A ‘last-minute’ transit contract? Russia-Ukraine-EU gas talks

On 21 January another round of trilateral gas talks between Russia, Ukraine and the European Union was held in Brussels. This meeting mainly concerned the new Russian-Ukrainian transit contract; the transit contract currently in force between Gazprom and Naftogaz will expire as of 1 January 2020. During the meeting, European Commission Vice-President Maroš Šefčovič submitted proposals to the parties concerning the parameters of a new contract transit, but did not make them public. The meeting was the latest in this series of trilateral gas talks; the previous round was held in Berlin in July 2018. In Brussels Russia declared its willingness to conclude a new transit agreement, although it highlighted the need for the legal dispute between Naftogaz and Gazprom to be resolved before that could happen.

The lack of success during the talks so far, the divergent interests of the various parties and the current political context suggests that a new contract transit will probably only be concluded by the late autumn or winter of this year, and possibly in the period immediately before the expiry date of the current contract between Naftogaz and Gazprom. It is also conceivable that the negotiations will be extended into 2020, and that meanwhile transit will take place on the basis of principles agreed in the short term, along the lines of the so-called winter packages in 2014 and 2015, something which would be very disadvantageous for Ukraine and the EU, but extremely convenient for Moscow. There is no reason to expect rapid progress in the Russian-Ukrainian negotiations; they are proceeding in complicated conditions, including the ongoing political conflict between Kiev and Moscow, the numerous legal disputes between Naftogaz and Gazprom, the construction of new Russian export pipelines, the continuing fundamental reform of the Ukrainian gas sector, and finally a packed political calendar (for both Ukraine and the EU) in 2019. The negotiation process is also difficult because of the contradiction between the long-term interests of Ukraine, which wants to maintain its status as a key transit route for Russian gas in the long term, and Russia, whose strategic goal is to become independent of the Ukrainian transmission network.

Old format – new edition

The trilateral format for talks on the transit of Russian gas via Ukraine was initiated by the European Commission in Warsaw in May 2014. According to the original assumptions, considering the de facto suspension of the Russian-Ukrainian contracts for the supply and transit of gas (both became the subjects of dispute in the arbitration proceedings), the trialogue’s[1] primary function is to work out the ad hoc rules for the supply and stable transit of Russian gas via Ukraine to the EU (the so-called winter packages)[2] every year, before each winter season. The newest version of the trialogue is aimed at developing the rules for transit cooperation between Russia and Ukraine in the longer term.

The contradicting goals of Russia and Ukraine, the complicated political context and the relentless legal claims of both parties have led to a lack of progress in the tripartite talks on gas transit.

The January talks in Brussels were attended by EC Vice-President Maroš Šefčovič, the Russian energy minister Alexander Nowak, the Ukrainian foreign minister Pavlo Klimkin, and the heads of Gazprom and Naftogaz, Alexey Miller and Andriy Kobolev. During the meeting, Vice-President Šefčovič submitted to the parties a package of compromise proposals concerning the parameters of a new contract (its duration, the volume of transit, the transit tariffs), but did not reveal them the public. According to media reports, Brussels proposed to the parties a minimum 10-year contract for the transit of 60 bcm of gas per year. The talks also focused on the issue of the implementation of the so-called Third Energy Package in Ukraine, and the demand for gas in Europe, and were preceded by bilateral meetings between the European Commission with Ukraine and Russia.[3] The trilateral meeting did not produce any measurable results on any of the topics discussed.

The context of the Russian-Ukrainian gas negotiations

The expected lack of progress in the negotiations so far is a consequence of the complex context in which they are being conducted. The ongoing legal disputes between Gazprom and Naftogaz mainly result from the verdicts by the Court of Arbitration issued in December 2017 and February 2018, which went against the Russian side. The balance sheet from the judgements reveals Gazprom’s debt to Naftogaz ($2.5 billion), which the Ukrainian side has been trying to enforce in the courts of the United Kingdom, the Netherlands, Switzerland and the US, demanding that its claims be met from the Russian company’s assets. Gazprom has consistently challenged those decisions which went against it by initiating appeal proceedings. Additionally, in July 2018 Naftogaz initiated further arbitration proceedings against Gazprom, in which it is demanding $12 billion in compensation for the losses it has incurred because of the reduced transit flows since the activation of the Nord Stream 2 and TurkStream gas pipelines.

