The transformation of agriculture in Ukraine: From collective farms to agroholdings

In recent years, Ukraine’s agriculture has been consistently improving and has been the only part of the country’s economy to buck the recession. According to preliminary estimates, in 2013 agricultural production increased by 13.7% - in contrast to a 4.7% decline in the industrial sector. According to official statistics, Ukraine’s industrial production was up 40% in the final months of 2013 when compared to the same period of 2012. This translated into an unexpected gain in fourth-quarter GDP growth (+3.7%) and prevented an annual drop in GDP. Crop production, and particularly the production of grain, hit a record high: in 2013, Ukraine produced 63 million tonnes of grain, outperforming its best ever harvest of 2011 (56.7 million tonnes). The value of Ukraine’s agricultural and food exports increased from US$4.3 billion in 2005 to US$17.9 billion in 2012, and currently accounts for a quarter of Ukraine’s total exports. Economic forecasts suggest that in the current marketing year (July 2013 - June 2014) Ukraine will sell more than 30 million tonnes of grain to foreign markets, making it the world's second biggest grain exporter, after the United States.

Ukraine’s government hopes that the growing agricultural production and booming exports will help the country overcome the recession which has been ongoing since mid-2012, and that the sector will become a driving force for sustained economic growth. However, the success of this plan is contingent on several factors: primarily, on the economic situation in Ukraine’s export markets, a better investment climate inside the country, as well as on future government policy, including the completion of an agrarian reform launched over 20 years ago. Despite pressing ahead with land ownership reform, the government has so far been reluctant to permit the free purchase and sale of agricultural land. Consequently, the growth of the agricultural sector has led to a concentration of production within very large agricultural holdings, known locally as agroholdings, characterised by large-scale intensive farming. The top one hundred holdings already control over 30% of all the land (6.7 million hectares) farmed by all agricultural companies operating in Ukraine (about 50,000 of them), corresponding to more than 16% of the total agricultural land in the country. This agricultural model has led to growing socio-economic disparities in Ukraine’s crisis-stricken countryside.

The significance of agriculture to Ukraine’s economy

Agriculture accounts for about 8% of Ukraine’s gross domestic product - a rate several times higher than among Europe’s major agricultural producers[1]. Its significance to the economy stems mainly from crop production, which accounted for nearly 67% of all domestic agricultural production in 2012. Despite showing signs of recovery from a severe crisis in the 1990s, animal production in Ukraine remains tied to small farms and is used largely for the personal consumption of the producers.

Ukraine has the second largest acreage of farmland in Europe (after Russia) with a total of 41.5 million hectares of agricultural land (about 70% of the total area of the country), of which arable land accounts for over 32 million hectares. Ukraine benefits from a favourable climate and good quality soils, of which about half are the highly fertile chernozem (or black earth). Ukraine is one of Europe’s leading grain producers: it is the continent’s largest producer and exporter of corn, the second largest producer of sunflower seeds and sunflower oil (and the world's largest exporter), as well as being a leading producer and exporter of wheat and barley (see Appendix 1).

Between 2005-2012, the export of food and agricultural products[2] increased by 315% (in 2013, Ukraine’s agricultural exports were worth an estimated US$17-18 billion). This makes agriculture Ukraine’s second most important export sector, after the country’s traditional export leader – the steel industry[3]. In the previous marketing year (July 2012 - June 2013), Ukraine exported about 23 million tonnes of grain; in the 2013/2014 marketing year, which started in July, Ukraine is planning to export 30-32 million tonnes of grain, which would break the 1991 record. In August of last year, the US Department of Agriculture estimated that with grain exports of over 30 million tonnes, Ukraine may become the world's second biggest grain exporter in the current marketing year (second only to the United States).

This year’s record high production and exports of food and agricultural products have become a driving force behind the “propaganda of success”, which the Kyiv government has actively engaged itself in to divert public opinion from the exceptionally poor overall performance of the Ukrainian economy. In fact, the record-breaking results are obscuring the grave problems that both this sector and the entire Ukrainian countryside have been facing for many years.

Post-1991 reforms: privatisation and land lease

After gaining independence, Ukraine entered a long-term agricultural crisis. The crisis was caused by the collapse of the centrally planned economy that had previously bankrolled a system of large and expensive programmes across the Soviet Union, but more broadly, also by the failure of the sector to adapt to the new economic reality[4]. Agricultural reform proved exceptionally difficult due to the lack of adequate market experience, insufficient capital investment, and the lack of a coherent vision for reform among the ruling elite.

One of the main objectives of the reform was to privatise Ukrainian land free of charge, under the “socially-correct” slogan: “Land for those who work it”. This was seen as the primary means to transform Ukraine’s rural areas and its agriculture. In the 1990s, Ukraine closed down nearly all 12,000 of its kolkhozes (collective farms) , whose assets were then placed under collective ownership of the newly created non-state businesses.

