The growing role of Ukraine on the Central European gas market

According to data from Ukrtranshaz, the operator of Ukraine’s underground storage facilities, the country has accumulated 27 bcm of gas in them as of 16 September, which is the largest volume in 10 years. According to the head of Naftogaz, Andriy Kobolev, the volume of the stored gas may reach 28 bcm before the heating season begins. In recent years, Ukraine had on average accumulated only around 17 bcm of gas by this time of year. The scale of involvement by foreign entities is another new phenomenon: about 30% of the fuel stored belongs to companies from third countries.

The Ukrainian gas storage system consists of twelve underground storage facilities with a total technical capacity of 30.9 bcm, five of which (with a total capacity of 25.3 bcm) are located along the EU border and the rest along the border with Russia. Currently, the facilities are full to 87.2% of capacity.

Commentary

- Until 2019, the storage tanks were usually filled to just over half their capacity before the heating season (which usually starts in mid-October and ends in mid-April; see Figure 1). Last year was exceptional as the management of Naftogaz, concerned that the transit of Russian gas might be suspended when the previous agreement with Gazprom expired, decided to accumulate a quantity of natural gas that would be sufficient for Ukraine to meet its needs over the winter. However, on 30 December 2019 Ukraine and Russia signed a new five-year transit agreement. In addition, gas consumption in Ukraine was lower than usual due to the mild winter: only 6 bcm of gas was withdrawn from storage, compared to 8.44 bcm in the previous year and 9.5 bcm in the 2017/18 season.

- The factors that contributed significantly to the accumulation of record gas stocks this year include the situation on the global gas market and the ongoing reforms to the gas sector in Ukraine. Since 2019 there has been an oversupply on the global and European gas market, exacerbated by the ongoing coronavirus pandemic. The decrease in demand and the high availability of pipeline and LNG gas have led to persistently low prices, and low demand often means it is more difficult to use all of the gas supplies contracted. On the other hand, the increasingly advanced reforms to the gas market in Ukraine, in many cases consistent with EU regulations (including the ongoing liberalisation of gas trading and changes to the rules of access to the transmission network), have increased its transparency and operational efficiency, and thus made it more attractive to external customers. Solutions have been introduced to simplify access to Ukrainian infrastructure (such as the implementation of virtual VIP interconnection points on the borders with Poland and Hungary), and to facilitate gas storage by non-residents under the so-called custom-free warehouse mode. This procedure exempts traders from taxes and customs duties on the stored fuel for a three-year period. Since the beginning of 2020, shorthaul services ( short-distance, point-to-point, discounted transmission services) have been introduced; these may be combined with the option of custom-free storage. Also this year, so-called virtual reverse flows became possible: from Poland since the start of the year, from Hungary and Slovakia in spring, and from Romania in August. Moreover, July saw the start of Ukrainian capacity auctions , organised in line with the EU law & calendar.

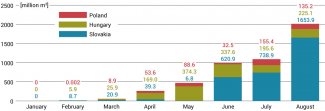

- The above-mentioned processes have led to greater demand for Ukrainian cross-border and storage capacities by EU gas market participants. From January to August this year, the Ukrainian operator OGTSU transmitted around 12 bcm of gas from Europe to Ukraine, an increase of 30% year-on-year. Up to 8.2 bcm of the imported gas was pumped into the storage facilities. As part of the total transmission, OGTSU transported almost 5 bcm of gas on a shorthaul basis, with significant increases visible since the spring. This service has been used by 26 entities, including 22 from abroad. The greatest interest in shorthaul service was for entry in Slovakia (3.1 bcm transported), followed by Hungary (1.3 bcm) and Poland (0.5 bcm). Just in August there were further significant increases (of 85% month-on-month) in shorthaul volumes, amounting to 2 bcm in that month alone (see Figure 2). In most cases, the short-distance transmission service has been combined with the storage of gas in Ukraine. The use of Ukrainian storage facilities in custom-free warehouse mode by foreign companies has risen significantly. Although European companies had already accumulated certain amounts of gas there (1.4 bcm stored by 31 foreign entities in August 2019) before the last heating season (2019/20), in fear of a possible Russian-Ukrainian gas conflict, the volumes stored are now much higher. As of 1 September, foreign entities have 7.9 bcm of gas stored in Ukraine under custom-free warehouse mode (including 4.9 bcm of the shorthaul volumes); this is 4.4 times more than in the corresponding period of the previous year.

- In addition, gas transmission to Ukraine has become easier thanks to the enabling of the virtual reverse gas flows. The greatest influence came from a temporary increase by the Slovak operator Eustream in the capacity available for reverse flows at the main border point in Veľké Kapušany. In March, when the Slovak-Ukrainian interconnection agreement was signed, Eustream made 10 mcm per day available for reverse flows, while from 1 July to 1 October it increased the capacities offered to as much as 60 mcm per day. This temporary increase was due to the ongoing maintenance works on the Ukrainian side of the pipeline near the Budince border point, which usually serves physical gas supplies from Slovakia to Ukraine. According to OGTSU, from January to August this year 38% of Ukrainian imports (around 4.7 bcm of gas) were transmitted in virtual reverse flow mode. This means that the fuel from Russia, bought by European companies, was collected directly in Ukraine and often pumped into storage tanks there. In September, all supplies of natural gas to Ukraine have been realised in backhaul mode, which means an important change to both the traditional path of gas supply to the country and the physical gas flows along the main transit route and border point with Slovakia. However this may change from October, if Eustream ceases to offer increased capacities for the virtual reverse flows to Ukraine.

- Reforms to the Ukrainian gas market and the implementation of solutions which make it more attractive are ongoing; these include the work which is underway to launch the Ukrainian gas exchange in cooperation with the Energy Community. This will further encourage Ukraine to take advantage of the current market situation to increase its role on the European (and especially the central European) gas market. The flows and trade in gas as well as the integration of the Ukrainian market with those of neighbouring countries is increasing, as a result of the increased use of Ukrainian infrastructure for regional needs, and the availability of new products and services. As a result, a new role for Ukraine, one not directly related to the transit of Russian gas, is being defined on the Central and East European gas map. The continuation of the current processes (including reforms to the Ukrainian gas sector), and good cross-border cooperation among the gas network operators (and other entities), will intensify the use of the regional infrastructure and the development of the gas trade – and thus the creation of gas hubs, both in Ukraine and more widely within Central Europe. However, maintaining the physical transit of Russian gas via Ukraine to Europe is still of essential importance if the changes taking place are to succeed.

Figure 1. Level of gas stocks in underground storage facilities in Ukraine in 2015–2020

Source: OGTSU.

Figure 2. Demand for Ukrainian shorthaul service in 2020

Source: OGTSU.