Great ambitions: Russia expands on the LNG market

Expansion on the liquefied natural gas market has become one of the priority areas in Russia’s energy policy in recent years. This has been reflected in the statements made by government representatives and the many strategic documents that have been adopted recently. In particular, on 16 March this year the government approved a document entitled The Long-term Programme for the Development of Liquefied Natural Gas Production in the Russian Federationwhich envisages ambitious plans for further development in this area: an output of 80 to 140 million tonnes of LNG in 2035. The assumptions of the strategy fit in with the trend of regular increases in the production and export of Russian LNG which have been visible in recent years (from 11 to nearly 30 million tonnes in 2016–19). It can be concluded from these announcements that Russia is planning to increase its share in the global liquefied natural gas market to over 10%, and possibly even up to 20–30%. The expansion in this sector is also an argument for Moscow to strengthen its political and military presence in the Arctic. Increasing the Russian share on the European LNG market may also be a kind of remedy for Gazprom’s loss of influence in some EU countries.

Some projects, especially those planned by Novatek, have a good chance of being implemented, a result of not only the Kremlin’s political support but also of the administrative and financial support offered by the Russian authorities. This area of expansion may also become a new source of income for companies controlled by Russian oligarchs. However, the maximalist production and export plans are in fact quite unrealistic, considering the changes in demand, the intensified competition and the technological challenges, as well as the issues linked to the need to decarbonise LNG production.

The systemic growth of Russian LNG production and exports

Over the past five years, there has been a significant increase in the production capacity and the volume of exports of Russian LNG. Whereas at the end of 2016 there was only one large-scale gas liquefaction plant in Russia, the Sakhalin 2 project with a total production capacity of 10.8 million tonnes, towards the end of 2019 Russia’s LNG production potential almost tripled, reaching around 30 million tonnes.[1] In 2017–18, three production lines at Russia’s largest gas liquefaction plant were launched as part of the Yamal LNG project (16.5 million tonnes). In turn, the Novatek-controlled terminal in Vysotsk (0.7 million tonnes) was put into service in 2019.

The increase in production capacity has translated into an improved trade balance. Whereas exports of Russian liquefied natural gas reached around 11 million tonnes in 2016, this volume had risen to 29 million tonnes in 2019. This favourable trend also continued in 2020, despite the downturn on energy markets related to the decline in demand for raw materials due to the outbreak of the COVID-19 pandemic. Exports also slightly increased last year, from 29 to 30.3 million tonnes y/y.[2] At present, Yamal LNG (17.3 million tonnes) and the export terminal operating as part of the Sakhalin 2 project are the largest Russian LNG exporters. Gazprom has also increased its sales on the LNG market. Detailed data on the volumes and directions of Russian liquefied natural gas supplies are presented in Table 1.

LNG is gaining significance in Russia’s energy strategy

The development of LNG projects is an important element in the debate among the relevant authorities of the Russian Federation. For example, it was discussed by the presidential Commission for Strategic Development of the Fuel and Energy Sector and Environmental Security , which often takes strategic decisions regarding the Russian energy sector.[3] Issues concerning the LNG market have also been regularly discussed during government meetings, and as part of the activity of the Ministry of Energy.

Ambitious plans for the LNG sector are envisaged in the latest edition of the Energy Strategy of the Russian Federation to 2035, which was approved on 9 June 2020. Furthermore, the production and export of liquefied natural gas are among the main factors that are expected to contribute to the development of the Arctic, as confirmed by the Strategy for Developing the Russian Arctic Zone and Ensuring National Security until 2035, which was approved on 26 October 2020. For the first time in Russian history, strategic documents devoted strictly to the LNG industry were adopted in 2021. On 13 February, the government of the Russian Federation approved an Action Plan (Road Map) for the Development of the Small-Scale LNG and Gas Fuel Market in the Russian Federation until 2025.[4] In turn, the Long-term Programme for the Development of Liquefied Natural Gas Production in the Russian Federation was adopted on 16 March.[5] This extensive document (consisting of six parts and eight appendices) presents not only the detailed assumptions of Russian expansion onto the LNG market, but also the main factors stimulating the development of its potential in this area and the most important challenges, including those related to intensifying competition and technological limitations.

Ambitious plans

The Long-term Programme is further confirmation of Moscow’s ambitious long-term plans to expand onto the global LNG market. In the last few years, further increases in production and exports of this fuel have been announced by President Vladimir Putin,[6] the Ministry of Energy of the Russian Federation and local companies, in particular Novatek, the country’s second largest gas producer after Gazprom.

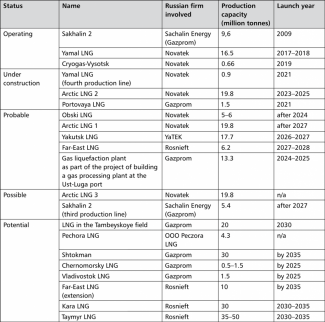

This document, which was approved on 16 March, assumes that Russia will systematically and rapidly increase its LNG production capacity: up to 46–65 million tonnes by 2024, 63–102.5 million tonnes in 2025–30, and 80–140 million tonnes in 2031–35. Moreover, the document states that an increase in sales of this fuel could raise the value of Russian exports by around US$150 billion. The programme includes a detailed presentation of the so-called large- and medium-scale LNG projects, which are divided into the following categories: 1) existing (27.66 million tonnes), 2) under implementation (21.3 million tonnes), 3) likely to be implemented (62–63 million tonnes), 4) possible to implement (25.2 million tonnes) and 5) potentially considered (131.3–147.3 million tonnes): a detailed list is presented in Table 2.

If the maximum level of liquefied natural gas production is reached, the Russian Federation’s share in LNG global market would grow significantly, from the present level of 8% to over 10% or even 20–30%. The Russian calculations are based on very optimistic assumptions presented by Russian and foreign expert centres. They envisage the very rapid development of the global LNG market over the next 10–15 years. The Long-term Programme presents a fairly wide range of values regarding the forecasts for an increase in global demand for LNG: it is expected to grow by 421 million tonnes (the lowest value) or even by as much as 718 million tonnes (the highest value). Russia also believes that the rapid increase in the capacity of regasification terminals worldwide (to around 920 million tonnes at the end of 2019) is an illustration of this positive trend.

The document does include detailed assumptions regarding the shares individual companies will hold in the Russian LNG market. However, if the planned projects are broken down into categories, it becomes clear that Novatek will remain the market leader. It can also be assumed that Gazprom will retain its privileged position in the segment of gas distribution and export via the pipeline system. This is because the programme stipulates that an increase in production and export potential in the sector should not lead to competition between Russian producers and exporters.

Factors contributing to the expansion

The fact that the Russian authorities will maintain the support mechanisms they already operate will help in the process of implementing some of the Russian LNG projects.[7] Based on existing practice and the assumptions of the strategic documents adopted, it can be concluded that fiscal instruments are an especially important element. Tax privileges (including a zero export duty rate and zero extraction tax rates for the projects implemented on the Gyda and Yamal peninsulas) and a number of other reliefs for entities offering services related to the implementation of LNG projects are planned. Another advantage is the raw material base. According to the document, the estimated gas resources total 73.1 trillion m3. The deposits in Western Siberia (mainly those located in the Yamalo-Nenets autonomous okrug), Eastern Siberia and the Arctic shelf will be the predominant sources of raw material for the planned projects. Another favourable factor is the fact that the production costs of Russian LNG are still relatively low. According to the assumptions made in the programme, the break-even point is estimated at US$3.7–7 per 1 MMBtu.

Another factor of strategic significance is the political support from the state, in particular from President Putin, who is still the most important decision-maker in key issues concerning the energy sector. Novatek owes its success primarily to the close social and political ties between its owners (Leonid Mikhelson and Gennady Timchenko)[8] and the Kremlin. These translate not only into the specific administrative and financial decisions made by state institutions, but also into making it easier to attract foreign investors: partners from China, France and Japan are involved in Novatek’s key projects. Another proof of the political support for the expansion of this company are the decisions regarding the expansion of its resource base on the Yamal Peninsula which have already been issued or are being planned.[9]

The construction of gas liquefaction plants may also turn out to be a new source of income for many of the Russian companies which usually win governmental contracts for the implementation of strategic projects because their owners have close relations with the Kremlin. Thus, the LNG projects may in a way serve as a continuation of the pipeline projects which have been completed or are near completion (including Nord Stream 1 and 2, TurkStream and Power of Siberia).

How Moscow benefits from developing LNG projects

Russia’s expansion on the LNG market offers it a chance to strengthen its leading position among the world’s natural gas exporters. So far, this status has been a consequence of the increase in sales of gas shipped by Gazprom through the pipeline system, primarily to Europe, including the former USSR and Turkey, as well as Asian countries (to Central Asia and, from December 2019, via the Power of Siberia gas pipeline to China). Additional LNG terminals will also make the Russian external gas policy more flexible, which is particularly important in the context of changes taking place on the global energy markets. Although the Long-term Programme indicates that Asian markets will be the main direction of the expansion, Europe is currently the key sales market (53.3% last year) for Russian LNG; the rest goes to buyers in Asia. The importance of the European market is especially visible in the case of the Yamal LNG gas liquefaction plant. Contrary to the original assumptions, according to which the project was primarily targeted at exporting gas to Asian countries, at present over 90% of its production goes to Europe (France, Belgium, Spain, the United Kingdom and the Netherlands).

Russia’s strengthening its share on the European (mainly EU) LNG market may also be a kind of compensation for Gazprom’s loss of influence in some countries. Whereas in 2016 Russian liquefied natural gas was exported only outside Europe, in 2019 and 2020 its shares on the EU market reached 19.6% and 20.2% respectively.[10] It is possible that the Kremlin hopes that the LNG supplied by Novatek (and also by other companies in the future) will be perceived differently in some European countries than the gas ‘contaminated by politicisation’ transported via Russian pipelines.

Most of the Russian LNG projects implemented both at present and in the future are located in the Arctic, which potentially creates opportunities for Moscow to strengthen its role in this region of the world. The need to increase the capacity of the so-called Northern Sea Route, which is expected to become an important route for transporting Russian energy resources, will certainly be one of the Kremlin’s arguments to intensify its political and military presence in the Arctic.

Besides, according to the Long-term Programme, developing the potential of liquefied natural gas production will also be important to a certain extent, considering the implementation of the country’s gasification programme (one of the government’s strategic projects) and its use as fuel in the transport sector. The forecast demand in these areas is not significant: 7.4–9.8 billion m3 for the needs of gasification, and about 5.5 million tonnes for transport by 2035. Therefore, the so-called small-scale projects will be used to achieve these goals.

The main challenges

Although some of the plans outlined in the strategy, in particular Novatek’s projects[11] such as Arctic LNG 2,[12] Obsky LNG and Arctic LNG 1, have a chance of being implemented, it is currently unlikely that the maximum assumed increase in liquefied natural gas production to 140 million tonnes in 2035 will be reached, for several reasons.

Firstly, it is difficult to predict at the current stage how many of the projects classified as probable, possible and potential will actually be implemented; and if so, on what scale and within what timeframe. While it is quite likely that Novatek will build new gas liquefaction plants, there are currently doubts about the prospects for the implementation of Gazprom or Rosneft’s ambitious LNG plans. Russia’s largest gas producer has not yet implemented any of its own large-scale LNG projects. This was partly due to Gazprom’s strategic priorities, which focused primarily on the implementation of pipeline projects, and partly due to political and market conditions. The suspension of the Shtokman LNG project (a plan to develop a field on the Russian continental shelf of the Barents Sea) in 2012 was a consequence of the downturn in potential markets, in particular in Europe and the US. The project to build a gas liquefaction plant in Vladivostok has also been significantly reconfigured (initially it was planned to build 3 production lines with a total capacity of 15 million tonnes, but now only a small-scale LNG plant with an annual potential of 1.5 million tonnes is planned). In turn, the plans to build a third production line as part of the Sakhalin 2 project have not been fulfilled mainly due to sanctions; the Yuzhno-Kirinskoye field, which was planned to be the resource base for LNG production, has been subjected to US restrictions. The withdrawal of Shell changed the plans for the Baltic LNG project in Leningrad oblast. In April 2019, Gazprom announced plans to build a large gas processing complex, including a gas liquefaction plant Its construction was officially inaugurated on 21 May 2021.

The prospects Rosneft has proposed for the implementation of its ambitious projects are even vaguer. Although Russia’s largest oil company announced plans to build a gas liquefaction plant in the Russian Far East nearly a decade ago (the Far Eastern LNG project, which is currently planned to be located near the De-Kastri port by the Japanese Sea), it is still in the design phase.

Secondly, the initial assumptions of the Russian strategy may have to be modified, given the high volatility of the global LNG market. Intensified competition among producers and exporters (Qatar, Australia, the US) and less optimistic than expected changes in demand may adversely affect the profitability of some Russian projects. Although the economic criterion is not always decisive when the Russian authorities make decisions regarding energy infrastructure investments, they may be forced to reduce their involvement in financing or co-financing large-scale LNG projects due to the decreasing revenues from the extraction and export of fossil fuels.

Thirdly, access to the technologies used in the construction of gas liquefaction plants may also become a challenge, which is also mentioned in the Long-term Programme. The document notes that the technologies used in all the ‘large-scale’ LNG terminals currently operating in Russia are those of Western companies: APCI, Linde, Shell and Air Liquide. Although the fourth production line as part of the Yamal LNG project will be based on Russian technology known as ‘Arctic Cascade’, it is not clear to what extent it can be used more widely in the next series of planned gas liquefaction plants.

Fourthly, the need to reduce greenhouse gas emissions (especially methane) in LNG production, resulting from regulatory changes in third countries, may also prove to be a challenge. So far, Russia has not made any intensive efforts to decarbonise its economy, including the energy sector, and the recently initiated pilot projects (including between Novatek and Siemens) may prove insufficient in the context of the regulatory solutions being prepared in the countries which are key markets for Russia. This applies in particular to the European Union, which plans to implement the relevant provisions on this issue as part of the European Green Deal concept announced in December 2019. The greatest challenge for Russia may turn out to be the so-called ‘Carbon Border Adjustment Mechanism’, i.e. plans to impose a duty or tax on the import of certain goods from countries with lower emission reduction requirements.

Forecast

The actions taken in recent years confirm that LNG projects will be one of the most promising areas for the development of the Russian energy sector over the coming decade. There are many indications that although Novatek will remain the leader of the Russian LNG market, Gazprom may also strengthen its position in this segment, mainly thanks to the construction of a large gas processing complex in the vicinity of the Ust-Luga port, which will include a gas liquefaction plant. It seems rather unrealistic to expect the maximum output envisaged in the strategy to be reached. However, there are numerous indications that over the next decade Russia will be able to increase its share in the global LNG market, mainly due to the Arctic LNG 2 project under construction and other projects by Novatek. It is also very likely that Moscow will strive to strengthen its position on the European LNG market. The price competitiveness of Russian gas, in particular its production costs which are still relatively low, may help it achieve this goal. Although it is difficult to expect that Russia will be ready to make systemic decisions regarding the decarbonisation of the energy sector at the moment, it is likely that Novatek, interested in further expansion in foreign markets, will engage in more pilot projects in this area in its co-operation with foreign partners.

APPENDIX

Table 1. Directions of Russian LNG exports in 2020

Marginal quantities of Russian LNG are also exported to Belarus, Latvia, the Czech Republic, Kazakhstan and Mongolia.

Source: author’s calculations based on data published by Interfax Energy.

Table 2. Russian LNG

Source: Распоряжение от 16 марта 2021 года № 640-р, op. cit.

[1] Taking into account large-scale (production capacity over 2 million tonnes annually), medium-scale (up to 2 million tonnes annually) and small-scale (up to 80,000 tonnes) terminals.

[2] It was worth US$7.56 billion, which means a 10.7% decrease y/y. The average price in Russian liquefied natural gas exports was US$162.5 per 1000 m3, i.e. around US$4.3 per MMBtu.

[3] A decision to liberalise the rules of gas exports with regard to LNG was passed in February 2013 during one of the first meetings of this commission. For more detail, see: S. Kardaś, ‘A feigned liberalisation. Russia is restricting Gazprom’s monopoly on exports’, OSW Commentary, no. 121, 26 November 2013, osw.waw.pl.

[4] Распоряжение от 13 февраля 2021 года №350-р, Russian Federation Government, government.ru.

[5] Распоряжение от 16 марта 2021 года №640-р, Russian Federation Government, government.ru.

[6] ‘Владимир Путин: «Рассчитываем к 2035 году выйти на уровень производства СПГ в 120–140 миллионов тонн в год»’, Ministry of Energy of the RussianFederation, 2 October 2019, minenergo.gov.ru.

[7] For more detail on the concrete forms of support provided to Novatek by the Russian government for the Yamal LNG and Arctic LNG 2 projects, see: S. Kardaś, ‘Expansion at the state’s expense: Novatek as a driving engine of the Russian LNG sector’, OSW Commentary, no. 275, 27 June 2018, osw.waw.pl.

[8] For more on the links between Timchenko and Putin, see for example: A. Luhn, ‘Gennady Timchenko denies Putin links made him one of Russia’s top oligarchs’, The Guardian, 21 March 2014, theguardian.com.

[9] According to media reports, President Putin backed Novatek’s applications for permits granting the right to develop the Neitinskoye and Arkticheskoye fields in the Yamal nature reserve. Furthermore, there are many indications that Putin has also given preliminary consent for the company to buy a group of the Tambeyskoye gas fields owned by Gazprom (resources located on the Yamal Peninsula are estimated at 7.3 trillion m3). See: ‘Путин поддержал предоставление НОВАТЭКу месторождений газа на Ямале’, Интерфакс, 28 April 2021, interfax.ru; Т. Дятел, Ю. Барсуков, ‘Игра на сжижение. НОВАТЭК хочет купить у «Газпрома» Тамбейское месторождение’, Коммерсантъ, 19 April 2021, kommersant.ru.

[10] These values have been calculated on the basis of data published by the International Gas Union as part of the annual World LNG Reports, available on the website igu.org.

[11] In addition to the gas liquefaction plants, Novatek is implementing two projects involving the construction of LNG reloading terminals in Murmansk and Kamchatka, with a reloading capacity of 21–22 million tonnes each. The infrastructure is planned to be put into operation in 2022–23.

[12] In April 2021, 20-year LNG supply contracts were concluded with all participants of the Arctic LNG 2 consortium. Furthermore, Novatek has announced that the investment is now around 40% ready.