Gazprom: revenue slumps, debt rises

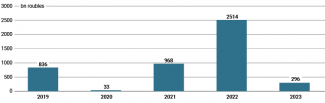

In late August, Gazprom published its financial report for the first half of this year. It gave the company’s net income as 296.2 billion roubles ($3.1 billion), an exceptionally low figure compared to the previous decade (excluding 2020, when the COVID-19 pandemic was raging). On a year-on-year basis, this drastic decrease is mainly due to the record revenues that were achieved in 2022, when Gazprom recorded a net income of 2.5 trillion roubles in the first half of the year due to unusually high gas prices. However, even when compared to the average receipts of more than 996 billion roubles in the first halves of 2018–2022, this year’s income plunged by around 70%.

The report also contains data on the company’s debt, which stands at more than 6 trillion roubles. This compares to 5 trillion roubles in the same period last year. According to Gazprom’s statement, this is a ‘comfortable’ level of debt because the company has sufficient liquidity to pay its short-term obligations on an ongoing basis.

Chart 1. Gazprom’s net income in H1 2019–2023

Source: Gazprom.

Commentary

- It is no surprise that Gazprom has reported such low earnings. The drop in its net income mainly stems from the loss of a significant part of its European market as a result of the political decision to reduce gas exports to the EU countries. In the first half of this year, about 12.6 bcm of gas was shipped to EU customers, a reduction of about 75% compared to the same period last year. According to estimates that take into account the current level of deliveries westwards, this year’s ‘lost’ volume may amount to c. 120 bcm compared to the volumes transported in 2021. Gazprom’s financial situation has also been adversely affected by higher fiscal burdens (including an additional extraction tax of 600 billion roubles per year that will apply in 2023–5), the implementation of a costly programme for infrastructure investments (including the gasification of Russian regions), as well as relatively low gas prices on the global market in the current year. In addition, the Russian government’s introduction of rouble settlements for gas sales to the so-called ‘unfriendly’ countries has reduced Gazprom’s access to foreign currencies and aggravated its financial situation. In the period discussed, the free cash flow ratio was negative, which means that the company’s potential for investment has decreased.

- Unlike 2020, when the Russian government stepped in to support Gazprom amidst the pandemic, we should not expect it to provide state aid to the company in the current situation, as it has consistently pursued a policy of balancing the budget at the expense of the oil and gas sector. However, the devaluation of the rouble has partly mitigated Gazprom’s difficulties. Moreover, the operations of Gazprom Neft, the company’s subsidiary that extracts and sells oil, have also helped to improve Gazprom’s financial indicators through the acquisition of foreign currency amid rising gas prices.

- The government is also trying to offset Gazprom’s falling export revenues at the expense of domestic consumers. In July this year, the Federal Antimonopoly Service (FAS) decided to raise wholesale gas tariffs for all categories of gas consumers in Russia. The charges will be increased twice: by 8% in July 2024 and by another 8% a year later. A similar hike of 8.5% was applied last December. According to the FSA, the funds from these spikes in tariffs will be allocated to investment programmes: the gasification of the country and the renovation of the existing transmission infrastructure. In addition, Gazprom is still calling for the relaxation of wholesale gas prices for industrial customers, which could provide another source of funding for the programme to upgrade the gas network. It is possible that if unsatisfactory financial results persist over the next few years, an even bigger portion of the costs of Gazprom’s investments, both those in Russia and those related to export connections, will be passed on to domestic consumers.

- Gazprom is unlikely to rebuild its position on the European market in the coming years due to infrastructural and political obstacles. These include the damage to both lines of Nord Stream 1 and one line of Nord Stream 2, as well as the unclear status of future shipments through Ukraine after the transit agreement that Gazprom and Ukraine’s Naftohaz concluded in 2019 expires in December 2024. Ukraine is clearly unwilling to enter into another long-term agreement on this issue. Finally, the sanctions against Russia currently make resuming transit through the Yamal–Europe gas pipeline impossible. Even if they are lifted, customers will probably not be interested in importing gas from Russia via this route. In this situation, the European branch of TurkStream, with a capacity of 15.75 bcm of gas per year, will offer a reliable overland export route to the EU from 2025 onwards. Officials from Gazprom and the Russian government seem to be aware of these challenges, as evidenced by their push to redirect supplies to the east.

