Stable stagnation: Hungary’s economic standing after 16 years of Orbán’s rule

After 16 years of uninterrupted rule by Viktor Orbán, Hungary is among the EU countries with the most distinctive political and economic model. Since 2010, the authorities in Budapest have consistently moved away from the liberal paradigm of transformation, declaring the construction of a ‘sovereign’ economy and a stronger role for the state in shaping development processes. In the second decade of the 21st century, Hungary stabilised its public finances, reduced unemployment, and accelerated growth under favourable global economic conditions and a high inflow of EU funds. At the same time, this model has from the outset been based on the selective redistribution of benefits, the privileging of economic elites loyal to the authorities, and the perpetuation of dependence on foreign capital and exports. In subsequent years, problems intensified, including low productivity among domestic enterprises and insufficient investment in human capital and innovation. The shocks that occurred after 2020 – the COVID-19 pandemic, Russia’s invasion of Ukraine, and the energy crisis – as well as the growing conflict with EU institutions, culminating in the suspension of a significant portion of EU funds, were not the source of these problems but rather sharply exposed pre-existing structural weaknesses.

The economic stagnation observed in recent years indicates that the model shaped during Orbán’s rule has exhausted its potential and has become a barrier to Hungary’s convergence with the economies of more developed EU member states.

The unorthodox economic policy of Fidesz: key assumptions

After Viktor Orbán came to power in 2010, Hungary was in a challenging macroeconomic situation as a result of the global financial crisis, which had pushed the economy into deep recession (in 2009, GDP fell by 6.8%). In 2008, in order to avoid default, the socialist government utilised a €20 billion assistance package provided by the International Monetary Fund (IMF) and the EU. The new government attributed responsibility for the poor state of public finances to its predecessors, while criticising the fiscal consolidation policy implemented in 2009, including cuts to social spending introduced by the then technocratic government. Orbán’s party, holding a constitutional majority in parliament together with the Christian Democrats (KDNP), sought to reshape the existing political and economic order.[1] The initial period of the Fidesz–KDNP coalition’s rule, which continues to this day, was marked by intensive reforms that did not, however, constitute a coherent development strategy and were often reactive in nature. The measures introduced are commonly referred to as ‘Orbánomics’, denoting an unorthodox economic policy characterised by a departure from dominant models and marked by numerous contradictions. Fidesz’s economic policy rests on the paradox of ‘socialism for the rich and capitalism for the poor’, as the main beneficiaries of these measures have been the upper middle class and economic elites aligned with the government.

At the outset of Fidesz’s rule, extensive fiscal reforms were introduced. The existing personal income tax rates (18% and 36%) were replaced with a single flat rate of 16% (reduced to 15% from 2016). Alongside this, the 16% corporate income tax was differentiated into two rates: 19% and a preferential 10% (which, from 2017, were replaced by a single corporate income tax rate of 9%, the lowest in the EU). To compensate for the decline in revenues from direct taxes, in 2012 the government increased the standard VAT rate from 25% to 27% (currently the highest in the EU)[2] and introduced a package of extraordinary sectoral taxes imposed primarily on banks and businesses operating in sectors dominated by foreign capital, such as energy, retail, and telecommunications. This policy was complemented by one-off measures, including the takeover of assets from private pension funds.

After 2010, the Orbán government set itself the goal of reducing the role of foreign capital in the economy.[3] The value of foreign direct investment (FDI) as a share of GDP showed a clear downward trend during the period of right-wing rule: falling from 76% in 2009 to 60% in 2022, representing the steepest decline in the region. Between 2004 and 2010, previous governments allocated a total of $612.2 million in subsidies for enterprises, of which nearly 98% went to international companies and only around 2% to domestic entities. In the period 2011–2018, the government more than doubled the scale of support for domestic businesses to approximately $1.3 billion, while increasing their share in the distribution of funds tenfold. This led to the strengthening of national capital in selected sectors regarded by the authorities as strategic from the perspective of political control – above all in the media, banking, and energy sectors. At the same time, the authorities sought to enhance the presence of manufacturing companies in Hungary, with which dozens of strategic cooperation agreements were concluded. Consequently, the country consolidated its position as a production hub for German automotive brands such as Audi, Mercedes, and BMW. Between 2010 and 2019, the value of automotive production in Hungary increased by 165% – mainly due to the expansion of companies with German capital – and the sector currently accounts for around 25% of the country’s exports.

