The OPAL pipeline: controversies about the rules for its use and the question of supply security

The record volumes of gas supplied via the OPAL and Nord Stream pipeline in recent weeks have been accompanied by controversy over the rules for utilisation of the OPAL pipeline’s capacity. There has long been uncertainty as to the actual content of the decision taken by the European Commission at the end of October 2016, the full text of which was published on 9 January 2017. Both the clash of interests between companies and states about how to use the gas pipeline, and the different interpretations of the impact of Gazprom’s increased utilisation of OPAL due to the new EC regulations on the situation on the gas markets in the EU, including in Central Europe and Poland, have been revealed. Uncertainty concerning the principles of the pipeline’s use has also been increased by Poland’s formal challenge of the EC’s decision.

The decisions by the European Court of Justice and a court in Düsseldorf related to this matter, which temporarily suspend the implementation of the EC’s regulations, have not yet been published. This deepens the doubts about the principles for increased utilisation of the OPAL pipeline, and about the legality of the increase in gas flows along the route which has been apparent since 22 December. At the same time, these gas flows are affecting the situation on the European (and especially Central European) gas markets. OPAL’s record fill-up translates to a record usage of the Nord Stream pipeline, as well as an increase in the role of Germany and the Czech Republic in the transit of Russian gas to the EU, especially to Central and Eastern Europe. This in turn affects the changes in gas flows in the Central European region, and reduces the transit role of Slovakia and Ukraine.

The increase in the utilisation of the OPAL pipeline, which changes the situation on the Central European gas markets , raises questions about how to increase these markets’ competitiveness and supply security. The controversies connected with the principles of using the pipeline reflect more substantial controversies within the EU concerning the key challenges and objectives of the EU’s security of gas supplies policy, in particular the role which should be played by Gazprom and deliveries of Russian gas, as well as the particular delivery routes. The EC’s interpretation of security of gas supplies visible in its October decision seems to be closer to the position of the supporters of normalisation, or even reinforcement of gas cooperation with Russia (by implementing the Nord Stream 2 pipeline, among others), despite the existing disputes at the political level, as well as of strengthening the role of Germany on the Central European gas market.

1. The legal situation

At the request of the German regulator BNetzA, and after years of negotiations, on 28 October 2016 the European Commission announced new rules for the use of the OPAL gas pipeline (see the Appendix; for more, see Agata Łoskot-Strachota, ‘The European Commission enables increased use of the OPAL pipeline by Gazprom’, OSW Commentary, 9 November 2016). The full text of the EC’s decision was only published on 9 January, which raised a series of questions about the publication procedure and transparency of the whole process, and about the details and consequences of the decision for the parties concerned, including actors from Poland and Ukraine. Even before the EC’s decision was published, the parties interested in how the pipeline was to be utilised had already taken a number of steps. On the one hand, on 28 November, the conditions of OPAL’s use were adapted to the EC’s new regulations by the pipeline operator, and on 19 December the first capacity auctions based on these rules were held (see below). On the other hand, the Polish gas company PGNiG and the Polish government applied to have the implementation of the EC’s decision halted, and challenged it at the European Court of Justice, deeming it a threat to the competitiveness and security of gas supplies to Poland and the whole of Central & Eastern Europe. PGNiG also lodged a complaint with a court in Düsseldorf, Germany. As a consequence, according to PGNiG’s statement, on 23 December the EU Court of Justice ordered a temporary halt to the implementation of the EC’s decision concerning OPAL, and requested additional clarification from the parties to the proceedings, i.e. PGNiG and the EC. After this is clarified, the Court is supposed to take a final decision as to the possibility of maintaining the suspension of the application of the EC decision until the plaintiff’s case has been considered. A week later, on 30 December, a similar decision was taken by the court in Düsseldorf, and the German regulator Bundesnetzagentur (BntezA) implemented it; this move should result in the temporary suspension of any further capacity auctions based on the new rules (see table in Annex).

