The European Commission enables increased use of the OPAL pipeline by Gazprom

Cooperation: Szymon Kardaś i Tomasz Dąborowski

In response to a request by the German energy regulator, on 28 October the European Commission announced its decision setting out the rules for increased utilisation by the Russian gas company Gazprom (and possibly other companies) of the onshore leg of the Nord Stream gas pipeline, i.e. the OPAL pipeline. This decision raises a series of questions as to its content, its publication procedure, the context of its adoption and its potential consequences. These doubts are aggravated by the lack of clarity of information regarding both the OPAL pipeline itself and the initial rules governing its utilisation (including its exemption from the third party access rule – TPA), and the present decision by the European Commission. As a consequence, the Commission’s decision is provoking conflicting reactions. On the one hand, it is being received (for example by the Polish and the Ukrainian side) as one that enables Gazprom to increase its access to the European market, which could compromise the security of gas supplies to Central Europe and the transit of gas via Ukraine. On the other hand, it is being interpreted as a decision which does not meet the expectations of Gazprom and the OPAL pipeline operator, which sought increased opportunities to book the pipeline’s capacity in the long term. Therefore, it is not known if and when the rules concerning the of OPAL as proposed by the EC will be implemented and, as a consequence, whether the EC’s decision will put an end to the process of negotiating the rules for the German pipeline’s use that has been ongoing for many years.

The situation so far

In 2009, the European Commission consented to the exemption of the transit part of the OPAL pipeline’s capacity (i.e. the capacity from Germany to the Czech Republic) from the TPA rule: of more than 50% (even up to 100%) of the capacity, provided that the 3 bcm per year gas release programme by companies with a dominant position on the Czech gas market is implemented[1], otherwise it would be 50% exempt. Due to the fact that the gas release programme has never been implemented, up to now OPAL has been exempt from TPA to the level of 50% and has been used (mainly by Gazprom) below its actual capacity – see Appendix 1.

For several years now, Gazprom, supported by the German regulator (Bundesnetzagentur, BNetzA), has solicited the European Commission’s consent to fully exempt the OPAL pipeline from TPA and to enable long-term booking of the pipeline’s full capacity. The apparent lack of third parties interest in the pipeline’s spare capacity was the core argument in this case. The EC avoided taking decision on this matter and was prolonging the administrative procedure, for instance, by postponing deadlines.

The Commission’s decision, vague points, doubts

In May 2016, the BNetzA submitted – pursuant to a four-party agreement concluded by Gazprom, Gazpromexport, the OPAL pipeline operator and the BNetzA[2] – another request to the EC for approval of its proposal aimed at enabling increased use of OPAL’s capacity. The deadline for considering the request was 31 October 2016 and according to Maroš Šefčovič, Vice-President of the European Commission for Energy Union, the Commission had no solid legal grounds to reject the request[3]. On 28 October, the EC announced its decision regarding the rules for OPAL pipeline use: in line with its official capacity the EC has conditionally approved the BNetzA’s proposal, requesting several changes to its content. According to its press release, the Commission:

- has set the level of OPAL’s capacity exemption from TPA at 50%;

- has decided that up to 20% of OPAL’s capacity (if there is sufficient demand) is to be made available to third parties on a short-term basis from the German Gaspool hub. Gazprom (and other companies having a dominant position on the Czech market) may bid for this capacity only at a specific base price. In the event of documented increased demand, the capacity made available to third parties may be increased;

- as a consequence, the Commission has enabled access to at least 30% of the remaining capacity with no additional conditions and/or limitations, which means that this portion of the capacity may be booked by Gazprom to thereby increase its share in OPAL’s capacity to at least 80%;

- has introduced the certification requirement as regards the OPAL operator (certification by the national regulator and the EC)[4].

The changes proposed by the EC are expected to be in effect until 2033, and they are legally binding on the German regulator which should implement them within a month. However, this is unlikely. Considering the fact that the BNetzA is obliged to consult the new rules with the interested companies, the deadline for implementing the new regulations would most likely need to be postponed for several months. Moreover, it is legally possible to appeal against the EC’s decision, and for the BNetzA to withdraw from the proposed changes in OPAL utilisation submitted in May 2016 (instead, the BNetzA could, for example, try to devise a new version of the proposal in cooperation with the OPAL operator and Gazprom).

The European Commission has not yet published the content of its decision regarding the OPAL pipeline in its official documents, and its press release raises numerous doubts, for instance due to the incomplete nature of the information contained therein. Referring to the request submitted by the German regulator and to its own previous decision (published only in German), the EC fails to explicitly state whether its present decision covers the pipeline’s full capacity or merely its ‘transit’ capacity. It also does not specify how one differs from the other in the situation of increasing integration of the German and Czech markets. Similarly, it is unclear, for example, what minimum OPAL capacity (if any) is to be made available to third parties and according to what rules this volume could be increased (or decreased).

