Gas revolution? Prospects for increased gas production in Ukraine

For a number of months now the Ukrainian gas mining sector has been undergoing a major overhaul to improve the conditions in which it operates, with a view to significantly increasing production. The most important reforms include lowering tax rates and deregulation. These changes are a result of the government’s gas sector development plan for Ukraine, approved in 2016. Under this programme, the amount of gas extracted is to increase from the current 20 bcm to 27 bcm by as soon as 2020. Combined with greater energy efficiency, this would enable Ukraine to become self-sufficient in terms of its gas supply, and even to export gas in subsequent years. Because Ukraine has traditionally been dependent upon imports, and due to the political importance of gas-related issues, this course of events would be strategically important and have implications for energy relations in the entire region.

Government forecasts showing an increase in gas extraction in such a short time may not be very realistic, but it does seem likely that in the next few years production could reach a level rendering Ukraine independent of imports. Ukraine has large gas reserves of hitherto untapped potential (the third largest in Europe). Meanwhile, this development can only occur if reforms within the mining sector, a reduction in corruption, an influx of foreign investment, and political stability are all in place.

How much gas does Ukraine have?

When World War II came to an end, the Ukraine Soviet Socialist Republic was a major producer of gas, and at the beginning of the 1950s gas was even supplied from fields in Galicia to Moscow. In the mid-1970s, the level of extraction rose to a maximum of 68 bcm per year (approximately 12 bcm of this from western Ukraine), which was a quarter of the gas produced in the Soviet Union[1]. In the years that followed, production began to fall rapidly, however – to 42 bcm in the mid-1980s, and 28 bcm in 1990. This was mainly due to the potential of the fields in operation being used up, a low level of investment, a shortage of technology, and a rapid increase in extraction in Western Siberia, where the fields were larger, easier to access, and cheaper to operate. Over the last twenty years, gas production in Ukraine has remained constant at between 19 and 20 bcm per year.

Despite the downturn in domestic extraction, Ukraine has the third largest confirmed natural gas reserves in Europe (1.1 tcm), exceeded only by Russia (35 tcm) and Norway (1.8 tcm), and ahead of the Netherlands (700 bcm) and the United Kingdom (200 bcm)[2]. At the same time, when measured according to the international methodology, Ukraine’s gas deposits have increased by more than one third over the last decade.

The currently existing reserves mean that Ukraine can improve considerably on its production, which was 20.5 bcm in 2017. For the sake of comparison, the United Kingdom, which has deposits five times smaller, extracts more than twice as much gas per year (41.9 bcm), and the Netherlands extracts more than 80% more (36.6 bcm). Norway, on the other hand, produces six times as much (123.2 bcm), with reserves two thirds greater than Ukraine’s. The ratio of production to volume of deposits is approximately 17% of reserves per year for the United Kingdom, 6.5% for Norway, 5% for the Netherlands, and 2% for Ukraine. This illustrates the potential of Ukraine’s gas production sector. Also, Norway and the United Kingdom extract gas entirely from offshore fields, and the Netherlands extracts half from offshore fields, while a large portion of Ukraine’s deposits are located inland, rendering extraction less costly[3].

Ukraine’s natural gas reserves are estimated to be possibly even several times larger[4]. This applies in particular to unconventional gas (shale gas, coalbed methane, tight gas sands). Ukraine attempted shale gas prospecting and exploitation (under agreements with Shell and Chevron signed in 2013), but this was unsuccessful, and a return to this cannot be expected in the next years[5]. The Black Sea and Sea of Azov shelves are potentially rich in energy reserves, but promising tests could not be continued due to Russia’s annexing of the region (except for Odessa). As a result, projects to increase production from conventional inland fields will be the most promising over the next few years.

The structure of the gas mining sector

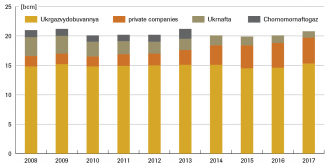

Almost 75% of Ukraine’s gas is extracted by the state-owned Ukrgazvydobuvannya (UGV), which is a subsidiary of Naftogaz. In recent years, it has maintained a production level of approximately 15 bcm. 20% of production comes from approximately 50 private gas companies (in reality only a few truly count), and the level of extraction has been increasing rapidly in recent years. While their total production in 2008 was 1.8 bcm, by 2017 it was 4.1 bcm. The major private firms are: Naftagazvydobuvannya (1.7 bcm), which is part of oligarch Rinat Akhmetov’s DTEK, and the Burisma Group (1.3 bcm), controlled by Mykola Zlochevsky, former minister of ecology and natural resources during Victor Yanukovych’s presidency[6]. These two companies collectively extract two thirds of gas produced by private firms. The other important companies include Ukrnaftaburinnya (0.4 bcm), controlled by oligarchs Ihor Kolomoysky and MP Vitaliy Chomotynnyk, Geo Alliance (0.25 bcm), owned by Victor Pinchuk and Vitol and also PNK (0.2 bcm), and UK company JKX Oil&Gas, in which Kolomoysky is the majority shareholder. This illustrates that a large majority of private gas companies are controlled by the oligarchs.

