Israel Memorandum of Understanding, The European Commission, 15 June 2022, energy.ec.europa.eu.

[8] A. Fouad, ‘Egypt’s future in the LNG market’, Middle East Institute, 21 September 2021, mei.edu.

[9] This gas field contains around 120 bcm of gas, and is the most likely of Cyprus’s gas field to commence gas production. Its stakeholders include Delek, Chevron and Shell. See ‘Strategic Energy Hub’, Cyprus Profile, December 2021, cyprusprofile.com.

[10] J. Krasna, ‘Politics, War and Eastern Mediterranean Gas’, Moshe Dayan Center for Middle Eastern and African Studies, 24 March 2022, dayan.org.

[11] EU-Egypt Joint Statement on Climate, Energy and Green Transition, The European Commission, 15 June 2022, ec.europa.eu.

[12] See the 2018 MoU on strategic energy partnership between the EU and Egypt.

[13] M. Tanchum, ‘Egypt’s Synergy Between Natural Gas and Green Energy Transition: Cairo’s Advances in LNG and Green Hydrogen are Shaping the COP 27 Agenda’, Middle East Institute, 5 May 2022, mei.edu.

[14] G. Mitchell, ‘Exporting Israel’s gas to Europe…’, op. cit.

[15] ‘Eastern Mediterranean countries to form regional gas market’, Reuters, 14 January 2019, reuters.com.

[16] A. Michalski, ‘Cypr w polityce Turcji’, Komentarze OSW, no. 412, 20 October 2021, osw.waw.pl.

[17] Pipelines vs. Interconnectors: Israel and the EU energy relationship, BICOM, 16 June 2022, bicom.org.uk.

[18] ‘President Isaac Herzog delivers his ‘Renewable Middle East’ speech’, The President of Israel, 23 February 2022, gov.il; Regional Climate Change Initiative of the Republic of Cyprus, emme-cci.org.

[19] J. Krasna, ‘Politics, War and Eastern Mediterranean Gas’, op. cit.; D. Zaken, ‘Lebanon reportedly drops claims on Karish gas field’, Globes, 20 June 2022, en.globes.co.il.

[20] S. Nowacka, ‘Znaczenie udziału polskiego kontyngentu w misji UNIFIL dla polityki Polski wobec Bliskiego Wschodu’, PISM, 25 July 2022, pism.pl; O. Mizrahi, Y. Schweitzer, ‘Resolving the Gas Dispute with Lebanon: First Exhaust Diplomatic Efforts’, INSS Insight No. 1618, 14 July 2022, inss.org.il.

[21] An example of polemics: N. Shtrasler, ‘When Will Israel's Natural Gas Cultists Admit They Were Wrong?’, Haaretz, 13 May 2022, haaretz.com; Y. Langotsky, ‘A Myopic View on Israel’s Natural Gas’, Haaretz, 19 May 2022, haaretz.com.

[22] ‘Israel: Energy – Oil & Gas’, The Legal 500, legal500.com.

[23] The Supreme Court verdicts that are of key importance to the sector’s operation were passed relatively quickly, and have not usually caused any major delays in developing the sector. For example, in August 2012 the Supreme Court upheld the regulations adopted in March 2011 on imposing taxes on oil & gas production revenue; in October 2013 it upheld the government’s right to decide on the country’s export policy without the need to enact a relevant law each time (a decision of June 2013), and in March 2016 it overruled the 10-year contract stability guarantee that the Israeli state had pledged to the Noble-Delek consortium in an agreement signed in December 2015 (an amended contract was signed in May 2016). S. Ashwarya, Israel’s Mediterranean Gas. Domestic Governance, Economic Impact, and Strategic Implications, Routledge 2019, p. 70–129.

[24] A. Roe, ‘שנים למתווה הגז: קרן העושר כמעט ריקה, מחיר החשמל לא ירד, והתחרות מקרטעת’, Calcalist, 13 September 2021, calcalist.co.il.

[25] One possible example was the protests against the security-motivated decision to locate the installation for separating gas from natural gas condensate obtained from the Leviathan gas field a mere 10 kilometres away from the coast. Although the protests were organised by numerous local residents, their demands aroused controversy in various environmental protection organisations, and ultimately were not met. S. Surkes, ‘Energy Ministry agrees on role for public in supervising natural gas’, The Times of Israel, 14 August 2018, timesofisrael.com.

[26] Ead., ‘Knesset passes legislation to force companies to pay into sovereign wealth fund’, The Times of Israel, 11 November 2021, timesofisrael.com; ‘Record royalties collected from natural resources’, Israel’s Ministry of Energy, 28 February 2022, gov.il.

[27] Y. Katz, D. Brinn, ‘How Israel…’, op. cit.

[28] See for example Israel: The Land of Milk, Honey and Solar Power, American Friends of Bar-Ilan, 18 January 2022, vimeo.com.

[29] See e.g. ‘A plan formulated by the ministry shows how to increase the use of renewable energies without giving up open spaces’, Israel’s Ministry for Environmental Protection, 15 February 2022, gov.il; A.K. Leichman, ‘The companies that will disrupt the way we store energy’, Israel21c, 8 February 2022, israel21c.org.

[30] The Eastern Mediterranean Security and Energy Partnership Act, in H.R. 1865 (116th): Further Consolidated Appropriations Act, 2020, quoted after: govtrack.us.

[31] See for example E. Rettig, S. Polinov, S. Chorevl, ‘What does Russia want with Lebanon’s gas fields?’, The Jerusalem Post, 7 June 2020, jpost.com.

[32] K. Zielińska, ‘Izrael wobec antysemickich wypowiedzi Ławrowa’, OSW, 5 May 2022, osw.waw.pl.

[33] Source: International Energy Agency, iea.org/countries/Israel.

[34] Sources: A. Fouad, ‘Egypt’s future in the LNG market’, op. cit.; ‘Record royalties…’, op. cit.; ‘Egypt Transports 4.6 bcm of Gas for Exports in 2020/21’, Egypt Oil&Gas, 19 December 2021, egyptoil-gas.com.