Similarly, the very procedure in which the EC announced its decision was controversial. Unconfirmed details had been reported by the media several days before the decision was announced and when it was officially revealed at a press conference, a ban on disseminating this information was introduced, lasting for several hours (until 6 pm on Friday, 28 October 2016). This gave rise to suspicions that the EC deliberately tried to halt the spread of information and prevent prompt reactions to it. Even before its official announcement, the content of the decision was criticised by gas companies – Poland’s PGNiG and Ukraine’s Naftogaz. At the same time, it seems that the decision does not fully meet the expectations of the interested parties, including Gazprom and the OPAL operator (see Appendix 2).

Finally, the coincidence of the EC’s decision regarding the OPAL pipeline, which had been postponed for many years, with the EU-Russia talks over the increasingly likely settlement in the EC’s anti-trust proceedings against Gazprom (26 October), and the rumour suggesting that Russia has withdrawn from the construction of the Nord Stream 2 pipeline, is causing additional doubts. This coincidence prompts, for example, a question as to whether there might be a more comprehensive gas agreement between the EU and Russia. Although this would be tantamount to a rather surprising shift in the EC’s mode of operation in relations with Gazprom to date, the decision regarding the OPAL pipeline (if it gets implemented) and the possible anti-trust settlement would resolve two problematic issues that have plagued EU-Russia gas relations for years, thereby contributing to an improvement thereof.

The potential consequences

At present, it is difficult to state if and when the rules concerning use of the OPAL pipeline established by the EC will be implemented by the German regulator (see above) and whether and how Gazprom will want to take advantage of them.

However, it can be stated that the terms set by the EC enable Gazprom to apply for at least 10.2 bcm more of OPAL capacity. In this way, these terms (together with the presently considered option to increase the capacity of the Nord Stream pipeline by 5 bcm) enable increased supplies of Russian gas to the German and Central European markets. Increased supplies of Russian gas (at a potentially competitive price) via OPAL would:

– contribute to decreased demand for supplies via existing alternative routes / sources (for example the LNG terminal in Świnoujście) in Central Europe and would limit the demand for the implementation of new diversification projects;

– reduce the significance of Ukrainian transit route, at the same time boosting the importance of Germany and also the Czech Republic in the transit of Russian gas;

– raise questions regarding the likelihood of the EU’s goal involving diversification of sources of supply being attained.

The greater share of OPAL pipeline capacity available to Gazprom means that Gazprom would be able to transport more gas via Nord Stream (even more if Nord Stream’s capacity would get increased by an additional 5 bcm as planned). This could temporarily reduce Gazprom’s immediate need to build Nord Stream 2 (it would be possible to redirect more gas from the route via Ukraine and/or to offer increased supplies to the European market). At the same time, it is unlikely that Gazprom would use this as a key reason to abandon the plan to build Nord Stream 2: increased availability of the OPAL pipeline does not satisfy all the goals associated with Nord Stream 2, and the terms set by the EC may to some degree facilitate its construction as they clarify the rules covering gas transport via Germany.

Alongside this, the terms specified by the EC would force Gazprom to take a more active part in the market game: to be able to take advantage of the option for increased gas transmission via OPAL, Gazprom would have to regularly book OPAL’s capacity on a short term basis, by which it would have to increase its adaptation to the rules of the liberalising EU market.

Should capacities made available (according to the terms set by the EC) to third parties via the German Gaspool hub be utilised, this would foster greater integration of the Czech market – and potentially the entire Central European market – with the German market. In consequence, this would increase the role of Germany in the regional gas market, whereas it would lower the chances for implementation of some of regional integration projects in Central Europe (including the integration of the V4 gas markets).

Appendix 1. The OPAL pipeline and its capacity booking

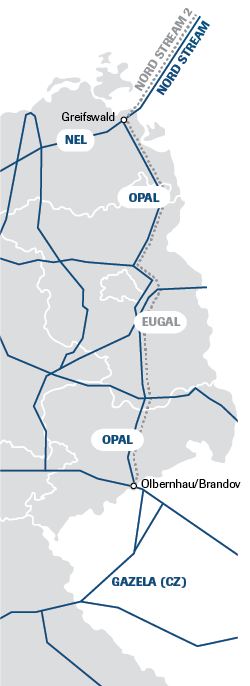

The OPAL pipeline, which runs from Lubmin near Greifswald (the entry point of the Nord Stream pipeline to the German network) to Olbernhau on the German-Czech border, was launched in 2011. It is 80% owned by the WIGA company (WIGA Transport Beteiligungs-GmbH & Co. KG – a joint undertaking of Wintershall and Gazprom) and 20% owned by the Lubmin-Brandov Gastransport GmbH company (a subsidiary of E.ON). Its capacity is 36.5 bcm.

