‘The oil friendship’: the state of and prospects for Russian-Chinese energy cooperation

Cooperation: Jakub Jakóbowski

The oil sector has been the major element of Russian-Chinese energy cooperation. The years 2013–2015 saw a significant increase in the volume of crude oil exported by Russia. In 2015, China became the main importer of Russian oil; Russia became the second largest supplier of oil to the Chinese market, after Saudi Arabia. From Beijing’s perspective, supplies of Russian oil are of strategic importance because the main supply routes are overland routes. Russia, for its part, is interested in boosting its export because of its deteriorating position on the European market, which hitherto has been considered a strategic market.

Cooperation in the field of natural gas has been less advanced; so far Russia has exported only insignificant amounts of liquefied natural gas (LNG) to China. China is less dependent on the import of gas (its own production covers around 70% of the demand). Beijing has been dynamically developing its LNG infrastructure, and has at its disposal gas pipelines which connect China with producer countries in Central Asia. Additionally, all the projects carried out within the framework of Russian-Chinese gas cooperation are being hampered by the financial problems Moscow is experiencing.

Energy cooperation is and will remain the most important component of Russian-Chinese economic relations. In the present form of this cooperation, Russia has mainly played the role of China’s oil base. The process of Chinese companies investing in oil production in Russia is progressing more slowly than before; most of the agreements made regarding this matter are still framework agreements. In the mid-term perspective, however, a qualitative change to the present model should be expected. It is very likely that Chinese companies will enter the Russian upstream sector, especially taking into account the financial standing of the Russian energy sector and China’s interest in gaining direct access to oil fields.

Record high crude oil supplies

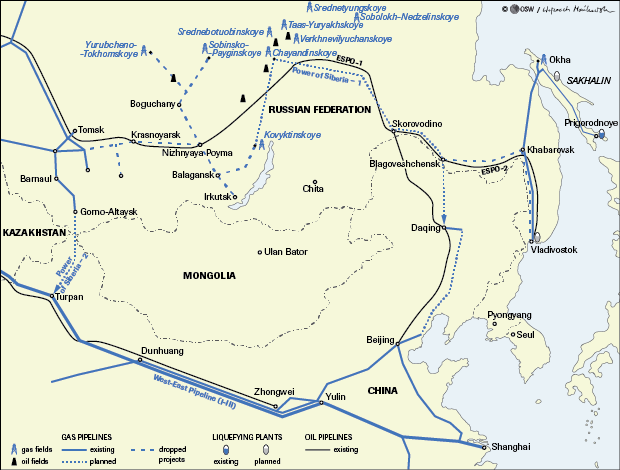

The dynamics in Russian-Chinese energy cooperation[1] are reflected mainly in the significant increase in the volume of crude oil supplies from Russia to China (from 24.4 million tonnes in 2013 to 41.29 million tonnes in 2015). Russia’s state-controlled oil company Rosneft has been the biggest supplier. Its export to Chinese contractors recorded an almost two-fold increase, from 16.55 million tonnes in 2013 to 30.3 million tonnes annually in 2015 (for detailed figures see the Appendix). The main export channel is the branch of the East Siberia–Pacific Ocean (ESPO) oil pipeline, running to China. Half of the oil exported by Rosneft is currently supplied via this branch. The rest of the supplies reach China via the Kozmino sea terminal and as part of swap transactions with Kazakhstan (Rosneft supplies around 7 million tonnes annually to northern regions of Kazakhstan, and in exchange Kazakhstan supplies its own oil to China using the Atasu-Alashankou pipeline[2]).

China’s import of crude oil is well-diversified. The share of each individual supplier in this import does not exceed 20%. From Beijing’s perspective, the supplies of oil from Russia have privileged status due to their strategic importance. The major portion of the oil China imports is supplied via an overland pipeline which connects the two countries with no transit states between them. This makes it possible to reduce the share of oil imported from the Middle East, which currently accounts for more than a half of total oil imported by China. The Middle East is increasingly exposed to geopolitical turbulence. Similarly, the maritime oil supply routes run through several ‘bottlenecks’, mainly the Strait of Malacca, which would be easy to block in case of a conflict. The years 2013–2015 saw an increase in the importance of the share of oil imported from Russia in the total volume of oil which China imports. In 2013, Russia as a supplier was ranked fourth (8.6% of China’s total import), whereas in 2015 it was ranked second (12.3%)[3].