The transit negotiations have also been hindered by Russia’s actions related to the construction of routes which can serve as alternatives to the transit of Russian gas to Europe via Ukraine. In September 2018, the construction of the Nord Stream 2 pipeline started (according to statements from Gazprom in January 2019, 20% of the pipeline has now been built). In November 2018 the construction of the marine section of the TurkStream pipeline was completed, which according to plans will be put into service in 2019 (the first branch has a capacity of 15.75 bcm, and is designed to export Russian gas onto the Turkish market). Moreover, political pressure from the US is still being exerted on Germany and the companies involved in the Nord Stream 2 project, with the aim of blocking the construction of the controversial pipeline (the threat of sanctions, supported by the US government, on companies involved in Nord Stream 2). The European Commission and some member states are also taking action to ensure the EU has jurisdiction over the project, which would greatly complicate its full use. The emergence of new routes for Russian gas exports to Europe would substantially reduce Russia’s demand for Ukrainian transit, while the uncertainty about the timing and final form of the implementation of both projects and the rules for their use makes it difficult to estimate what the actual demand for Ukrainian transit capacity over the next few years will be.

The gas negotiations are taking place in the context of continuous Russian military and economic pressure on Ukraine.

Another factor complicating the formal issues related to the possible shape of a new, long-term transit contract is the ongoing fundamental reform of the gas sector in Ukraine and the implementation of the rules of the so-called Third Energy Package[4]. One challenge may lie in the still unfinished process of unbundling, i.e. separating the different stages of the value chain in the gas sector (including activities related to gas transmission) and the implementation of network codes (including the introduction of a requirement to hold annual auctions of gas capacity).

It is also very important that the gas negotiations are taking place in the context of constant Russian military and economic pressure on Ukraine. One example of the former is the attack carried out in November 2018 on three units of the Ukrainian navy, as a result of which the Ukrainian ships and the 23 sailors on them were detained. The latest example of economic pressure is Russia’s extension in December 2018 of its list of sanctions to include selected Ukrainian enterprises and the introduction of an embargo on imports from Ukraine of a number of commodity groups. According to various estimates, this embargo could lead to a drop in the value of Ukrainian exports to the Russian Federation of about $450-550 million.

An additional complicating factor is the upcoming elections in Ukraine and the European Union. In March this year Ukraine will hold the first round of presidential elections, and parliamentary elections are scheduled for October, after which long talks on the formation of a coalition and government are likely to occur. This may mean that by the end of the year Kiev will have a problem putting a delegation together for the trilateral negotiations. In parallel, there will be elections to the European Parliament in May this year which, with regard to the formation of a new group of personnel in the EU institutions, will generally hamper their smooth operation until at least November 2019.

Russia’s strategic and tactical goals

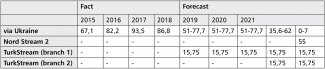

Independence from the Ukrainian transit route is one of the strategic goals of Russian energy policy. Much indicates that Russia’s main aim within the framework of the tripartite negotiations is to conclude a temporary transit agreement which would regulate the conditions for the transit of Russian gas via Ukraine until such time as it can make full use of the new gas export pipelines. In 2019, Gazprom will be able to divert a maximum of 15.75 bcm to the alternative routes; this will happen if the announced launch of the first branch of TurkStream comes to pass, as this would offer an alternative route for supplies to the Turkish market. Nord Stream 2 will be completed in 2020 at the earliest. Consequently, as shown by the data from recent years (see Table 1), Gazprom will be forced to use the Ukrainian transit network at levels of between 51 and 77.7 bcm of gas until at least 2020, unless there is a drastic fall in demand on the European market. If the Russian company can use the full transmission capacity of Nord Stream 2 and TurkStream in 2021, it will completely abandon the transit of gas via Ukraine.