Capacity booking:

- 6.4 bcm annually has been booked by E.ON (in connection with its 20% share in OPAL), 4.5 bcm – by the Gascade operator which makes capacity available to third parties (mainly under short-term contracts via PRISMA);

- half of the remaining 25.6 bcm is used by Gazprom (pursuant to the present exemption from TPA), and the other half has de facto remained unused.

(Agata Łoskot-Strachota)

Map. The OPAL gas pipeline

Appendix 2. Reactions to the EC’s decision regarding the OPAL pipeline

– Germany:

The media mainly emphasised the fact that the European Commission is forcing the German regulator, BNetzA, to toughen its proposal regarding the utilisation of the OPAL pipeline. It also pointed to the stance adopted by Poland, which opposes granting Gazprom special privileges on the EU market. Although the BNetzA has not yet published any press release, it did announce its plan to launch talks with those companies which are directly affected by the EC’s decision (the BNetzA is obliged to implement the EC’s decision within a month). The OPAL pipeline operator (OPAL Gastransport GmbH & Co. KG), for its part, announced in a press release that it would offer further remarks in response to the EC’s decision as soon as it obtains access to it[5]. Furthermore, it suggested that it is in the company’s interest to find a solution enabling long-term use of OPAL’s capacity. This suggests that the EC’s decision does not fully meet the operator’s expectations and the company does not regard it as final. Rafał Bajczuk

– Austria:

The tone of Austrian media reports on the EC’s decision was different from the German one. The main emphasis was placed on the fact that Gazprom gained considerable concessions from the European Commission. Another topic discussed in Austria was the impact of the EC’s decision on the construction of the Nord Stream 2 pipeline, because the Austrian company OMV is involved in it. The Wiener Zeitung newspaper wrote that the EC’s decision regarding OPAL is a positive sign in the context of investing in Nord Stream 2. It also pointed to the fact that the Polish gas company PGNiG opposed the EC’s decision. Rafał Bajczuk

– Russia:

The reactions to the EC’s decision regarding OPAL are varied. On the one hand, press reports quote positive comments suggesting that the EC’s decision, which is favourable for Gazprom, is rational and fair in the context of the present market situation (no real interest on the part of Gazprom’s competitors in utilising the ‘spare’ capacity of the pipeline; an attempt by the EU to protect itself should there be problems with the transit of Russian gas via Ukraine due to the lower level of utilisation of Ukrainian gas storage tanks than before).

On the other hand, the first public statement by a Gazprom representative, made on 1 November (4 days after the EC published its press release), increases the doubts as to whether the decision meets the Russian company’s expectations. In a TV interview, Gazprom’s vice president, Aleksandr Medvedev, said that the European Commission unilaterally made changes to the four-party agreement regarding the modes of the OPAL pipeline utilisation. Criticising the EC’s behaviour, he added that Gazprom will decide whether to accept the agreement amended by the EC after a detailed analysis of the document. Szymon Kardaś

– Ukraine:

On 27 October, before the EC had even announced its decision, Naftogaz issued a statement expressing hope that the EC’s decision regarding the utilisation of the OPAL pipeline will not only be fully in line with the EU’s energy and anti-trust legislation but also that it will take account of the EU’s intention to achieve energy independence. Furthermore, the company stated that one of the consequences of the possible increased utilisation by Gazprom of OPAL’s capacity would involve allowing the Russian company to “destroy Ukraine’s transit system as a competitor in the supply of gas to the EU states”. In its statement Naftogaz warned that, as a consequence of the EC’s decision, the volume of Russian gas transit via Ukraine will decrease considerably, as will the country’s revenue from gas transit. The presented calculations suggest that if Gazprom gains access to an additional 30% of OPAL’s capacity, then the transit of gas will be reduced by 10–11 bcm annually, and Ukraine’s revenue will decrease by USD 290–320 million. Should Gazprom gain access to 40% of OPAL’s capacity, this transit will be reduced by 13.5–14.5 bcm, and Ukraine’s revenue by USD 395–425 million.

