Ukraine: two years’ free trading of arable land

Two years ago, on 1 July 2021, a law on the land market came into effect which enabled trade in arable land for the first time in the history of independent Ukraine. Over these 24 months, more than 400,000 hectares of land have been sold, accounting for around 1.5% of the land covered by this law. Although the Russian invasion launched in February 2022 triggered a short-lived slump, within two months the land market started to recover, although the transaction dynamic has not returned to pre-war levels. The average price of one hectare of land is less than €1000, several times cheaper than in neighbouring EU countries. Some increase in the number of land purchase contracts can be expected starting from the beginning of 2024, when trade in land will be opened up to companies rather than natural persons alone. However, due to high loan interest rates and the uncertainty resulting from the war, it seems unlikely that the sale of agricultural land will continue on a mass scale.

The land market law

On 31 March 2020, the Ukrainian parliament enacted a law which lifted the former moratorium on trade in arable land. For the first time in the history of independent Ukraine, this allowed owners of agricultural land to sell it. The document came into effect on 1 July 2021 and stipulated that in the initial stage of its legal validity (that is, until the end of 2023) only natural persons would be able to acquire land, with no more than 100 ha in each transaction. From 1 January 2024, legal entities will also be granted this right, and the limit will be raised to 10,000 ha. In both cases only citizens of Ukraine and companies with no foreign capital are allowed to make such transactions. The law covered 27 million ha of land owned by the public, but the sale of state and municipal land remained prohibited.

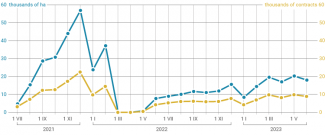

According to data compiled by the State Service of Ukraine for Geodesy, Cartography and Cadastre (SSUGCC), over the two years of the land market’s operation (that is, until 1 July 2023) nearly 190,000 contracts have been signed pertaining to the sale of 417,000 ha of land. In the first months after the law came into effect, the market began to grow quite dynamically: in the peak period in December 2021 57,000 plots of land with a total acreage of 22,500 ha were sold (see Chart 1). However, the Russian invasion caused a temporary slump: in March and April 2022 no transactions were recorded, but in May the market gradually started to recover.

Chart 1. Monthly change in the number of contracts and the acreage of arable land sold

Source: the State Service of Ukraine for Geodesy, Cartography and Cadastre.

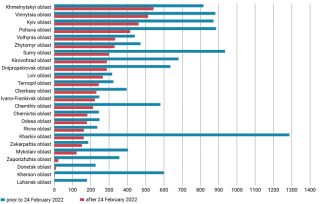

The invasion’s impact on the market varied depending on the region affected. In those oblasts which are under full or partial occupation (such as Kherson, Donetsk and Zaporizhzhia oblasts), transactions were effectively halted (see Chart 2). In those regions which were temporarily controlled by Russian troops (such as Kharkiv, Sumy and Chernihiv oblasts) a major decrease in the number of signed land purchase contracts was recorded. This was mainly for security reasons, including the continued shelling of cross-border areas and some areas being mined. As regards the regions in western and central Ukraine, the war’s impact on the number of contracts was limited or insignificant.

Chart 2. Comparison of the average number of transactions carried out monthly in specific oblasts prior to and after 24 February 2022

Source: the State Service of Ukraine for Geodesy, Cartography and Cadastre.

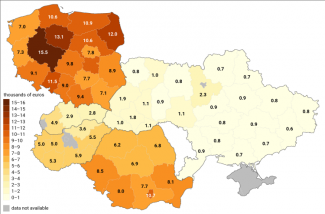

The price of arable land

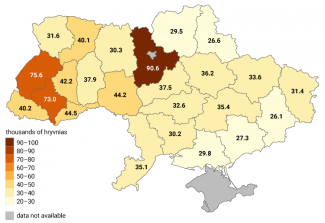

The average price of one hectare of arable land also varies depending on the region. It should be noted that no complete data on this issue is available because the SSUGCC has no information regarding the transaction value of the majority of the contracts signed. The high price of land in Kyiv and Lviv oblasts (see Map 1) is most likely due to the practice of buying plots of land in the vicinity of big cities in order to transform them later into building plots. Moreover, it seems that the average price depends on the distance from the front line, rather than on the quality of soil in the specific area. As a consequence, relatively less fertile land in western Ukraine is more expensive than land located in the south-eastern part of the country, which before the war accounted for the majority of Ukraine’s agricultural production.

Map 1. Average price of 1 ha of arable land in specific oblasts

Source: the State Service of Ukraine for Geodesy, Cartography and Cadastre.

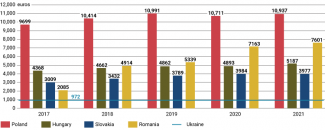

According to the SSUGCC, over the two years since the land market was opened up, the average price of 1 hectare of land was 39,000 hryvnias (around €970) and remained stable throughout this period. As mentioned above, this price is much lower than in Ukraine’s EU neighbours (see Chart 3), and this has not changed in the last ten years.

Chart 3. Comparison of the average price of 1 ha of land in Ukraine and in the neighbouring EU countries

Source: Eurostat.

The difference in the price of arable land in Ukraine and in the neighbouring EU countries is even more evident at the regional level. Even in Slovakia’s mountainous regions the price of land is higher than that in Kyiv oblast, and in the Polish voivodships bordering on Ukraine the prices are several times higher.

Map 2. The average price of 1 ha of arable land in Ukraine and in the neighbouring EU countries in 2021

Source: Eurostat, the State Service of Ukraine for Geodesy, Cartography and Cadastre.

Outlook

It seems that by the end of this year – that is, the period in which only natural persons are allowed to buy land – no major increase in the number of transactions should be expected. It remains to be seen whether the decision to allow companies to buy land starting from 1 January 2024 will be a major spur to the land market’s development. Most likely the number of contracts will grow, although numerous factors will curb the extent of this increase. The anti-concentration regulations (according to which corporate buyers will not be allowed to acquire more than 10,000 ha of land) will exclude the biggest agricultural holdings from the market. However, it is difficult to assess whether small- and medium-sized agricultural companies will have access to funding. The absence of clear prospects regarding the export of agricultural produce, both by sea and by land to Ukraine’s EU neighbours, may be another factor discouraging the potential investors. Although a certain increase in the price of land is likely, it will be limited to Ukraine’s western and central regions, which are located at considerable distances from the front line. Even if the war ends in the next few months and the occupied territories are liberated, farming activities will not resume in these areas any time soon because of the damage to the irrigation systems and problems caused by mines and unexploded shells.

In theory, the opening up of the agricultural land market to foreign capital could trigger its rapid development. This is because, given the huge differences in land prices between Ukraine and the EU, this capital could be interested in investing in Ukrainian agriculture even in a situation of ongoing war. The law envisages the possibility of foreigners acquiring land, provided that this is approved in a nationwide referendum. However, it is impossible to hold such a referendum as long as martial law is in place. Moreover, taking into account public sentiment as recorded in previous years (before the war a mere 15% of Ukrainians supported the proposal to enable foreigners to buy Ukrainian land), a positive outcome of this referendum should be considered unlikely.