Table 1. Transit of gas via Ukraine, if Nord Stream 2 and TurkStream are activated and used to full

capacity

Source: Authors’ calculations, based on data published by Gazprom[5]

So far, the statements by the Russian side suggest that Moscow is ready for several variants of compromise on the transit question.

The first involves concluding the transit contract based on the transfer of relatively small volumes (10-15 bcm). This variant was suggested back in April 2018 by Gazprom’s CEO Alexey Miller, although it is unclear whether this would be a short-, medium- or long-term contract.

Although it has declared its readiness to agree upon a new transit contract, Moscow would most prefer to conclude a temporary agreement.

The second variant would envisage guarantees of long-term transit for Ukraine, while simultaneously guaranteeing Russia the trouble-free operation of Nord Stream 2 (this could be allowed by German political action within the EU to neutralise attempts at restricting the pipeline’s operation). This variant seems more likely, as revealed by German statements during bilateral talks with Russia; this includes a statement by Chancellor Angela Merkel after talks with President Vladimir Putin in August 2018, in which she said that the launch of Nord Stream 2 should not contribute to the loss of Ukraine’s transit significance.

The third option would involve Russia’s consent to the conclusion of a long-term contract if Kiev is ready to agree upon a new supply contract. Although Ukraine is not interested in a new contract for gas supplies from Russia, it cannot be ruled out that Russia will submit a package deal in the course of further talks. This interpretation was suggested in a statement by Gazprom’s CEO Alexey Miller, who declared during the last tripartite meeting in Brussels that Gazprom “is ready to extend both of the 2009 contracts without any additional consultations”, referring to the contracts for transit and gas supplies to Ukraine. For his part, Alexander Nowak stressed that if there is a new transit contract, it should be guided by a balance of interests along the lines of what happened when the 2009 contracts were signed (the Russian-Ukrainian transit contract and the contract for the supply of Russian gas to Ukraine were signed in parallel). The Russian energy minister also added that Kiev is currently meeting Ukraine’s own gas needs from imports of Russian gas from the West, which means higher costs for gas consumers in Ukraine.

Meanwhile, Russia’s tactical aim remains the use of the tripartite negotiations to offset the losses incurred by Gazprom in its arbitration proceedings with Naftogaz. Russia has made its agreement to sign a new transit contract conditional on a resolution of the legal disputes between Naftogaz and Gazprom; this move should be interpreted as a demand for the de facto cancellation of attempts to recover the debts awarded to Ukraine by the Court of Arbitration in Stockholm. Statements made by representatives of the Russian government (including Putin) and Gazprom indicate that this is a sine qua non for the agreement of a new contract transit.

Moreover, Russia is interested in dragging out the negotiation process, counting on political changes in Ukraine after the presidential and parliamentary elections scheduled for 2019. Moscow expects that the new Ukrainian government will be willing to reach an agreement on terms which favour Russia. Besides, Russia hopes that by the end of the year it will have made significant progress in the construction of Nord Stream 2, and will be able to resolve the question of extending the TurkStream pipeline’s second branch[6], which will strengthen Moscow’s bargaining position in its talks with Kiev.

Ukraine’s objectives and strategy

Ukraine’s strategic goal is to ensure the greatest possible volume of Russian gas is transported via its territory for as long as possible. The optimal solution would be to conclude a new long-term contract with a ship-or-pay clause and high transit rates. The possible loss of transit country status would be a serious blow to Kiev, both politically and economically. In the Ukrainian government’s opinion, the Kremlin’s fear of disruption to the flow of gas to the EU was one of the most important factors which have inhibited Russian aggression against Ukraine on a wider scale. Likewise for Brussels, and also for some member states, Kiev’s transit role was the cause of the EU’s increased involvement and interest in maintaining stability on the Dnieper. On the other hand, from the economic perspective, gas transit is a very important source of income, amounting to $3 billion in 2017 and $2.2 billion during the first three quarters of 2018. This is almost equivalent to Ukraine’s total expenditure on all imported gas ($3.2 billion in 2017). According to estimates from the Ukrainian Ministry of Finance, if transit is halted, the direct losses resulting from a drop in the export of services alone will amount to 2.5-3% of the country’s GDP.