On one hand, numerous factors in China are fostering an increase in the import of crude oil from Russia. First, the Chinese domestic market is applying a mechanism of administrative control on the prices of petroleum products which links these prices to global oil prices. In reaction to the drop in the price of oil, in January 2016 price brackets between US$40 and US$130 per barrel were introduced (when the price falls below US$40, Chinese oil extraction is no longer profitable for the producers). In practice, this means that oil companies, in particular Sinopec and CNPC (PetroChina), are allowed to sell petroleum products at a price much higher than the global price, thereby boosting their revenues. Additionally, the Chinese leadership has allowed numerous small refineries to operate in the oil processing sector. Another factor boosting China’s demand for crude oil has been the creation of strategic reserves by Beijing. China intends to create reserves by 2020 which would cover a 100-day demand for oil. Chinese reserves are currently (early 2016) estimated at a volume able to cover a 29-day demand.

Russia has been interested in increasing its exports to China. One of the main reasons behind this are the negative trends observed on the European market (a gradual decrease in Russia’s export recorded in 2011–2014), which hitherto has been considered a strategic market. Another reason involves long-term forecasts regarding the consumption of crude oil in Europe, which are unfavourable to Russia.

On the other hand, however, one of the barriers to a continuing dynamic increase in the export of Russian oil to China may be infrastructural problems and delays in exploring the fields which are intended to be the raw material base for new supplies. Pursuant to an agreement signed in 2013, Rosneft committed itself to double its export to China, from 15.8 million tonnes in 2013 to 30 million tonnes annually in 2018–2030. This increase in the volume of supplies should have been effected via the ESPO pipeline branch. However, due to delays in constructing the infrastructure, which according to the Russian media were caused by China, the increased supplies were delivered via the Kozmino sea terminal and in swap operations with Kazakhstan. Transneft announced a plan to expand the capacity of the ESPO pipeline from the present 58 million tonnes to 80 million tonnes in 2020. Similarly, there are plans to expand the Kozmino sea terminal to reach a capacity of 36 million tonnes annually by 2017 (according to Transneft, an expansion to exceed 36 million tonnes would not be possible for technical reasons). If further delays prevent Rosneft from increasing its export to China using the ESPO pipeline, the rivalry between Rosneft and other Russian oil exporters over export quotas enabling the supplies of oil via Kozmino is likely to increase. For Russian oil-producing companies, the Kozmino port has been a relatively profitable export channel.

The waning ‘Powers of Siberia’: increasing problems of gas pipeline projects

So far, Russian-Chinese cooperation in implementing joint gas pipeline projects has been much less successful.

The construction of the Power of Siberia-1 gas pipeline has been experiencing repeated problems (the project is intended to enable the export of Russian gas from Eastern Siberian fields to China). In 2015, Gazprom launched the construction of a new pipeline[4], but at the same time it repeatedly changed its plans regarding the deadline for finishing the works and launching the supplies. Back in December 2014, Gazprom representatives suggested that the maximum contractual volume of supplies agreed in May 2014 (38 bcm of gas annually) would be reached in 2024[5]. However, in May 2015, during a special news conference focusing on Gazprom’s strategy in South-East Asia, it was mentioned that this level could be reached in 2024–2031. The planned route of the constructed Power of Siberia pipeline has also been changed. Originally, the pipeline was intended to connect the Eastern Siberian Kovykta and Chayanda fields with Blagoveshchensk, and further with Khabarovsk and Vladivostok (see Map). A statement published by Russia’s Energy Ministry in February 2015 suggests that the project no longer involves the construction of the Khabarovsk-Vladivostok section, which is likely to be a consequence of Gazprom’s withdrawal from its plan to build an LNG terminal in Vladivostok.