The employees of the former collective farms (about 7 million people, or more than 40% of Ukraine’s rural population) - most of whom subsequently found employment in the new, non-state businesses – were given a land share, or a so-called pai, on the land previously managed by the collective farms (an average of 4 hectares). In addition, over 7 million rural residents were granted ownership of small plots of land (up to 0.4 hectares) from the so called “Land Reserve Fund” and/or from the so-called “reserve land” (both owned by central or local government). The land was to be used for small-scale domestic farming (in total, approximately 2.6 million hectares). For many rural residents, this land has become their main source of income. However, unlike in the case of household plots, the allocation of land shares (or pais) within the reformed agricultural businesses (confirmed by official certificates) was not followed by an automatic right to physically claim the land - that is, the pais were not demarcated at specific locations and the farmers were not issued with title deeds to individual plots. Although this process began (with great difficulty) in the late 1990s, it was not until May 2003 that parliament passed a special bill regulating the question of land titles. By the end of 2012, title deeds had been issued to 6.4 million people (about 93% of the eligible population[5]). As a result, in late 2012 as much as 30.7 million hectares of agricultural land (or 74% of all agricultural land in Ukraine) was – nominally at least – in private ownership[6].

Initially, it was envisaged that the land privatisation process and agrarian reform would pave the way for the unrestricted purchase and sale of farmland in the country, but ongoing political disputes have led to the introduction of a series of temporary moratoriums on land sales, which are to remain in place until appropriate market conditions have been created in Ukraine. By “appropriate conditions” the policy makers meant the establishment of the necessary legal and institutional infrastructure, and especially land market legislation being passed and a cadastre being created. The government’s progress in this area, however, has been extremely slow.

The privatisation of farmland without the concomitant right to freely sell it, has contributed to the emergence of an agriculture based on land lease, which has been facilitated by the statutory authorisation to use pais as the subject of lease contracts. According to data from late 2012, half of all domestic agricultural land in Ukraine (49.8%) is under the management of about 50,000 businesses, operating mainly on leased land[7].

Until 2010, the average annual cost of leasing 1 hectare of agricultural land did not exceed the equivalent of US$40. More recently, however, lease fees have increased to around US$70[8] - this was caused by the government’s decision to raise the arbitrarily determined normative value of 1 hectare of farmland, and to increase the minimum land lease fee (to 3% of the land’s normative value). The low cost of land leasing (a fraction of the rates charged in the EU[9]), coupled with the possibility to use goods and services (often at inflated prices) in lease settlements, have facilitated the emergence of private and, most importantly, very large agricultural companies.

From kolkhozniks to farmers...

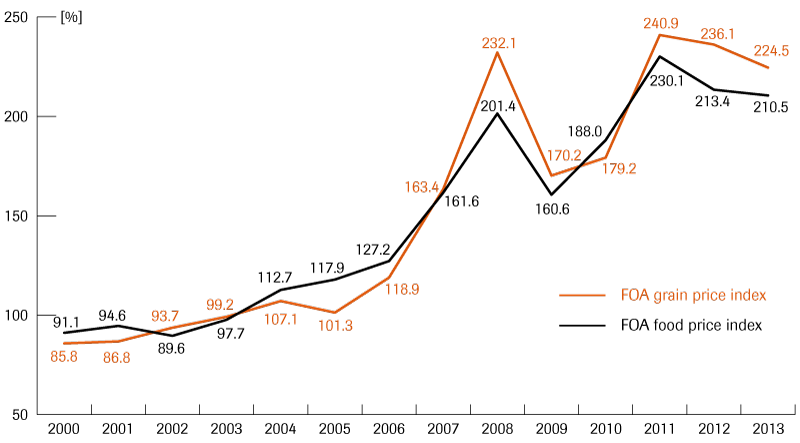

A period of economic growth from 2000 to 2008 (averaging about 7% of GDP per year) and low land lease rates and cheap labour (wages in agriculture are among the lowest in the economy) have improved the business conditions in the sector and the possibility of state support for Ukrainian agriculture. The most significant changes included: the introduction by parliament of the so-called “fixed agricultural tax”[10] in December 1998, VAT rebates, and state subsidies for agricultural production, which mainly benefitted the largest players[11]. The development of large-scale farms, however, was most directly facilitated by the increasingly appealing export opportunities. Since 2005, global markets have seen a systematic increase in the price of food and agricultural products (see Appendix 2); this has translated into higher prices for the main grains produced in Ukraine: wheat, barley and corn. Even after taking into account the interim (although admittedly, painful) price falls (2008-2009 crisis), by 2013 the price of the three main grains mentioned earlier had increased significantly: two-fold for wheat, two and a half times for barley, and three-fold for corn. Importantly, the global increase in grain prices was accompanied by growing demand generated mostly by developing countries[12].