Another challenge is maintaining the viability of the transit gas transmission system (GTS). According to estimates by Naftogaz, the minimum amount of gas to be transported so that the GTS does not suffer losses is 40 bcm per year[7]. If Russian gas transmission stops completely or is limited to 10-15 bcm, doubts will arise as to whether there is any sense maintaining the expensive infrastructure capable of transporting the gas, up to 178.5 bcm annually according to Ukrainian estimates.

The possible loss of Ukraine’s status as a transit country would be a serious blow to Kiev, both politically and economically.

All this means that Ukraine is still the main opponent of Nord Stream 2 and TurkStream, and it has been leading an intensive lobbying campaign against them, primarily in EU institutions. However, the effectiveness of these activities has been severely limited due to the Ukrainian actors failing to take a consistent position. The most active role in trying to block Nord Stream 2 is being played by Naftogaz, rather than the state institutions. Initially, the company wanted to achieve this goal by attracting a Western investor for the transit gas pipelines. This solution was allowed thanks to a law on the gas market in Ukraine (adopted in 2015) which stated that the operator of gas pipelines should come from a country belonging to the European Energy Community or the United States (which clearly excludes Russia). This investor would be interested in keeping as much transit of Russian gas running via Ukraine as possible; however, their involvement would be conditional on a prior unbundling of Naftogaz, which still has not occurred because of a conflict between the company’s management and the government (in particular the representatives of the Ministry of Energy). In the absence of any coordination with the central authorities, Naftogaz’s attempts to find an investor have been doomed to failure. This has even led to a situation where the government and Naftogaz have been holding talks independently with potential investors in the Ukrainian transmission network.

The possible loss of Ukraine’s status as a transit country would be a serious blow to Kiev, both politically and economically.

Recently, Naftogaz’s management has changed tactics. On 9 January Andriy Kobolev announced that the company is willing to withdraw from the aforementioned lawsuit against Gazprom in the amount of $12 billion on condition that a new long-term contract for the transit of Russian gas is signed, although he has not given any details of this proposal.

The lack of coordination within Ukraine has also been demonstrated by the situation regarding the transit rates. The National Committee for Energy Regulation (NKRE) introduced temporary rates as of 1 January 2019, which are half the amount of the previous ones, a step which is intended to encourage EU fuel consumers to buy gas transported using the Ukrainian GTS. This move has met with sharp criticism from Naftogaz, who say that the low rates threaten the GTS operator’s financial stability.

The aims of the EU’s involvement, and the political & institutional constraints

The main aim of the EU’s involvement is to guarantee the security of Russian gas supplies to European customers. Recent proposals by the European Commission indicate that the EU would be interested in a new long-term Russian-Ukrainian transit contract. But so far there is no consensus within the EU on what specifically the future role of Ukrainian transit in supplying Russian gas to Europe should be (including what volumes and duration of the transit agreement would be desirable for European consumers of Russian gas). Countries supporting the implementation of Nord Stream 2 and/or TurkStream (such as Germany and Austria) see Ukrainian transit as an important risk factor, and seem inclined to significantly limit its role in supplying Russian gas to the EU. Meanwhile countries opposing the new Russian projects see maintaining a key transit role for Ukraine as an essential element for stability and energy security, also in the EU.

In recent months the European Commission, acting as a mediator, has included other issues relevant to Russia-Ukraine-EU gas cooperation in the transit negotiations, in particular issues regarding Nord Stream 2, amending the gas directive, the issue of unbundling in the Ukrainian gas sector and its modernisation, and finally issues of implementing the arbitration verdicts in the legal disputes between Gazprom and Naftogaz.

However, the overly broad scope of negotiations, together with a lack of unanimity within the EU as to what form of gas relations it desires with both Russia and Ukraine, has limited the effectiveness of the EU’s involvement in the transit negotiations. Another challenge may come from unilateral action by member states, which would reduce the European Commission’s effectiveness within the talks’ trilateral format. One example is the activity of Germany in 2018; in parallel with its support for the implementation of the controversial Nord Stream 2 project, began to conduct its own discussions on the future transit of Russian gas via Ukraine. This was not consulted or coordinated with other EU countries or the European Commission. Maintaining this transit was discussed both during meetings between Chancellor Merkel and President Putin, and during German-Russian meetings at the ministerial level.