The Power of Siberia-1 pipeline has experienced financial problems regarding the expansion of its infrastructure. Real investment expenditures for the construction of the Power of Siberia pipeline were included in Gazprom’s budget only in 2015, and their amount is insignificant (30.98 billion roubles, which accounts for a mere 7% of total funds earmarked by Gazprom for investments involving the construction of gas pipelines). Back in the summer of 2015, plans were made to invest around 200 billion roubles in the construction of the Power of Siberia during 2016. However, in January 2016 the planned amount was reduced to a mere 92 billion roubles. In December 2015, Gazprom cancelled tenders for the construction of around 800 km of the gas pipeline. The official reason behind this decision was reservations raised by the Russian Federal Antitrust Service, although the true cause might have been Gazprom’s difficult financial standing. Equally surprising is the fact that Gazprom has not yet updated the most recent total cost calculation regarding the construction of the new pipeline, which was prepared in 2011 (at that time, the cost of constructing 3246 km of the pipeline was estimated at 800 billion roubles).

Secondly, another important factor involves serious delays in exploring the gas fields intended to be the project’s raw material base. Gazprom had already taken account of these delays at the present stage of project implementation. The Chayandinskoye gas field is expected to reach its maximum output (22 bcm of gas annually) no sooner than 2022, whereas the Kovyktinskoye field is expected to increase its production from the planned 5 bcm of gas annually in 2022–2023 to 13 bcm of gas annually in 2024–2031. At the same time, Gazprom representatives have indicated that the agreement with CNPC provides for the possibility to delay the launch of supplies for three years, which means that the deliveries will most likely be launched in 2021 (originally, the first deliveries were scheduled for 2018).

Thirdly, China has been less interested in importing gas from Russia than in importing Russian oil. On the one hand, the Chinese economy has been less dependent on the import of gas. In 2014, China imported 31% of the natural gas it consumed, i.e. 58 bcm (total consumption was 183 bcm). The capacity of the present pipelines running from Central Asian countries and Burma is 70 bcm, and is expected to rise to 90 bcm by the end of the present decade. In 2014, China used only 50% of this capacity, importing just 31 bcm. In 2015, the volumes of gas consumption and import remained largely the same`, and reached 191 bcm and 62 bcm respectively. This is to be supplemented by the increasing capacity of LNG terminals which China uses to import less than 50% of its gas. Even if the planned Power of Siberia pipeline is fully used, supplies from Russia would account for half of the planned import from Central Asian countries, and would have to compete with supplies of liquefied gas.

Despite the above-mentioned difficulties and the unavoidable delays, the Power of Siberia-1 pipeline will eventually be constructed because both sides are truly interested in its completion. Russia treats the gas infrastructure currently being expanded as an important element of the programme of gasification of Eastern Siberia and the Far East. China, for its part, is mainly interested in covering the regional demand for gas in the north-eastern part of the country. In December 2015, this region experienced problems with ‘unloading’ LNG, as a result of which CNPC was forced to reduce its supplies to some of its industrial recipients.

However, there is still little progress in the negotiations over the Power of Siberia-2 project (formerly the Altai project), which involves the construction of a gas pipeline to connect Russia’s Western Siberian fields with China’s north-western provinces. Gazprom has been pushing this project forward since 2006. Its implementation would enable Russia to strengthen its negotiating position towards its European clients; the raw material base for the supplies would involve the same fields which contain gas supplied to European recipients (according to Gazprom, these are mainly the Zapolyarnoye field [3.3 trillion m3 of gas] and the Yuzhnorusskoye field [1.03 trillion m3 of gas])[6]. So far, only a series of framework agreements concerning the project has been made[7]. It should be remembered that the Russian leadership and Gazprom representatives have repeatedly suggested that the contract could have been signed in 2015, although its conclusion in the upcoming months is increasingly less likely.

From Beijing’s perspective, the biggest obstacle to the construction of the pipeline’s western section involves the need to deliver gas to locations along the eastern and the southern coast, which are separated by a distance of several thousand kilometres. The present network within the Chinese West-East Pipelines (WEP) is composed of three branches with a capacity of 77 bcm (including 60 bcm for Central Asian gas and 17 bcm for gas extracted in Xinjiang). The planned fourth and fifth branches are expected to reach their total capacity of up to 50 bcm (including 25 bcm for Central Asian gas, and the remaining portion for the gas from Xinjiang). The Altai gas pipeline would require the construction of a sixth branch.