Diagram 1. Gas mining in Ukraine, 2008–2017

Source: Naftogaz, Ministry of Energy and the Coal Industry

Ukrnafta is also a major gas producer, in which 50% plus one share is owned by Naftogaz, and 42% by the Prywat Group, controlled by Ihor Kolomoysky and Henadiy Boholyubov, who de facto control the firm operationally. A lack of investment has caused the level of extraction by this company to fall quickly over recent years, from 3.2 bcm in 2008 to 1.3 bcm in 2017. Up until 2014, Naftogaz-owned Czornomornaftogaz was also an important producer, extracting approximately 1.7 bcm on the Black Sea shelf. Following the annexation of Crimea, however, Ukraine lost control over the firm and its assets. A considerable increase in production by private companies was able to offset the loss caused by the loss of control over Czornomornaftogaz.

As much as 80% of confirmed gas reserves are located in the Dnieper-Donets region (mainly in the Kharkov and Poltava provinces), where 90% of Ukraine’s gas is extracted. The remaining gas comes from the western part of the country (13%) and the Black Sea and Sea of Azov shelves (7%)[7].

Plans for increased gas production

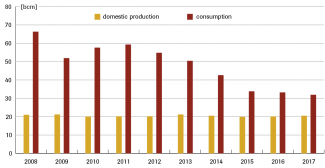

Ukraine’s chronic dependence on gas from Russia since 1991, which became a special kind of political challenge when the war with Russia broke out, led Kyiv to take measures to increase the level of domestic extraction. Successful diversification of Ukraine’s gas imports since November 2015 means that it does not need to buy from Gazprom, even though only a few years ago imports from Russia were between 35 and 40 bcm per year[8]. Reverse gas supplies from the West, however, are intended only as a step towards full independence.

Diagram 2. Gas consumption in Ukraine and domestic extraction, 2008–2017

Source: Naftogaz

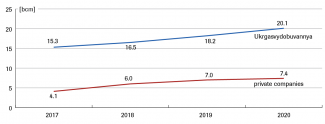

At the end of December 2016 the government adopted the gas sector development plan. The plan provides for an increase in Ukraine’s gas extraction to 27.6 bcm by the year 2020. When combined with a decrease in consumption, this is intended to enable gas independence and also, in the longer term, export of Ukrainian gas. The official document setting out the plan runs to no more than a few pages and only contains general information while failing to mention any specific measures to attain the envisaged targets. Ukraine’s energy strategy for up to 2035, adopted in August 2017, sets similar priorities.

According to the government’s plans, Ukrgazvydobuvannya would play the biggest part in this increase, extracting 20.1 bcm. UGV itself has adopted a document of its own, the 20/20 Strategy, and this confirms the government’s forecasts.

Diagram 3. Ukraine gas extraction forecast for up to 2020

Source: The government’s gas sector development plan for Ukraine of 28 December 2016.

When Oleg Prokhorenko took over management of UGV in 2015, an array of positive changes took place within the firm, one of the largest in Ukraine. Many mechanisms involving corruption, which had hampered the company’s growth for many years, were stopped. Among other things, the firm’s new president broke off all agreements with private companies that were extremely detrimental to UGV and effectively “drained” the company’s revenue[9]. This resulted in a significant improvement in its financial results, increasing annual profit from less than 20 million US dollars per year to around USD 450 mln in 2016 and USD 1.1 bn in 2017. At the same time, UGV’s investments went up from USD 200–250 million in 2015–2016 to USD 450 million in 2017, and almost USD 1 billion in 2018. Gas extraction rose from 14.5 bcm in 2015 to 15.3 bcm in 2017, the company’s highest level since 1993. In addition, the gas mining sector is one of the biggest contributors to Ukraine’s budget – in 2017 taxes from gas production companies came to approximately USD 2.7 billion, which is approximately 9% of budget revenue[10].