Forecast for the tripartite negotiations

Although the next ministerial meeting is scheduled for May this year, it is unlikely that a new transit agreement between Russia and Ukraine will be concluded before the end of 2019. The most likely scenario is that the Russian side will drag out the negotiations for as long as possible, pending the outcome of presidential elections in Ukraine (the first round will be held on 31 March) and the parliamentary elections in October. Russia is hoping that groups will come to power in Kiev who are more inclined to compromise; it has special hopes of Yulia Tymoshenko, who in 2009 agreed to sign a gas supply agreement which was very favourable to Moscow (it is no coincidence that the next round of talks will be held after the election of Ukraine’s new president). Also, as the expiry date of the current transit agreement comes closer, the EU countries, in particular Germany, concerned about possible problems with gas supplies, could increase pressure on Ukraine to give way to the Russian demands. Finally, in the near future the effectiveness of the talks’ trilateral format, or even the EU’s entire policy in this area, will be weakened by the political calendar: on the one hand the upcoming elections to the European Parliament (and therefore the end of the mandate of both the EP and the present EC); and on the other the decision by Maroš Šefčovič, who has been conducting the trilateral talks, to stand in elections for the presidency of Slovakia (he has temporarily ceased to work for the Commission as of February this year, and will be replaced by Manuel Canete).

It thus seems very likely that the new transit contract will be agreed just before the expiry of the current transit agreement, and its final form will primarily be the result of political calculations by the entities involved in the negotiation process.

It is also possible that the negotiations will be dragged out until 2020. In this case, transit would be regulated by short-term ad hoc arrangements between the parties, like the so-called winter packages agreed in 2014-2015. This would be very inconvenient for Kiev, but nevertheless Ukraine would be interested in keeping the stable transit and maintaining its reputation as a reliable transit country. Such a situation would most of all favour Russia, in whose interests lie the transitional arrangements to ensure the transit of gas via the Ukrainian system until the new export routes can be launched. At the same time, this would pose a challenge both to Kiev (which wants to guarantee the use of its national infrastructure in the longer term) and the EU, as it seeks a more durable and stable framework for the supply of Russian gas.

[1] ‘European Commission’s statement following the meeting of EU Commissioner Günther Oettinger, Russian Energy Minister Alexander Novak and Ukrainian Energy Minister Yuriy Prodan’, 2 May 2014, http://europa.eu/rapid/press-release_MEMO-14-361_en.htm

[2] The first so-called winter package, laying down the principles for buying Russian gas by Ukraine and the transit of gas from Russia via the Ukrainian route to European customers in the period from November 2014 to March 2015, was adopted in October 2014. In September 2015 this format was also used to establish the principles of gas cooperation between Russia and Ukraine during the period from October 2015 to March 2016.

[3] ‘Statement by Vice-President for Energy Union Maroš Šefčovič following the trilateral talks with Russia and Ukraine on the future of gas transit via Ukraine’, 21 January 2019, http://europa.eu/rapid/press-release_STATEMENT-19-562_en.htm

[4] Information on the status of implementation of the so-called Third Energy Package on the Energy Community’s website. ‘State of compliance’, https://www.energy-community.org/implementation/Ukraine/Gas.html

[5] The forecast is based on the volumes of Russian gas transit via Ukraine in the years 2015-2018.

[6] Szymon Kardaś, ‘Pipeline success for Russia: TurkStream’s offshore section completed’, OSW Analyses 23 November 2018;https://www.osw.waw.pl/en/publikacje/analyses/2018-11-23/pipeline-success-russia-turkstreams-offshore-section-completed

[7] С. Головнев, ‘Сможет ли "Газпром" отказаться от украинского транзита газа’, Business Censor 14 January 2019,https://biz.censor.net.ua/resonance/3106056/smojet_li_gazprom_otkazatsya_ot_ukrainskogo_tranzita_gaza?fbclid=IwAR0ZNfqZxKqx0QsPI8gL3wqo1L8e4btxsWdoJ-anbH_ZuWXTokrYIieP82k