The preferential treatment of domestic capital in selected service sectors constituting the institutional base of political power, combined with generous incentives for foreign capital in manufacturing, as well as the renationalisation of enterprises and administrative intervention in energy prices, point to a consistent strengthening of the role of the state in the economy. At the same time, this process has been accompanied by a growing politicisation of the economic sphere, most notably reflected in intensifying oligarchisation since 2010, characterised by the preferential treatment of enterprises linked to the governing camp. In practice, the Fidesz leadership has gained decisive influence over which entities could join the group of beneficiaries of state policy and take advantage of informal financial privileges. Public procurement has become a key mechanism for the accumulation of wealth by a business elite loyal to the government.[4] After 2010, the scale of corruption in this area increased markedly. A significant role was also played by the transfer of state assets through foundations and companies with opaque ownership structures, effectively linked to individuals from the inner circle of the governing party. Independent media has reported on numerous asset-related scandals involving elites close to the authorities. The clientelist system that has emerged in this way, based on the exchange of mutual benefits, has contributed to the consolidation of the government’s political support base.

Assessment of the 2010–2025 period: an overview of selected macroeconomic indicators

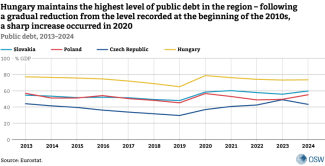

The economic conditions at the beginning of Fidesz’s rule, together with the subsequent improvement in the macroeconomic situation, created the framework for lasting changes in the conduct of economic policy. In 2009, before the right-wing coalition came to power, Hungary’s GDP fell by 6.8%, public debt reached 77% of GDP, and the unemployment rate exceeded 10%. Although Orbán assumed office after painful reforms agreed with the IMF, his policies once again undermined the confidence of financial markets and investors. When the Hungarian economy re-entered recession in 2012 (GDP declined by 1.7%), an adjustment to the adopted course was introduced, including, among other measures, an increase in the VAT rate and a reduction in social spending.

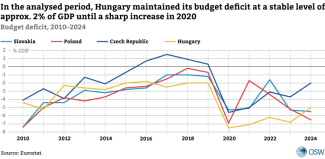

The Hungarian economy returned to a path of relatively sustained growth after 2012. The second half of the decade coincided with a global economic recovery, from which the countries of Central Europe benefited significantly. During this period, Hungary’s economy grew at an average annual rate of 2.7%, the balance of FDI inflows remained positive, employment increased markedly, and the level of poverty declined. Alongside this, public debt decreased from around 80% of GDP to 65%, while the budget deficit stood at approximately 2.6% of GDP. Meanwhile, despite periodic tensions in relations with Brussels, the inflow of EU funds remained stable; under the 2014–2020 financial framework, Hungary received around €22.5 billion.[5]

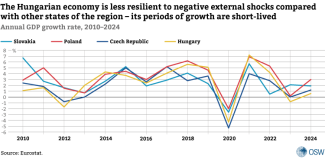

The several-year period of relative prosperity came to an end with the crisis triggered by the COVID-19 pandemic – in 2020, Hungary’s GDP fell by 4.3%. At the same time, the state of public finances deteriorated significantly: the budget deficit exceeded 7% of GDP, and public debt rose to nearly 80% of GDP, marking a departure from the previously maintained fiscal discipline. The short-lived post-pandemic recovery was not sustained – in 2023, GDP declined again by 0.8%, pushing the economy into a phase of stagnation amid falling investment and persistent external challenges, including limited access to EU funds. In 2023–2024, the Hungarian economy entered a technical recession twice – defined as a decline in GDP over at least two consecutive quarters. The slowdown was further deepened by the central bank’s restrictive monetary policy, aimed at curbing inflationary pressures. In 2024, GDP per capita in purchasing power parity terms reached 77% of the EU average – with only Slovakia, Latvia, Greece, and Bulgaria recording weaker results. Alongside this, the country had the lowest level of actual individual consumption per capita in the entire European Union (72% of the EU average, also in PPP terms). This indicates a limited redistribution of the benefits of economic growth to households and correlates with both persistently high inflation and the low share of wages in GDP.