The programme of expanding LNG terminals which Beijing has been dynamically implementing can be considered another factor strengthening China’s negotiating position in the talks over the import of gas from Russia. In 2013–2015, up to 11 LNG terminals, with a total regasification capacity of 32.4 million tonnes, were put into operation. This means that at the beginning of 2016 China was running 17 terminals with a total regasification capacity of 54.6 million tonnes annually (see Appendix: Table 1).

Framework agreements in the oil and gas production sector

So far, China’s involvement in the Russian production sector has been insignificant (see Appendix: Table 2). Over the last two years, Moscow has become more determined to encourage Chinese capital to invest in the Russian production sector. In September 2014, President Vladimir Putin announced that Russia would be willing to offer Chinese companies shares in strategic oil and gas deposits[8]. In February 2015, Russia’s Deputy Prime Minister Arkady Dvorkovich said that this offer could even involve controlling stakes[9].

So far, most of the agreements regarding China’s investments in oil production projects in Russia have been framework agreements, although it is likely that some of them will be finalised. Rosneft has been particularly interested in attracting Chinese capital. Back in 2013, Rosneft offered CNPC shares in the Taas-Yuryakh Neftegazodobycha company which operates the Srednebotuobinskoye gas field (Eastern Siberia), although as yet no final deal has been struck[10]. In November 2014, Rosneft signed a framework agreement on the purchase by the Chinese CNPC company of 10% of shares in the Vankor oil field located in Krasnoyarsk krai and owned by Rosneft. In September 2015, Rosneft entered into an agreement with the Chinese petroleum processing company Sinopec on cooperation in exploring Russia’s Russkoye and Yurubcheno-Tokhomskoye oil fields in Eastern Siberia (the agreement grants 49% of shares in each field to the Chinese partner). The oil from the Yurubcheno-Tokhomskoye field is to be exported to China via the ESPO pipeline. Although these transactions look very promising, their finalisation might be delayed. Rosneft’s negotiating position has recently been weakened due to the Western sanctions against Russia, which have limited Moscow’s access to Western capital.

Any tightening of Russian-Chinese relations in the gas production sector in the coming years is rather unlikely. On one hand, Gazprom has expressed its interest in cooperation in this area, as evidenced by general agreements signed with Chinese companies, such as the memorandum signed with CNOOC in November 2014 and the framework cooperation agreement signed with CNPC on 8 May 2015. On the other hand, announcements by Gazprom representatives suggest that the participation of Chinese companies in production projects in Russia would be possible only if Gazprom were granted similar operation opportunities in China, which seems very unlikely in the coming years.

As far as possible projects to be implemented by Chinese companies and Rosneft are concerned, the fact that Rosneft has no licence to export gas might be a problem (so far, Gazprom has had a monopoly on the export of gas via the pipeline system, granted to it by the relevant law). Back in 2014, President Putin ordered the government to devise a plan to grant the so-called independent gas producers access to export pipelines, but the difficult financial standing of the Russian energy sector (including Gazprom itself) could delay the final decision on this matter for several years at least. Moreover, the major Eastern Siberian gas fields owned by Rosneft, the Yurubcheno-Tokhomskoye field (around 152.4 bcm of gas) and the Srednebotuobinskoye field (around 155 bcm), are located far away from the planned route of the Power of Siberia pipeline (the distance between the Yurubcheno-Tokhomskoye field and the planned pipeline is around 1000 km).

Cooperation in the LNG sector: moderate progress

So far, Russian-Chinese cooperation in the LNG sector has been limited to Gazprom exporting a minor volume of liquefied gas to China, and to China’s involvement in the implementation of the Yamal-LNG project.

Despite the fact that Russian supplies of LNG to China were launched in 2009, their volume continues to be insignificant. In 2012–2014, it gradually decreased (0.38 million tonnes in 2012 and a mere 0.13 million tonnes in 2014). China is therefore not a significant market for Russian LNG (it accounts for 1.2% of total Russian LNG export). Similarly, for China the Russian liquefied gas is not an important source of supplies, as it accounts for a mere 0.65% of China’s total LNG import.