- Gazprom and the Russian government have declared their intention to rebuild the company’s position by increasing its share on the Turkish and Asian markets. In 2022, Turkey became the main non-European market for Russian gas, with shipments totalling 21.6 bcm. At the same time, the government in Ankara has been promoting the idea of creating a ‘gas hub’ in Turkey (see ‘Turkey’s dream of a hub. Ankara’s wartime gas policy’) would be supplied by Russia, suggesting that Turkish imports of Russian gas could increase. The rising exports to China also attest to the redirection of Russian shipments eastwards. Transmission of gas through the Power of Siberia-1 pipeline has been gradually increasing, and this year’s shipments are expected to reach 22 bcm of gas, almost 7 bcm more than last year. In addition, Gazprom will start exporting gas to Uzbekistan in October this year (2.8 bcm per year) while leaving open the possibility of increasing this volume in the future. Russia has also signalled its desire to enter into a similar contract with Kazakhstan.

- However, in the coming years, exports beyond the EU will only allow Gazprom to partially cushion the drop in its revenues and avoid an even deeper reduction in its exports. It is questionable whether Gazprom will be able to fully restore its pre-war position by increasing its sales to Turkey and Asia due to the significant constraints that are already apparent today. Given Turkey’s well-developed import infrastructure and its contracts with many global suppliers, it is far from obvious that Russian supplies onto the Turkish market will steadily increase. Last year, Russian supplies to Turkey were 18% lower than in 2021, while between January and August this year they stood at more than 10 bcm (according to Vladimir Putin), down nearly 40% on the same period last year. In view of this reduction and the increase in exports to China, the latter may become Gazprom’s primary market as early as this year. Indeed, the existing connection via Power of Siberia-1 will make it possible to transport up to 38 bcm of gas per year from 2025, when this gas pipeline is set to reach its full capacity. However, it is impossible to increase exports to a level that would replace the lost European market with the gas-hungry Chinese market, even if the projects to build new connections are successfully completed as intended, which is by no means a foregone conclusion. A separate issue is China’s actual demand for Russian gas imports in the quantities reported by Russia, that is 98 bcm per year from 2030 onwards (see ‘The Power of Siberia-2 gas pipeline remains in the design stage’). Demand for large volumes of Russian gas among customers in Central Asia also remains uncertain. Moreover, Gazprom’s weakened negotiating position may also allow importers to negotiate attractive price formulas, which will further erode the company’s revenues.

- Constructing new connections to enable gas exports to Asia and Turkey will require substantial financial resources, which may be difficult to find in the context of the company’s shrinking revenues. This applies not only to China, but also to the other markets which Russia has portrayed as important for the redirection of its gas from west to east. Should Gazprom move forward with this concept, carrying out the necessary infrastructural projects would probably swell the entire group’s debt. If the financial indicators fail to improve, Gazprom could be forced to abandon one of the planned routes, while infrastructural constraints will make it impossible to transport enough gas to significantly improve the company’s financial standing. Gazprom’s officials have declared their intention to expand the company’s operations on the LNG market, which could become a source of additional revenue, but this will not materialise in the medium term due to infrastructural and technological obstacles.

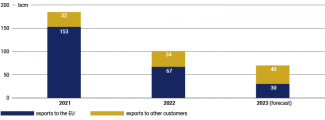

Chart 2. Gazprom’s exports to the so-called ‘far abroad’ (Europe excluding the Baltic states, plus Turkey and China) in 2021–2023

Source: the author’s own compilation based on data from Gazprom and the Bruegel think tank.