The authorities had expected an economic rebound in 2025, particularly in the context of the parliamentary election scheduled for April 2026. However, data from January indicates that Hungary’s real GDP grew by only 0.3% year-on-year last year. This growth was constrained primarily by weak industrial output (which declined by 3.5% year-on-year in the first eleven months of 2025) and associated export performance, while the main drivers of economic activity remained the services sector and construction.

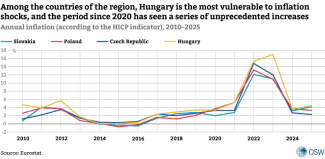

One of the key symptoms of the end of Hungary’s period of relative prosperity has been persistently high consumer inflation. As a result of expansionary fiscal and monetary policies even before 2020, price growth in Hungary had already exceeded levels recorded in most countries of the region. Following the outbreak of the COVID-19 pandemic and Russia’s invasion of Ukraine, this indicator reached unprecedented levels: in 2022, average annual inflation stood at 15.3%, rising to around 17% in 2023. Between September 2022 and November 2023, Hungary recorded the highest inflation rates in the EU every month. In 2024, there was a sharp decline in price dynamics to levels closer to those observed in other countries in the region. However, this adjustment was largely statistical and temporary in nature (resulting from a high base effect, falling commodity prices, and weakened consumption), rather than reflecting a structural improvement. At the same time, according to data for 2024, real wages increased by 8.9% year-on-year, meaning that wage growth outpaced consumer price inflation, partially offsetting the earlier decline in households’ purchasing power.

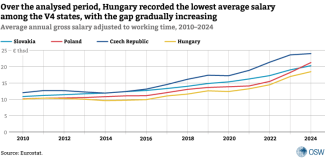

Hungary was the only country in the region to record a systematic decline in the share of wages in GDP during the second decade of the 21st century. Even in its latter half – the period of prosperity under Orbán’s rule – wage growth remained slower than in other countries in the region, a trend reinforced by the weak position of trade unions (with the share of employees belonging to a trade union at around 7%, one of the lowest rates in the EU). The country is also among those with the lowest earnings in the EU, both in terms of the minimum wage (€727) and average salaries. In 2024, the average annual gross wage amounted to €18,500, placing Hungary third from the bottom (ahead of only Bulgaria and Greece) and indicating a persistent income gap relative to the EU average, thereby confirming limited wage convergence.

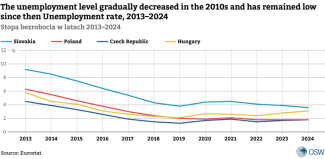

A notable achievement of Orbán’s economic policy has been the decline in unemployment, which fell from over 11% in 2010 to 5.8% in 2013 and reached as low as 2.1% in 2019. This was partly the result of a broad public works programme, which by the end of 2013 covered nearly 300,000 people. Since 2022, however, unemployment has been rising again, while labour productivity – adjusted for purchasing power parity – remains around 30% below the EU average.[6]

External challenges as catalysts of the crisis

Global developments after 2020 exposed the high vulnerability of Hungary’s economy under Orbán’s rule to external shocks and brought to an end the period of relatively stable growth observed in previous years. As during the global financial crisis of 2008–2009, the Hungarian economy experienced a deeper downturn than most countries in the region (including the Czech Republic and Slovakia, whose economies are of comparable size), pointing to its low resilience and suggesting the presence of significant internal factors that may amplify external shocks. In the government’s narrative, responsibility for the deterioration of economic conditions is attributed primarily to external factors such as the COVID-19 pandemic, the war in Ukraine, and the sanctions imposed on Russia. In reality, these developments have highlighted the structural limitations of Hungary’s growth model, which is based on inflows of foreign capital, exports, and an expansionary fiscal policy.

In response to the pandemic crisis, the government implemented strong fiscal stimulus measures, including broad transfer programmes, tax relief, and subsidies, which were maintained even after sanitary restrictions were lifted. At the same time, in 2021–2022, pre-election increases in public spending were introduced, which – under conditions of constrained supply – led to an ‘overheating’ of demand, particularly as wage growth and transfers were not aligned with productivity gains.