Russia’s most promising liquefied gas project, the so-called Yamal-LNG, has experienced major problems regarding sources of funding. The project’s shareholders include Novatek, Russia’s second largest gas producer after Gazprom (50.1%), the French company Total (20%), the Chinese company CNPC (20%) and the Chinese Silk Road Fund (9.9%). In May 2014, CNPC signed an agreement with the consortium for the purchase of 3 million tonnes of LNG annually. Only to a limited extent were external sources of funding obtained for the project (according to the original plans, they were to have accounted for 70% of the total budget, now estimated at US$27 billion). Novatek is subject to sanctions, and has limited opportunities to obtain capital from Western or Russian banks[11]. The company has only managed to win support in the form of 150 billion roubles from the Russian National Welfare Fund by selling its bonds to state-owned banks: it obtained 75 billion roubles (around US$ 1.2 billion at the exchange rate of that time) for the bonds it sold on 19 February 2015; the second portion of bonds, worth 75 billion roubles, was sold in September 2015. Russia expects to obtain the missing funds (around US$12–14 billion) from loans from Chinese banks; so far only preliminary agreements have been made regarding this issue. By now, the Chinese side has offered a loan amounting to a mere €730 million.

In the present conditions, the implementation of new Far Eastern LNG projects to supply the Chinese market seems rather unlikely. Due to financial difficulties, these projects are likely to be considerably delayed, and some of them even abandoned, such as the Vladivostok LNG (implemented by Gazprom) or the Far Eastern LNG (implemented by Rosneft) projects. Similarly, the fact that the Yuzhno-Kirinskoye field in Sakhalin has been subject to American sanctions is likely to delay the plans to expand the liquefying plant under the Sakhalin-2 project (this field was intended to be the raw material base for the planned third branch of the terminal).

Prospects for the development of energy cooperation

There has been dynamic progress in cooperation in increasing the volume of supplies of crude oil. However, Russian and Chinese companies have been unable to close any agreement regarding investments in the oil production sector for over a decade. The biggest suspected obstacle to increasing the volume of exports of Russian oil to China can be associated with the existing potential for extracting oil in Eastern Siberia. In this situation, the future development of cooperation could involve specifically Chinese investments in the upstream. These investments are likely to be fostered by both the rising political importance of cooperation with China as perceived by Russia and the growing financial needs of the Russian oil sector, in particular if the sanctions imposed by the West remain in force.

In the case of the gas sector, the prospects for launching exports of Russian gas via the pipeline system, which would boost Russia’s importance in China’s eyes, remain less promising. It should be expected that the launch of the Power of Siberia-1 pipeline will be delayed, and that a decision to construct Power of Siberia-2 will remain in the realm of plans, similar to other initiatives (involving, for example, the project to export gas via the system of pipelines from Sakhalin to China). Equally uncertain is the participation of Chinese companies in gas upstream projects carried out in Russia. In this context, the most promising area of cooperation involves the LNG sector, mainly the implementation of the Yamal project. This cooperation could gain new quality if big loans (in the amount of between ten and twenty billion US dollars) were granted by Chinese banks for the purpose of implementing the Yamal-LNG project.

Appendix

Table 1. Operating and planned LNG terminals in China

|

|

2012 |

2015 |

2017 (planned) |

|

Number of operating terminals |

7 |

18 |

22 |

|

Total regasification capacity of the operating terminals (in million tonnes) |

22.2 |

54.6 |

64.6 |

Authors’ own analysis, based on figures published in World LNG Report 2015.

Table 2. China’s involvement in the production sector in Russia

|

Chinese partner |

sector |

Russian partner |

Type of involvement |

|

CNPC |

oil |

Rosneft |

Vostok Energy Ltd.; exploration of resources of Verkhneicherskoye and Zapadno-Chonskoye fields located in Irkutsk oblast (Eastern Siberia) |

|

gas |

Novatek |

20% of shares in the Yamal-LNG project |

|

|

Sinopec |

oil |

Rosneft |

Participation in the Sakhalin-3 project (25.1%); exploration of the Veninsky block |

|

oil |

Rosneft |

49% of shares in the Udmurtneft company; oil production (around 6.5 million tonnes annually) |

Authors’ own analysis, based on figures published by news agencies Argus and Interfax.