Numerous Ukrainian politicians have expressed their concern over the EC’s decision regarding OPAL, emphasising that it would have a negative impact on Ukraine’s energy security. In the meantime, Kyiv has stepped up its plan to adopt a national programme of fuel supply diversification, particularly for gas. The Supreme Council is preparing a special appeal to the parliaments of EU states and the EU’s executive bodies regarding the risk involved in the implementation of new gas pipeline projects that bypass Ukraine. Wojciech Konończuk

– Central Europe:

The authorities of the Czech Republic, Slovakia and Hungary have offered no official reaction to the EC’s decision regarding OPAL. As far as the energy companies operating in these states are concerned, only the Czech company EPH (co-owner of the Slovak transit pipeline Eustream) has presented its stance. The Czech company announced that taking into account the ship-or-pay clause (Gazprom is obliged to ship 50 billion m3 via Slovakia by 2028) and the actual distribution of gas transmission in Europe, it does not expect its profit to decrease as a result of the EC’s decision.

The lack of reaction on the part of the Czech authorities to the EC’s decision seems to result from the fact that although Prague positively assesses the prospects of increasing gas transport via OPAL, it does not intend to emphasise that its interests are separate from the interests of Bratislava and Warsaw. Czech media, for its part, has openly discussed the issue of Czech interests in the context of the OPAL pipeline, claiming that the EC’s decision is favourable for the German-Canadian company Net4Gas (the owner and operator of the Gazelle pipeline which is an extension of the OPAL pipeline) and at the same time favourable for the Czech Republic, due to the expected increase in profit from the transport of gas via the country.

The absence of comment offered by the authorities of Slovakia on the EC’s decision regarding OPAL seems to confirm the government’s waning criticism of the Nord Stream 2 project. As a country holding presidency of the EU Council, Slovakia prefers to play the role of a moderator in the debates within the EU, and a dispute with the EC over OPAL would be tantamount to a dispute with Maroš Šefčovič – Vice-President of the European Commission for Energy Union. The Slovak government cooperates with Šefčovič and seems to regard the EC’s decision as a poor solution which nonetheless is the best of all the currently feasible solutions. Moreover, through Šefčovič it seems to be trying to underline its primary interest in the energy policy, i.e. to continue gas transit via Slovakia, most preferably by maintaining the transport of Russian gas via Ukraine. In the event of increased transport of Russian gas via OPAL, Bratislava would likely intend to make up for the expected decrease of gas transport from Ukraine with increased transport of gas from the Czech Republic.

Silence on the part of Hungary with regards to the EC’s decision over OPAL is connected with the fact that, on the one hand, Budapest fears the construction of Nord Stream 2 and the expected significant reduction of gas transport via Ukraine, yet on the other hand, it does not intend to aggravate its relations with Moscow. Both the government and the energy companies are satisfied with the present terms of gas cooperation with Russia. Budapest’s support for Visegrad Group’s political initiatives targeting the Nord Stream 2 project is largely determined by the intention to tighten Central European cooperation. It also forms part of the strategy to make plain the lack of consent for ‘unequal’ treatment by the European Commission for various projects (disagreement with the EC over the reservations regarding South Stream). It should not be expected that it will trigger any official decisions (e.g. appealing against the EC’s decision, arbitration with Gazprom). Jakub Groszkowski

[1] Cf the European Commission’s decision of 2009: https://ec.europa.eu/energy/sites/ener/files/documents/2009_opal_decision_de.pdf

[2] Agreement of 31 October 2013 („ursprünglicher Vergleichsvertrag”):http://www.bundesnetzagentur.de/DE/Service-Funktionen/Beschlusskammern/1BK-Geschaeftszeichen-Datenbank/BK7-GZ/2008/2008_0001bis0999/2008_001bis099/BK7-08-009_BKV/Ver%C3%B6ffentlichung_Aktuelles_BF.pdf?__blob=publicationFile&v=5

Agreement of 7 July 2009:

Agreement of 25 February 2009: http://www.bundesnetzagentur.de/DE/Service-Funktionen/Beschlusskammern/1BK-Geschaeftszeichen-Datenbank/BK7-GZ/2008/2008_0001bis0999/2008_001bis099/BK7-08-009_BKV/BK7-08-009_Beschluss_vom_25022009_bf.pdf?__blob=publicationFile&v=6

[3] Cf the statement by Maroš Šefčovič regarding OPAL during the Tatra Summit in Bratislava on 28 October 2016: https://www.youtube.com/watch?v=N5acXNISQNM (the question regarding OPAL – 8:53, Šefčovič’s reply – 15:47)

[4] Gas markets: Commission reinforces market conditions in revised exemption decision on OPAL pipeline, Brussels, 28 October 2016, http://europa.eu/rapid/press-release_IP-16-3562_en.htm

[5] OPAL Gastransport GmbH & Co. KG examines decision by the European Commission, 31 October 2016, https://www.opal-gastransport.de/fileadmin/Press_PDF_OPAL/OPAL_PR_161031_Decision_European_Commission.pdf