Russia’s full-scale invasion of Ukraine in 2022, in turn, led to a profound disruption of European energy markets and triggered an unprecedented surge in commodity prices. Hungary proved particularly vulnerable to these shocks due to its heavy dependence on Russian supplies and a decade-long policy of administratively suppressing energy prices. Consequently, in April 2022 Hungarian consumers paid approximately 60% less for electricity and 75% less for gas than the EU average. However, maintaining such low price levels was only possible through continuous state support: prior to the outbreak of the war, the subsidy programme cost the budget approximately 450 billion forints (around €1.17 billion) annually, while in 2022 its cost exceeded 1 trillion forints (approximately €2.6 billion).[7]

The tightening of monetary policy by the Hungarian National Bank further exacerbated the economic challenges of this period. In April 2022, the base rate stood at 5.4%, but under pressure from rapidly rising inflation, it was increased to 13% by July. Such a high level of interest rates was maintained for many months, significantly constraining investment and economic growth. By December 2024, the base rate had fallen to 6.5%, yet it remained among the highest in the EU. At the same time, the depreciation of the forint increased import costs (particularly for energy), reinforced inflationary pressures and forced the central bank to maintain a restrictive monetary policy, further limiting investment and domestic demand. While the depreciation of the forint brought short-term benefits to exporters, these had only a limited spillover effect on the domestic economy.

The external destabilising factors affecting the economy during this period were compounded by the freezing of EU funds for Hungary, which further significantly weakened its growth potential. For many years, the country had been among the largest net beneficiaries of the EU budget. In 2014–2020, it received the highest level of support from EU structural programmes in the region relative to GDP, averaging 3.2% annually. Under the new financial framework, Budapest could expect to receive around €22 billion from the Cohesion Fund and €5.8 billion from the Recovery and Resilience Facility (RRF), amounting in total to about 20% of GDP. However, in December 2022 the European Commission took the unprecedented decision to freeze EU funds under the conditionality mechanism, depriving Hungary of a key driver of growth. Despite the partial unfreezing of funds in 2023, approximately €8.4 billion from the Cohesion Fund and €9.5 billion from the RRF remain suspended, while part of the allocation has been irretrievably lost. In addition, financial penalties imposed by the Court of Justice of the EU have increased budgetary burdens. The problem is structural in nature and stems from a persistent conflict between Orbán’s model of governance and EU principles, thereby limiting the economy’s development potential. Attempts to compensate through financing from China – mainly in the form of loans – do not replace non-repayable EU grants and instead increase fiscal risks.

Entrenched structural problems

Hungary has consolidated a development model based on a strong dependence on foreign capital and on production characterised by low and medium value added. The country primarily serves as a manufacturing and assembly base for multinational corporations, and over the course of Orbán’s four consecutive terms in office there has been no significant reduction in the productivity gap between domestic and foreign-owned enterprises.

A real test of Hungary’s ability to escape the middle-income trap and achieve industrial upgrading would be the emergence of competitive domestic producers and exporters capable of competing on international markets. One of the main constraints in this regard is the fact that business functions within an oligarchic system, in which economic elites are not selected through open market competition but through political loyalty. Although domestic capital occupies a central place in Fidesz’s economic rhetoric, the adopted model has neither reversed the declining productivity trend of domestic enterprises nor reduced their structural subordination in export sectors. According to data from the Organisation for Economic Co-operation and Development (OECD), between 2010 and 2020 the share of domestic value added in Hungary’s gross exports hovered at around 50% and was among the lowest in the region (for comparison: around 60% in the Czech Republic and around 70% in Romania).

A particularly important role in Hungary’s exports is played by the automotive industry – including the production of components for electric vehicles – which has attracted the largest inflow of Western and Asian capital and currently accounts for approximately 8–9% of GDP. This high degree of sectoral concentration makes the entire economy excessively sensitive to fluctuations in a single industry, including to investment and demand cycles in Germany – Hungary’s main export market – as well as in the global automotive sector.[8] At the same time, the growing presence of Chinese manufacturers in the electromobility sector increases the economy’s vulnerability to the potential consequences of trade tensions between the EU and China. The dominance of the automotive sector, with assembly plants at its core, reinforces a model based on low labour costs, subsidies, and exports, rather than fostering diversification of the economic structure, innovation and the development of sustainable competitive advantages.