The main confusion on the rules of use of OPAL’s capacity as of 19 December concerns currently the following issues:

· what were the legal bases for the use of OPAL’s capacity between 23 December (when the Court of Justice issued the temporary halt to the implementation of the EC’s decision) and 30 December (the date of the decision by the court in Düsseldorf and its implementation by BNetzA);

· whether, in accordance with the generally accepted standards, the proceedings at the court in Düsseldorf are to be consistent with the proceedings currently before the Court of Justice, and whether the German court’s final decision will be taken before or after the EU court’s final decision is issued;

· whether the Court of Justice’s decision means the suspension of the organisation of further auctions as of the moment of its issue, or whether it also affects the way in which the OPAL pipeline should be used from that date (at present OPAL is being used according to the new regulations, to almost its full capacity);

· how long the Court of Justice (and the German court) will maintain the (currently temporary) suspension of the implementation of the EC’s decision on OPAL.

2. Auctions and gas flows via OPAL

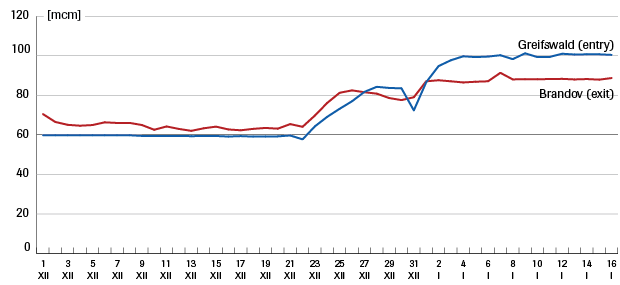

OPAL is a pipeline in which the capacity booked at the point of entry may vary from the capacity booked at the point of exit. This is because some of the gas from OPAL may be sold via Gaspool without any concrete points of exit being booked. In addition, OPAL has a physical connection with the Jagal and Ontras networks, and can thus transfer some gas in either direction. Consequently, in the case of OPAL, volumes of gas that enter the pipeline at Greifswald usually differ from those which exit at Brandov. In particular, until recently, due to the supplementary filling with gas flowing from the Gaspool area, it regularly occurred that more gas exited the pipeline at the Czech/German border than had entered it in northern Germany (see Appendix, Figure 1, for the period from 1 to 22 December).

Since 22 December, the increase in gas transfers via the OPAL pipeline has become clear (see Appendix, Figure 1):

- at the Greifswald entry point, from a daily average of 59.4 mcm during 1–22 December (the equivalent of 20.5 bcm annually), to levels sometimes in excess of 100 mcm per day (the equivalent of 34.6 bcm annually);

- at the Brandov exit point, from an average of 64.5 mcm per day during 1–22 December (the equivalent of 22.3 bcm annually), to levels sometimes in excess of 90 mcm/day (equivalent to 31.1 bcm annually).

Only on 31 December 2016 was a temporary decline in the pipeline’s use apparent.

Figure 1. The use of the OPAL gas pipeline (physical flows at the Greifswald entry point, and the exit point in Brandov) in December 2016 and January 2017

Authors’ calculations based on data from OPAL Gastransport GmbH & Co. KG

According to information from the pipeline operator OPAL Gastransport, on 19 December OPAL capacity auctions based on the rules adapted to the EC decision of 28 October 2016 were held at the PRISMA platform. The data from PRISMA shows that at 9 am on 19 December, new monthly products, most probably adapted to the new rules, were offered and sold:

a. at the Greifswald entry point, the operator OPAL Gastransport sold 12.66 GWh/h of the 15.86 GWh/h of the capacity available for the whole of January (the so-called Greifswald OPAL partly regulated);

b. at the Brandov exit point:

· the operators Net4Gas and OPAL Gastransport sold 2.63 GWh/h of the 5.83 GWh/h as part of the monthly bundled product (Brandov Opal bundle);

· OPAL Gastransport sold 100% of 10.03 GWh/h for the entire month (Brandov Opal partly regulated);

· according to reports from Energate, the operators Net4Gas and OPAL Gastransport also offered a bundled product corresponding to 10% of the pipeline capacity belonging to OPAL’s operator, although none of the 3.2 GWh/h was sold.

The capacities sold at Greifswald equal the sum of the capacities sold at Brandov, and come to around 28.5 mcm per day (and 10 bcm annually).

In the interpretation of the media and the energy market intelligence providers, all of the capacities sold were most likely bought by Gazprom. In connection with the suspension of the next auctions until the final judgement by the court in Düsseldorf on PGNiG’s complaint, and the lack of legal certainty as regards both the duration of the suspension and a final judgement on the complaints by the Polish side, it is not known whether the next auctions of the above-mentioned monthly products will take place in January/February. It is known that auctions at PRISMA of the same capacities are scheduled for 6 March 2017, but for a much longer period – most likely a period of 15 years (the maximum allowed by EU regulations), broken up into one-year pieces[1].

The capacities sold at auction on 19 December for the whole of January explain (leaving aside the current legal doubts) the rise in gas flows via OPAL as of 1 January. Consequently, the pipeline has seen record levels of usage, and the same is also true for the Nord Stream gas pipeline. According to media reports, in early January Gazprom supplied 165.2 mcm of gas per day via its Baltic Sea route, using more than 100% of the total technical capacity of the Nord Stream pipeline during 4-6 January.

The sharp drop in flows on 31 December was most likely because German regulator’s decision to stop the OPAL capacity auctions (see table in Appendix) had come into force on the previous day (30 December). Nevertheless, it is still unclear why the increase in flows on 22–30 December was just as sharply marked, and on what basis it took place (for example, whether it was connected with the use of capacities unused throughout the year on the basis of the old regulations, or with the daily auctions organised according to the new regulations).

3. OPAL and gas flows in Central Europe and Ukraine

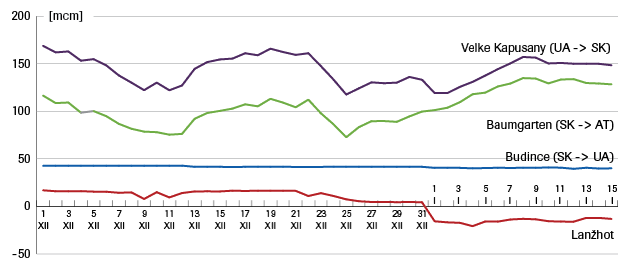

The increase in gas flows via the OPAL and Nord Stream pipelines has had a direct impact on the amounts and directions of gas transmission via other routes in Central & Eastern Europe. Above all, this has influenced the transit of gas via the Ukrainian route – a key alternative to the Nord Stream route for supplying Russian gas to Europe. The daily volume of gas transmission via Ukraine at the key border point in Veľké Kapušany (Slovakia) fell from around 160 mcm (22 December) to 117 mcm (25 December), a drop of over 25%, and then began to rise again (see Appendix, Figure 2).

Figure 2. Gas flows through key points of the Slovak network, in December 2016 and January 2017

Authors’ calculations based on data from Eustream

At the time of writing (16 January), the flows via Veľké Kapušany are lower by around 10 mcm per day from the level they stood at prior to the increase of flow via OPAL. At the same time, however, due to the low temperatures in Europe, it is likely this level is primarily related to greater demand for Russian gas and the lack of alternative opportunities for Gazprom to supply it, as the Russian company is already using Nord Stream’s maximum available capacity. If no additional capacities were made available in OPAL, transit via Ukraine would be significantly larger as this route has started to be used as the ‘last-resort option’. Similarly, there has been a temporary drop in gas supplies via Slovakia to Baumgarten in Austria. The most obvious change resulting from the increase in the use of OPAL, however, is visible in the flow of gas via the border point at Lanžhot between Slovakia and the Czech Republic; whereas before 22 December much more gas had flowed from Slovakia to the Czech Republic, at present the situation has reversed, and more gas is flowing from the Czech Republic to Slovakia (and probably onwards, to Baumgarten and other points).

It is thus clear that the immediate effect of the increased utilisation of OPAL is a strengthening of the role of not only Germany but also the Czech Republic in the transit of Russian gas, partially at Slovakia’s expense. In addition, the relative importance of Ukraine as a transit corridor for gas to the EU is decreasing. The Ukrainian route is increasingly being used as an option of last resort when demand for gas peaks and there is no access to alternative export routes.

At the same time, the larger deliveries via OPAL are associated with the greater availability of Russian gas in Germany (including at Gaspool) and in the Czech Republic, which may affect gas prices there.

The transit of gas via Slovakia to Ukraine (via Budince, which is currently the most important gas supply route onto the Ukrainian market) has seen only minimal declines. At the same time, however, the question remains open as to whether changes in routes, directions and volumes of gas flows from Russia in Central Europe may affect the availability and price competitiveness of EU gas supplies to Ukraine.

4. OPAL and the competitiveness and security of gas supplies to the EU

The changes already visible in the pattern of gas flows through Central & Eastern Europe show that increasing Gazprom’s access to OPAL and the possibility of it using the pipeline to a greater extent will affect the situation in gas markets around the region, in Germany, and indirectly throughout the EU. In addition to that the increase in Gazprom’s use of OPAL could have a significant effect on the Central European and Ukrainian gas markets, for the following reasons:

- the EC’s ongoing antitrust proceedings against Gazprom which is allegedly abusing its dominant position on the gas markets of Central & Eastern Europe;

- the EU’s ambitious foreign and gas policy objectives with regard to Ukraine, including the tripartite talks initiated annually by the EC aimed at ensuring the stability of gas supplies via Ukraine to the EU and to Ukraine itself.

Meanwhile, the justification of the EC’s decision primarily presents an assessment of how an increase in the use of OPAL will affect the security and competitiveness of supplies and the functioning of the market in the Czech Republic. In addition, although it admits the significant rise in Gazprom’s use of OPAL could have a negative effect on competition in the Czech Republic, the opinion expresses the hope that this will be mitigated by other positive effects of the new regulations for the pipeline[2]. The EC envisions a particularly substantial role here for the option (guaranteed by the EC’s decision) for third parties to reserve a minimum of 10% of OPAL’s capacity (via Gaspool). At the same time, at the first auction of OPAL’s capacities no interest was expressed in the OPAL capacities forecast for the third parties; it is uncertain whether such interest will arise in the future. Nor is it clear how, in such a situation, the EC intends to counterbalance the increasingly strong position of Gazprom in supplies to the Czech market.

The EC’s decision also de facto supports the development and importance of the role of Germany, and in particular the Gaspool market area, in the gas trade in both the EU and Central & Eastern Europe. In the opinion of the Commission, one of the beneficial effects of its decisions is the increased integration of the Czech market with the increasingly liquid Gaspool area. In this way, the EC’s decision has indirectly hampered further implementation of alternative projects for regional integration (such as the V4).

Allowing Gazprom to make greater use of OPAL indirectly ties the development of Gaspool to the boosting of Gazprom’s role in Germany and the region, as well as to larger supplies of gas from Russia (particularly in the context of declining production in the Netherlands and the North Sea). This partnership is reinforced by Germany’s already strong commitment to Gazprom (gas pipelines, storage facilities, gas trading etc.) and by plans to boost these ties even further (Nord Stream 2). However, the EC’s decision contains no analysis of the benefits and risks associated with such a link between the development of a key gas market in the EU with cooperation with the Russian-controlled gas company, the world’s largest – including any analysis of the effects on the German, regional and EU gas markets, and the impact on the shape and the independence of EU energy and foreign policy in this area. In support of its decision[3], meanwhile, the EC that the increased use of OPAL will lead to increased security of gas supplies to the EU, thanks among other factors to the availability of additional transfer capacities, irrespective of the apparent tendency by Nord Stream (and OPAL) to increase supplies at the expense of transit through Ukraine.

In consequence, the EC’s decision seems to make up part of one – but not the only – way of thinking on how to improve the security of gas supplies to the EU presented, among others, by gas companies and states (such as Germany) which support the implementation of the Nord Stream 2 gas pipeline. In this concept, larger imports of Russian gas are intended to guarantee the long-term stability and security of gas supplies, potentially low costs, and specific economic benefits for the states or companies involved in direct cooperation with Russia and Gazprom. Therefore, emphasis is placed on normalising the gas relationship with Russia, despite current misunderstandings at the political level (Ukraine, Syria).

Meanwhile, an alternative current of thought about supply security exists within the EU, one characteristic of Central European states (for example, Poland and Lithuania). In this way of thinking, significant dependence on gas imports from Russia (as shown by previous experiences, not only concerning supplies via Ukraine) is associated with the real risk of disruption; also, Russian gas might still be expensive, especially as long as Gazprom remains the dominant supplier. In this approach, it is noteworthy that gas markets do not operate in a vacuum, and fuel questions happen to be related to foreign and security policy issues. Those EU countries which consider supply security along these lines are cautious about reinforcing the gas relationship with Russia, especially in the context of the ongoing conflict in Ukraine; they see the diversification of supply sources and the reduction of dependence on Russian gas as priorities for supply security. The EC’s adoption in its decision on OPAL of a different interpretation of the key policy objectives of the security of gas supply in the region may consequently cause complaints that it is biased, which will shake trust in the EU’s institutions.

Agata Loskot-Strachota,

with assistance from Szymon Kardaś, Rafał Bajczuk

APPENDIX

Table. Legal documents regarding current rules for the OPAL gas pipeline’s capacity use

|

Documents |

Dates |

Basic points |

Unclear or unknown issues |

|

|

Issued |

Published |

|||

|

The European Commission’s decision on the principles of utilisation of OPAL’s capacity |

28 October 2016 |

9 January 2017 |

- alters the previously operational decision by the EC from July 2009 - establishes exemption from the third-party access (TPA) rule at 50% of pipeline’s ‘transit’ capacity - increases Gazprom’s access to the OPAL pipeline’s ‘transit’ capacity to as much as 90% - commits parties to hold auctions of capacity non-exempt from TPA regulation, - allows third parties access to a minimum of 10% of capacity (via Gaspool) - promotes greater integration of the Czech market with Gaspool and the German market |

|

|

Change in the four-way agreement between BNetzA, OPAL, Gazprom |

28 November 2016 |

|

- adjusts the four-way agreement from 11 May to the EC’s provisions of 28 October - forms the basis for changes to the terms of use of the OPAL pipeline by its operator, and for the start of auctions |

-the content of the four-way agreement (original |

|

PGNiG’s complaint |

4 December 2016 |

|

- complaint concerning the EC’s decision of 28 October, lodged by PGNiG Supply & Trading GmbH, operating on the German market; and a request for an immediate halt to its implementation - the allegations of a breach by the EC of the Treaty on the EU, the Treaty on the functioning of the EU, and Directive 2009/73/EC on the common principles of the internal gas market - according to PGNiG, the EC’s decision on OPAL is a challenge to market competitiveness and the security of gas supplies to Poland and Central & Eastern Europe |

-the exact wording of the complaint, including |

|

PGNiG complaint |

15 December 2016 |

|

- PGNiG and PGNiG Supply & Trading GmbH complain to the German court in Düsseldorf about the four-party agreement between BNetzA, OPAL, Gazprom and Gazprom Export, adapted to conform with the EC’s decision of 28 October, to exempt Gazprom from the principle of third-party access to OPAL - PGNiG lodges a complaint after BNetzA rejects its 4 proposals (to publish the text of the decision; to initiate a proper administrative procedure compatible with |

-no details of the complaint from PGNiG |

|

Polish government (foreign ministry)’s complaint |

16 December 2016 |

|

- call to suspend the decision - the EC’s decision threatens the diversification of sources and supply routes as well as the security of supplies to the EU, especially Central Europe and Poland, in connection with the increasing role of one source (Russia) and one supply route - Foreign Ministry also accuses the EC of violating principles of energy solidarity |

- no content of the complaint (a dispatch from the Polish Press Agency available on the Foreign Ministry’s website) |

|

Provisional decision by the Court of Justice of the European Union |

23 December 2016 |

|

-According to information provided by PGNiG, the Court decided to suspend the implementation of the EC’s decision of 28 October; at the same time it asked the EC to clarify the details of the auction of OPAL capacity, and asked PGNiG Supply & Trading to provide an in-depth analysis of the impact of the EC’s decision on the security and competitiveness of gas supplies to Poland

|

-The Court has not yet published the content of its decision |

|

Provisional decision of the court in Düsseldorf |

30 December 2016 |

|

-temporary halt to implementation of the new regulations concerning utilisation of the OPAL pipeline’s capacity (and by extension the holding of subsequent auctions) as of December 30 until a final decision is taken -most likely is a direct response to the complaint by PGNiG lodged in this court |

-not published -unclear how the proceedings in the Düsseldorf court are connected to the EU’s Court of Justice proceedings, and in particular, whether the court in Düsseldorf will suspend consideration of the case until the end of the proceedings conducted by the Court of Justice |

|

The decision of the German regulator BNetzA |

3 January 2017 |

10 January 2017 |

- in connection with the decision of the court in Düsseldorf of 30 December, resulting from the Court of Justice’s decision of 23 December, BNetzA has since 30 December temporarily banned the application of the EC’s decision of 28 October and the holding of subsequent auctions on OPAL’s capacity |

- which regulations for the auction of OPAL’s capacity have been in effect from the ECJ’s decision (23 December) until the decision of the court in Düsseldorf and its implementation

|

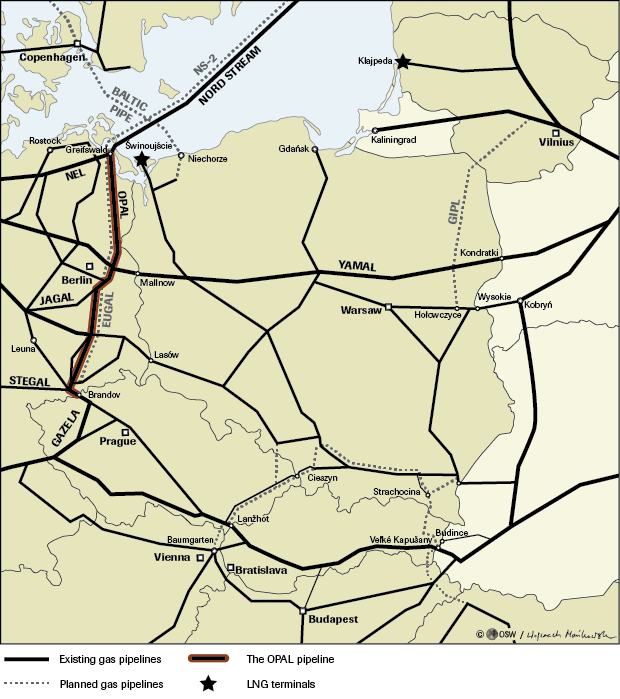

Map

[1] See Gasmarkt 1/17, H.Lochmann, energate, january 2017

[2] See 112-114, Comission Decision of 28.10.2016 on review of exemption of the Ostseepipelime-Anbindungsleitung from requirements of third party access and tariff regulation granted under Directive 2003/55/EC, Brussels 28.10.206, C(2016) 6950 final

[3] See 49-53, Comission Decision op.cit.