Table 3. Export of Russian crude oil to China in 2013–2015 (in million tonnes)

|

|

Exporter |

2013 |

2014 |

2015 |

|

via the Kozmino port

|

Rosneft |

0.9 |

2.2 |

7.3 |

|

Surgutneftegaz |

2.2 |

1.4 |

3.6 |

|

|

Gazpromneft |

0.1 |

0.6 |

1.2 |

|

|

minor producers |

1.3 |

1.5 |

2.21 |

|

|

TNK-BP |

0,9 |

0 |

0 |

|

|

LUKoil |

0.2 |

0.1 |

0.64 |

|

|

Total |

5.6 |

5.8 |

14.95 |

|

|

via the ESPO branch |

Rosneft |

15.75 |

15.6 |

16 |

|

via Kazakhstan |

Rosneft |

0 |

7 |

7 |

|

other routes |

companies total |

3.35 |

4.7 |

3.32 |

|

total (all routes) |

companies total |

24.4 |

33.1 |

41.29 |

Authors’ own analysis, based on figures published by news agencies Argus and Interfax.

Map

Russian-Chinese energy projects

[1] This text focuses on the oil and gas sector. Cooperation in the electrical energy sector has been rather inert, and is limited to Russia selling relatively small amounts of electrical energy to China. Pursuant to the contract signed in 2012, Inter RAO exports electrical energy to the Chinese market. The contract has been signed for 25 years and envisages a total export of 100 billion kWh, which in practice means that annual export volume will not exceed 4 billion kWh. In 2014, the export volume was 3787.58 million kWh (an increase of 3.6% against 2013) worth US$164.42 million (a drop of 11.9% against 2013, when the figure was US$186.49 million)[1]. In the first three quarters of 2015, Russia’s export was 2617.65 kWh, worth US$134.92 million. http://www.ved.gov.ru/exportcountries/cn/cn_ru_relations/cn_ru_trade/

[2] The agreement provides for the possible increase in the volume of transported oil to 10 million tonnes annually. The relevant agreement between Russia and Kazakhstan was signed on 24 December 2013.

[3] In some months of 2015, supplies from Russia exceeded those from Saudi Arabia.

[4] The first section of the pipeline from Chayanda to the city of Lensk (208 km) is to be constructed by Stroytransgaz (according to information provided by Gazprom, in 2015 about 50–60 km of the pipeline had been built).

[5] Проектный объем поставок газа в Китай по "Силе Сибири" будет достигнут в 2024 году,

http://tass.ru/ekonomika/1644464 (10 January 2016).

[6] In August 2014, President Vladimir Putin announced that under the Eastern Gas Programme gas networks in western and eastern regions of Russia will be connected, however, in May 2015, during a news conference, Gazprom representatives said that these concepts were no longer valid and are economically unprofitable.

[7] The most recent general agreements were signed in Beijing in November 2014 and in Moscow in May 2015, respectively.

[8] Russia’s President has said that “for our Chinese friends there are no limits”. Для китайских друзей ограничений нет, http://www.gazeta.ru/business/2014/09/01/6199073.shtml

[9] Дворкович пообещал Китаю контроль над российской нефтью, http://www.vedomosti.ru/newspaper/articles/2015/03/01/neft-techet-v-kitai. Pursuant to the current regulations in force in Russia, foreign companies are free to purchase packages not exceeding 10% of shares in production projects; in early 2015 the Ministry of Natural Resources prepared a proposal to increase this limit to 25%, and to 49% with consent from the authorities. According to Russian law, strategic fields are those which contain at least 70 million tonnes of oil or 50 bcm of gas.

[10] In early 2015, Rosneft signed a preliminary agreement for the sale of 20% of shares in this company to the British company BP.

[11] Gazprombank and Vneshekonombank were expected to offer loans for this project, but they were covered by Western financial sanctions, which considerably worsened their financial standing.