Back to discipline: How Germany views the reform of EU budgetary rules

One of the topics to be discussed at the European Council on 23–24 March 2023 is the reform of the Stability and Growth Pact (SGP), a system of rules aimed at maintaining the fiscal discipline of EU member states. These rules have for years been a source of conflict between advocates of greater flexibility and discretion in budget expenditure (especially during crises) and defenders of macroeconomic stability and a restrictive approach to public finances. The dispute has been less pronounced in recent years as the pact was suspended during the pandemic. However, the relaxation is coming to an end in 2023, so the issue of reforming fiscal rules has urgently returned to the EU agenda.

Criticism of the current system

The existing system is based on two general indicators: a permitted public debt level at 60% of GDP and a 3% threshold for the deficit in public finances. Additional criteria, interpretative rules and exceptions have been introduced through numerous changes since the pact was adopted in 1997. One of the most important of these is the so-called medium-term budgetary objective (MTO), which refers to a structural deficit ‘cleansed’ of the impact of cyclical fluctuations in the economy. It gives countries a little more leeway to increase spending during economic crises. The so-called 1/20 rule also plays an important role in enforcing fiscal stability. It stipulates that countries with excessive debt must reduce it each year by one-twentieth of the amount exceeding the reference level of 60% of GDP. Under the pact, countries that flout the rules may face the ‘excessive debt procedure’ (EDP) and sanctions (these are much tougher for eurozone members).

A resumption of this system would be inconvenient for almost all the stakeholders in the integration. Highly indebted countries such as Italy and Greece would have to quickly implement fiscal restrictions, which is difficult to imagine for political reasons. It would also be a problem for proponents of an investment drive in Europe, which is necessary due to the war in Ukraine, the energy crisis and the need to increase industry subsidies in response to the US Inflation Reduction Act (IRA). Nor would the countries that advocate tough fiscal policy be happy with a return to the previous rules. The pact came under fire for the extreme complexity of its rules, its opacity, the abundance of exceptions, and for the politicisation and unequal treatment of countries. The most glaring example of the latter was the European Commission’s refusal to get tougher on the French government’s budgetary policy in 2016 ‘because it is France’, in the words of President Jean-Claude Juncker. However, even the opening of infringement procedures means little in the current regime – no decisions on sanctions have been pushed through so far, as they require the consent of all the member states.

The European Commission’s proposal

The backdrop for the negotiations on the future of the SGP is formed partly by the conviction of all the stakeholders that it is necessary to simplify its rules and partly by the traditional dispute between the South, which calls for a shift away from the dogmatic debt reduction policies, and the North, which envisages a system that effectively enforces financial discipline.

The European Commission put forward a proposal to break the deadlock in November 2022. In essence, the idea is to move towards setting individual, medium-term debt reduction plans for member states. The governments would have four years to achieve a fiscal ‘path’, primarily a positive structural budget balance, to allow for gradual debt reduction. This period could be extended to seven years if countries submit plans for structural reforms and investments to help strengthen public finances. These proposals mean that the controversial 1/20 rule, which involves stringent fiscal constraints, would no longer apply. The rules for imposing sanctions are also set to change, as the previous, deterrence-based formula has proven to be ineffective. In any new formula, penalties would be less severe and thus politically easier to apply.

Sceptical Germans

Germany outlined its reform proposals back in August 2022. For finance minister Christian Lindner, the priority was to maintain the numerical fiscal stability criteria as the anchors of the system. However, he recognised the need to simplify and clarify the specific rules, and he also agreed to renegotiate the 1/20 rule. First of all, the new pact would need to make it easy to identify breaches of discipline and feature effective enforcement tools. Germany expected the reform to force EU member states to reduce their debt (which increased as a result of pandemic spending) and to build up financial buffers for future crises and investment challenges. Otherwise, the German finance ministry feared, there would be mounting pressure to launch further ‘recovery funds’ financed through common bonds.

Germany greeted the commission’s proposal with disappointment. It saw the shift from a rules-based system to individually negotiated paths as a fundamental problem. Indeed, the commission’s concept does not eliminate the problem of politicisation and the not entirely equal treatment of some member states by officials in Brussels. Despite the commission’s assurances that the methodology for creating paths will be uniform, in practice there is a high risk of legitimising the infamous ‘because it's France’ principle. Therefore, some German experts have started calling for the establishment of a separate, independent body, which at least in theory would be free of immediate political pressure, to assess the fiscal situation in the member states; an example of this could be a European Fiscal Council. Another point raised by Germany concerns the actual effectiveness of ‘individual paths’. It should be expected that at the end of the four-year (or possibly seven-year) transition periods, governments will try to negotiate additional time for the necessary adaptation measures in the area of public finances or secure watered-down assessments of their structural reforms.

The Northern bloc on the back foot?

Germany is not alone in its criticism of the European Commission’s ideas. The other northern countries, the Netherlands, Denmark, Austria and Finland, traditionally regarded as fiscal policy hawks, have voiced similar views. This time, however, it will be difficult to push through a different vision of reform for at least three reasons.

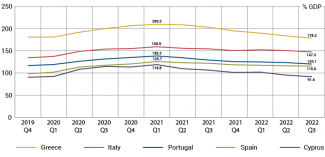

Firstly, the southern countries will point out in the negotiations that they have achieved debt reductions in real terms in recent quarters (see chart). This has come about mainly thanks to the post-pandemic GDP recovery, the resurgence of the tourism sector and, in particular, high inflation, which has reduced the debt-to-GDP ratio. This trend, even though its sustainability is doubtful, makes it impossible for the North to push its political narrative that it is necessary to make a rapid turnaround in fiscal policy and take action to reduce public debt.

Chart. Public sector debt levels in selected EU countries from Q4 2019 to Q3 2022

Source: Eurostat.

Secondly, the number one political topic in the European Union is the imperative to increase spending on the energy and technological transformation. This is intended as a response to Washington’s IRA plan and last year’s shock on the fuel markets. There is no doubt that it will be difficult to reconcile this idea with tougher rules in the pact. In this case, the South would argue (rightly so) that the only option is to transfer these expenses and investment commitments to the community level. It does not help Germany’s case that this issue will also be discussed at the European Council in March and will thus directly affect the course of negotiations on reforming the pact.

Thirdly, Germany and other EU fiscal hawks could previously count on the Central and Eastern European member states. In the past, the latter shared the belief that fiscal stability and low debt were important for the health of the European economy. However, their possible support for such fiscal reforms is in question today due to the Russian aggression against Ukraine. Many of them are planning sharp increases in defence spending, which will be difficult to reconcile with any increased fiscal discipline. Therefore, they may find common ground with the southern countries in the negotiations on reforming the pact and endorse the changes proposed by the European Commission.