Between 1996-2000, Ukraine’s total wheat exports reached 9.3 million tonnes - since 1991, wheat has been the main grain produced in the country. Over the next five years, this figure more than doubled (to 21.3 million tonnes) and between 2006-2010, Ukraine’s wheat exports rose by another 50%, to almost 33 million tonnes[13].

Initially, wheat exports from Ukraine were dominated by large global players, such as Toepfer, Cargill, and Serna. Thanks to the cooperation developed between international players and the local intermediaries in the supply chain, Ukraine saw the emergence of local players who gradually invested their profits in production, and began to export their produce themselves. Many of Ukraine’s largest agricultural companies started out as small-scale private farms, established back in the 1990s by the managers of former collective farms. They then quickly increased their size, especially in the last 5-8 years, mainly on the basis of leased agricultural land.

The development of private farms - which constitute the majority of all agricultural businesses established after 1991 (around 80%) and which operate an average area of about 100 hectares - began to slow down in the middle of the past decade. The number of such farms fell from 42,400 in 2005 to 40,700 in 2012. However, also this category of agricultural business shifted towards large-scale farming: at present 16.2% of the largest private farms manage 80% of all the land cultivated by this type of agricultural business (a total of about 4.4 million hectares).

... from farmers to large-scale land-managers

The process of consolidating agricultural companies through the merger and acquisition of smaller players (together with their land banks) has accelerated over the past few years. This consolidation allowed for the creation of a number of so-called “agroholdings”, which often operate in several parts of the country. The largest of them, UkrLandFarming, operates across an area of 670,000 hectares, making it the world’s eighth biggest agricultural holding (by land size)[14]. In terms of size, UkrLandFarming remains unmatched even by the largest agricultural companies in Russia - despite Russia’s unrestricted land market. UkrLandFarming is owned by 40-year-old Oleg Bakhmatyuk, who began his career in the late 1990s as a manager in Itera - a Russian intermediary company supplying gas to Ukraine and other CIS countries (for a few months in 2006, Bakhmatyuk became one of the vice-presidents of the state monopoly NAK Naftogaz of Ukraine). In early January 2014, the US agribusiness giant Cargill announced that it had purchased a 5% stake in UkrLandFarming for US$200 million, which put the market value of the entire Ukrainian holding at US$4 billion. Bakhmatyuk plans to increase the size of UkrLandFarming to 750,000-800,000 hectares, and to make his company one of the world's three largest agricultural giants within the next three years. This would raise UkrLandFarming’s total grain export capacity to 5-6 million tonnes[15].

In recent years, Ukraine’s agriculture has become sufficiently lucrative to attract the attention of some of the country’s biggest oligarchs. They have begun to notice that agriculture could offer them greater profit-making opportunities than Ukraine’s heavy industry and metallurgy - the two pillars of their business operations, which are currently suffering from the effects of the recession. Among the well-known Ukrainian oligarchs who already own large agricultural holdings are: Ihor Kolomoyskyi (120,000 hectares), Yuhym Zviahilsky - former acting Prime Minister of Ukraine, with close links to the current president (62,000 hectares), and Petro Poroshenko (96,000 hectares). Viktor Pinchuk has also expressed an interest in investing in agriculture, while Dmytro Firtash established the holding DF Agro in 2001, and has so far invested his money in the production of vegetables. In 2011, Rinat Akhmetov, Ukraine’s wealthiest businessman and one of the sponsors of the ruling Party of Regions, together with his business partner Vadim Novinsky, created HarvEast Holding. The company was formed on the basis of the agricultural assets of the Ilyich Iron and Steel Works (previously acquired by Akhmetov) and operates on nearly 200,000 hectares of land in Donetsk Oblast and in Crimea. Ukraine’s so-called “family”, an interest group linked mainly to Oleksandr Yanukovych, the son of the incumbent president of Ukraine has also made a foray into the agricultural sector. According to some sources, the “family” will enter the market through the recently established State Food and Grain Corporation of Ukraine, while they are expected to use the State Land Bank, established last year to help finance agricultural projects, as their delivery mechanism.

The vast majority of the local agricultural holdings continue to be controlled by Ukrainian investors. Due to the lack of a free land market, and due to restrictions on the acquisition of agricultural land, foreign investors have focused mainly on agricultural processing and on the trade in Ukrainian grain. The profit potential of Ukraine’s agricultural sector has also attracted passive foreign investors, who have been investing in shares in the Ukrainian agricultural companies listed on foreign stock exchanges. Owners of "traditional" agricultural holdings (without links to the industrial and financial groups run by local oligarchs who can generate income from other sectors of the economy) have found the issuing of shares abroad to be a convenient way to raise capital for further expansion in the domestic market. This has been particularly important since capital-raising opportunities in the domestic market are rather limited due to a poorly developed securities market in Ukraine and because of the high cost of borrowing. