Suspension of LNG exports from Qatar – the spectre of another gas crisis

The US-Israeli attack on Iran and its regional repercussions have significantly affected global energy markets, most notably the gas market. On 2 March, Qatar, the world’s third-largest exporter of liquefied natural gas, announced a temporary suspension of LNG production; a day later, it also halted the production of selected downstream products, including urea, polymers, methanol, and aluminium. QatarEnergy LNG, the world’s largest producer of liquefied natural gas, declared force majeure and suspended shipments to its customers. The decision was triggered by Iranian drone strikes on energy infrastructure in the industrial cities of Mesaieed and Ras Laffan, which are key hubs for LNG production in the country. The de facto halt in tanker traffic through the Strait of Hormuz from 1 March also contributed to the declaration of force majeure.

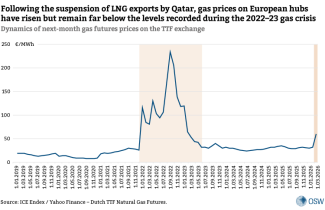

Qatar’s decision has led to sharp increases in gas prices for key customers in Asia and Europe. On the Dutch TTF exchange, prices on 3 March hovered around €55/MWh, 77% higher than the level recorded on Friday, 27 February, a day before the attack on Iran. The pace of increases is the fastest since the gas crisis of 2022–23, when prices peaked at €200/MWh. Prices have also risen on exchanges and in LNG contracts for Asian buyers based on baskets of oil products, which are also becoming more expensive as a result of the war in Iran.

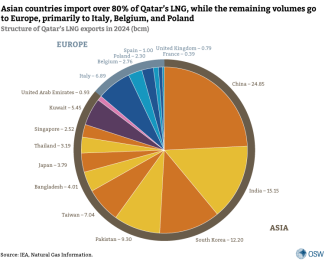

Qatar exports approximately 112–115 bcm of LNG annually, accounting for around 20% of all liquefied natural gas traded globally. A prolonged suspension of production would trigger a gas crisis, cause further price increases, require demand-side adjustments among the largest consumers in Asia and Europe, and aggravate their economic situation. Qatar’s pivotal role in global energy markets is also a key factor driving efforts to minimise the impact of the ongoing military operations in Iran on the production and transport of energy resources from the region, including steps to restore maritime traffic through the Strait of Hormuz.

Commentary

- In the short-term, a two- to three-day suspension of LNG deliveries from Qatar should not significantly affect global gas supply. Considerable volumes of gas remain on tankers outside the Strait of Hormuz, en route to their customers. Another factor mitigating the negative market effects is the end of winter and the onset of higher temperatures, which reduce demand for heating gas. Thus, the current price increases primarily stem from the risk of a prolonged absence of Qatari supplies from the market, a scenario that would have significant consequences given the scale of these deliveries. The market impact has also been amplified by other energy-related effects of the conflict: the suspension of LNG exports from the United Arab Emirates (around 7.5 bcm annually), Israel’s decision to halt production at some key gas fields and suspend exports to Egypt, as well as Iranian drone attacks on Saudi energy infrastructure and the likelihood of further strikes. The ongoing hostilities are multiplying the uncertainty and risks that have persisted in commodity markets since the outbreak of the full-scale war in Ukraine, particularly as they affect a region crucial for global supplies of LNG, oil, and petroleum products.

- The most severe negative effects of a de facto blockade of the Strait of Hormuz will affect Asian states, which receive 80% of Qatar’s LNG exports. In some of them, supplies from Qatar or the United Arab Emirates passing through the Strait of Hormuz account for the majority of LNG imports (about two-thirds in Bangladesh and India), or even all of them, as in Pakistan. Consequently, both diplomatic efforts by countries such as China and market adjustments were already under way. India began rationing gas supplies on the domestic market, including to industrial consumers, while Pakistan resumed domestic production and took emergency measures to diversify its gas sources. Prices of gas, derivative products (such as electricity), and gas substitutes, including coal, are all rising on Asian exchanges.

- In recent years, Europe’s dependence on Qatari LNG supplies has declined as imports from the United States have increased. In 2025, deliveries from Qatar accounted for only around 8% of LNG imports to the EU and less than 4% of the bloc’s total gas imports. Italy imports the largest volumes from Qatar (32% of its LNG mix), followed by Poland (25%) and Belgium (17%). Amid ongoing efforts to minimise imports from Russia, the EU has become heavily dependent on the global LNG market, both in terms of available volumes and prices. In addition, after a record-cold winter, the EU’s gas storage facilities are largely depleted, reducing its ability to use stored gas to mitigate price increases or, in the longer term, offset any potential shortages.

- A prolonged absence of Qatari LNG would trigger another global gas crisis and intensify price competition. This would drive up prices in other markets, including those for derivative products (such as electricity, fertilisers, and aluminium) and gas substitutes, notably coal. According to Goldman Sachs forecasts, if the suspension of gas production in Qatar lasts more than a month, gas prices in Europe could increase by as much as 130%. Deliveries from other sources, primarily the United States, could offset the loss of around 20% of global LNG supply only to a limited extent – according to emerging estimates, they could cover about one quarter of the annual shortfall. Consequently, it would be necessary to replace gas with alternative fuels or energy carriers and to implement demand-side measures. Moreover, the current price increases on exchanges have already exacerbated Europe’s problems associated with high energy prices.

- An LNG shortage could increase pressure from some countries to postpone the implementation of the EU regulation on phasing out gas imports from Russia, or even to partially resume supplies from that direction – both gas and oil. At the same time, in the event of such a shortage, European countries are likely to intensify discussions on restarting at least part of their domestic gas production (in countries such as Denmark, the Netherlands, and the United Kingdom) as well as on the possible removal of the link between gas and electricity prices on EU exchanges (the so-called merit order system). Calls to accelerate the energy transition and reduce imports of energy resources will clash with proposals to make the EU Emissions Trading System (ETS) more flexible in order to limit increases in emission allowance prices and their impact on energy prices.

- Despite some dependence on imports from Qatar, Poland is currently in a relatively favourable position. Its imports of Qatari gas are based on a long-term contract running until 2034 for the supply of 2.2–2.7 bcm annually (with some flexibility), equivalent to around 10–12% of Poland’s total gas consumption. The first two deliveries scheduled for March are already en route. LNG accounts for just under 40% of Poland’s gas demand. Besides Qatar, Poland imports LNG primarily from the United States, mainly under several long-term contracts concluded before the outbreak of the full-scale war in Ukraine. These prices are linked to the US Henry Hub benchmark, which is less exposed to the effects of the current crisis. In addition, more than 40% of the required gas is imported via the Baltic Pipe pipeline, primarily from Norway. The remainder comes from domestic production or from imports through interconnectors with neighbouring countries, including the Czech Republic, Lithuania, and Germany. Finally, Poland’s gas storage facilities are currently 51% full, compared with the EU average of 30%. Taken together, these factors should help mitigate the impact of the current disruption in Qatari supplies on the domestic market. At the same time, however, price increases on European and global exchanges will also affect the situation in Poland and on domestic exchanges. A prolonged disruption in Qatari deliveries would inevitably increase import costs, including the cost of refilling storage facilities, thereby leading to higher gas prices.

- Given the potentially serious consequences of the crisis for the economies of both the Gulf states and importers in Asia and Europe, efforts are already under way to resume the export of energy resources. All producers from the Gulf region have reportedly appealed to the United States to help guarantee the security of oil and gas production and exports. According to media reports, EU institutions and member states, as well as China’s Ministry of Foreign Affairs, have called on the parties involved to halt their military operations and avoid further escalation of tensions in order to ensure safe navigation through the Strait of Hormuz. At the same time, although the course of the war is difficult to manage, the United States likely shares the objective of quickly limiting the conflict’s impact on commodity markets, particularly the surge in global oil prices. Finally, Iran itself may have an interest in allowing shipping through the Strait of Hormuz to resume, as the waterway remains the country’s principal export route, including for its oil.