UGV plays a central role in the government’s gas self-sufficiency plan, as the company is expected to increase extraction by as much as 31%, to 7.4 bcm, by 2020. Over the same period, production by private companies needs to increase by 55% to 7.4 bcm. This would make it possible for Ukraine’s production to increase to 27.5 bcm, of which 5 bcm would have to come from new deposits (and 2.8 bcm of this would come from UGV), and the rest from old deposits, due to use of new technology[11].

Attempts at improving conditions in which the sector operates…

To achieve this ambitious government plan for a rapid increase in production, a number of major changes have been made over the last few months to improve the conditions in which the sector operates and to attract new investments.

On 8 December 2017, the Verkhovna Rada of Ukraine approved a new fiscal regime for the gas industry after more than two years of deliberations. The tax rate for new fields was reduced from 29% to 12% (for deposits of a depth of up to 5 km) and from 14% do 6% (for deposits below 5 km)[12]. In tandem with this, a guarantee was given that the new rates would remain in effect until 2023. This will make extraction more profitable and make Ukraine more attractive for foreign investors. Total investments worth an estimated USD 6 bn are needed to achieve extraction at a level of 27.6 bcm. However, the fields must be located in regions in which the transmission infrastructure is already in place, as this will reduce the costs of the entire investment.

Moreover, as early as December 2016, parliament decided that 5% of tax levied on gas and crude oil extraction would remain in local budgets, to help increase interest on the part of regions and local government authorities in developing production. According to estimates, in 2018 this would generate additional revenue of approximately USD 60 million[13].

On 1 March 2018, the parliament passed a deregulation act. This act will significantly speed up and simplify the permit procedure for extraction of raw materials. Some permits have been abolished, reducing the time needed to draft the necessary documentation from three years to 18 months. This means that the new fields will be exploitable more quickly.

…and the current problems

In spite of the positive developments outlined above, the changes that have already been made are not far-reaching enough to be considered a breakthrough in the way the Ukrainian gas mining industry operates. This would require, for instance, a thorough reform of the mining concession system. Over the last decade, 90% of concessions have been awarded without a competitive procedure and took place under opaque circumstances that facilitated bribery[14]. Many were awarded to oligarchical firms with links to politicians. Over the last two years, no mining licences have been awarded. This is incomprehensible in a situation in which the government has made a major increase in domestic extraction a strategic priority. The State Service of Geology and Natural Resources (Derzhgeonadra), which is responsible for issuing mining licences and providing geological data, also needs to be reformed.

The first international auction for 50 new mining concessions is scheduled to take place at the beginning of 2019. This will present an opportunity for international power sector companies, of which there are practically none in Ukraine at the moment, to enter Ukraine. If this does not happen it will be hard to anticipate an influx of capital and vital technologies, especially in order to revive the old fields and with respect to boreholes placed at great depths (65% of Ukraine gas deposits are located at a depth of more than 3 km).

It is also surprising how many problems the central and regional powers are causing for UGV. In mid-August a court froze the firm’s bank accounts due to a lawsuit filed by Karpatygaz, formerly a beneficiary under production separation agreements that were disadvantageous to UGV (this despite an award from a Swedish arbitration tribunal finding in favour of the state-owned company)[15]. Moreover, Derzhgeonadra repeatedly failed to renew UGV’s mining licences, causing extraction work stoppages. The Poltava and Kharkov province councils have not issued Ukraine’s largest gas company any new concessions for two years, even though over the same period 14 new licences were issued to firms that did not have any track record.

Prospects

Ukraine’s gas reserves mean that it can certainly increase gas extraction considerably and within a few years become a country that does not depend upon imports. Nevertheless, this implies that two requirements will have to be met. The first is increased energy efficiency and a decrease in consumption of approximately 15% from the current 32 bcm to 27 bcm. The second is continued improvement of the conditions in which the sector operates, so that the level of extraction can increase by a third. The changes that have been made up to now were adopted far too late and are still too limited for the principal target set in the government plan to be met, namely, gas independence.

The serious delay in implementing the document is confirmed by disappointing figures for the first half of 2018. UGV’s extraction level rose by a mere 0.8%, while that of private firms fell by 1%, despite forecasts that for the whole of this year production would increase by 7%[16]. This is a result of the expectation on the part of mining companies that the reforms would continue, but also of the current problems described above. It is clear at the same time that the changes approved in recent months have already led to increased investment activity. This is confirmed by record growth in maintenance services and the fact that in Q1 2018 the number of boreholes constructed by private firms went up by 80% on the same period last year[17], but it will be some time before this has any effect.