The systemic inability to move away from production with low and medium value added is also linked to chronic underinvestment in human capital and the dominance of a relatively low-skilled workforce. After 2010, Orbán’s government neglected areas crucial to a knowledge-based, high value-added growth model, particularly education and research & development. Already in 2010–2013, public spending on education was among the lowest in Central and Eastern Europe, and in the period 2014–2020 it declined further, fluctuating between 2.5% and 2.9% of GDP – well below the EU average. In 2020, Hungary was among the countries with the lowest expenditure on primary and secondary education in the EU: the EU average stood at 3.5% of GDP, while in Hungary it was only 2.1%. Higher education and research institutions also struggle with underfunding, brain drain, and increasing political control, which limits cooperation between academia and business. Spending on research and development (R&D) remains clearly below the EU average, amounting in recent years to around 1.5–1.7% of GDP, compared with approximately 2.2% in the EU. Moreover, its structure is highly polarised – a significant share of R&D activity is carried out by foreign industrial corporations in the automotive and electronics sectors, while domestic small and medium-sized enterprises remain only marginally involved.

Summary and outlook

After 16 years of Orbán’s rule, the Hungarian economy has entered a state of ‘stable stagnation’, losing its capacity to converge with more developed EU member states. The growth model based on inflows of foreign capital, exports, and low labour costs enabled periods of acceleration – particularly in the second half of the 2010s – but did not translate into structural modernisation or a lasting increase in the productivity of domestic enterprises. Fidesz’s unorthodox economic policy has favoured capital accumulation among higher social strata, selected segments of domestic capital and international industrial corporations, while limiting the redistribution of wealth towards households. This is partially offset by a generous pro-family policy, although it is to a large extent targeted at the middle class.[9] This has resulted in low wages, a declining share of labour income in GDP, and a persistent income gap relative to the EU average. The oligarchisation of the economy, a clientelist system of public procurement, and the politicisation of institutions have further weakened competition, innovation, and the country’s ability to move up global value chains. The government in Budapest had assumed that by obstructing EU decision-making it would force the unfreezing of funds, and that Donald Trump’s return to power would stabilise the global economic environment in a manner favourable to Hungary. Both of these assumptions have so far proved to be misguided.

Without sustained external support, the current growth model appears structurally unsustainable. The three major rating agencies – Moody’s, S&P, and Fitch Ratings – project a negative outlook for the Hungarian economy (as of December 2025), reflecting mounting fiscal, institutional, and political risks. At the same time, the economic downturn has opened up new political space for the opposition, rooted in a generational shift, driven by anti-corruption demands, and capitalising on growing economic frustration within society. Péter Magyar’s party – which seeks to dismantle the current political and economic system and restore access to frozen EU funds – now poses a real challenge to the ruling camp. Since the consolidation of the system after 2010, uncertainty about its durability has never been as high as on the eve of the April 2026 elections.

[1] A. Sadecki, In a state of necessity. How Orbán has changed Hungary, OSW, Warsaw 2014, osw.waw.pl.

[2] For some categories of goods and services the VAT rate is 5% and 18%.

[3] According to calculations by E. Voszka, between 1989 and 2008 Hungary attracted foreign direct investment totalling $60 billion, which represented the second-highest level of FDI per capita among the Visegrad Group countries (after the Czech Republic).

[4] D. Jancsics, A korrupció szociológiája – A kisstílű megvesztegetéstől a közpénzek ellopásáig Magyarországon, HVG könyvek, Budapest 2025.

[5] Cohesion Data. Hungary, European Commission, cohesiondata.ec.europa.eu.

[6] For an equivalent number of hours worked, the average Hungarian employee generates less than three quarters of the value added produced by the average worker in the EU.

[7] G. Scheiring, ‘Az orbanizmus kimerülése’, Új Egyenlőség, 14 November 2025, ujegyenloseg.hu.

[8] R. Stehrer, ‘How Trump’s new tariffs will impact the EU’s already struggling automotive industry’, The Vienna Institute for International Economic Studies, 1 April 2025, wiiw.ac.at.

[9] I. Gizińska, ‘Hungary’s ongoing demographic decline: an increase in birth rates is the only hope’, OSW Commentary, no. 658, 14 April 2025, osw.waw.pl.