The greatest threat to continued development of the mining sector lies in Ukrainian politics, however. For many years, the gas sector was one of the main sources of corruption, and the process of rooting out such practices and bringing professionalism to the sector is extraordinarily difficult and time-consuming. This is particularly evident when examining the problems that UGV is facing. This is because effectively combating bribery in the sector and increasing transparency depends on successfully exploiting the potential of the Ukraine gas fields. If the political climate allows, from the technological point of view it is only a question of time before production increases. This will have an extremely positive effect, not only on the Ukrainian state and economy but also on the gas situation in this part of Europe.

[1] P. Högselius, Red Gas. Russia and the Origins of European Energy Dependence, New York 2013, pp. 20, 96.

[2] BP Statistical Review of World Energy 2018, https://www.bp.com/content/dam/bp/en/corporate/pdf/energy-economics/statistical-review/bp-stats-review-2018-full-report.pdf Under the gas sector development plan for Ukraine, the volume of confirmed gas reserves is 924 bcm, https://www.kmu.gov.ua/ua/npas/249766439

[3] Energy Policies Beyond IEA Countries: Ukraine 2012, IEA, Paris 2012, pp. 84, https://www.iea.org/publications/freepublications/publication/Ukraine2012_free.pdf

[4] IHS CERA estimates probable gas reserves at 2.8 tcm, and the Ukraine government estimates them to be 2.9–5.6 tcm. К. Маркевич, Тенденції та пріоритетні напрями розвитку вітчизняного газовидобутку, Razumkov Centre, 28.10.2015, http://old.razumkov.org.ua/upload/1446025738_file.pdf;

[5] For more detail see: M. Honchar, First steps into the unknown. The prospects of unconventional gas extraction in Ukraine, “ OSW Commentary”, 27.04.2013, https://www.osw.waw.pl/sites/default/files/commentary_106.pdf

[6] Aleksander Kwaśniewski became a member of the Burisma Group supervisory board in 2014.

[7] Golden Rules for a Golden Age of Gas: World Energy Outlook Special Report on Unconventional Gas, IEA, Paris 2012, s. 129–130, https://webstore.iea.org/weo-2012-special-report-golden-rules-for-a-golden-age-of-gas According to the IEA, the amount of unconventional gas mined in Ukraine in 2035 could reach 20 bcm.

[8] T. Iwański, S. Kardaś, From vassalisation to emancipation. Ukrainian-Russian gas co-operation has been revised, “ OSW Commentary”, 7.03.2018, https://www.osw.waw.pl/sites/default/files/commentary_263.pdf

[9] Ціна українського газу: як розвивати, добувати і продавати, Hromadske.ua, 26.12.2016,

[10] Добыча газа на Франковщине выросла вдвое, Espreso.tv, 7.07.2018, https://ru.espreso.tv/news/2018/07/07/dobycha_gaza_na_frankovschyne_vyrosla_vdvoe

[11] Gas sector development plan, https://www.kmu.gov.ua/ua/npas/249766439

[12] In 2014 the Verkhovna Rada of Ukraine raised the tax rate for mining gas from 14-29% to 29-55%, which was the highest rate in Europe. This was a surprising measure considering Ukraine’s situation with regard to energy. In January 2016 it was reduced to 14-29%.

[13] Р. Опимах, Как преодолеть последние препятствия на пути к газодобывающей революции, Epravda.com.ua, 6.03.2018, https://www.epravda.com.ua/rus/columns/2018/03/6/634743/

[14] У нас є всі передумови почати експортувати газ, Ukrinform, 12.02.2018, https://www.ukrinform.ua/rubric-economy/2400057-roman-opimah-vikonavcij-direktor-asociacii-gazodobuvnih-kompanij-ukraini.html

[15] Рахунки АТ «Укргазвидобування» арештовано, Ukrhazwydobuwannia, 20.08.201, http://ugv.com.ua/uk/page/rahunki-at-ukrgazvidobuvanna-arestovano The Ukraine media have reported that Karpatygaz is controlled among others by oligarchs Dmytro Firtash and Mykola Martynenko, an influential politician of the National Front, who is in the ruling coalition.

[16] В Украине застыла добыча нефти и газа, “Novoe Vremya”, 1.08.2018, https://biz.nv.ua/markets/v-ukraine-zastyla-dobycha-nefti-i-haza-2485732.html

[17] Без открытия геоинформации не будет нефтегазовых аукционов, AGPU, 12.06.2018, http://agpu.org.ua/ru/news/bez-otkrytiya-geoinformacii-ne-budet-neftegazovyh-aukcionov-opimah.htm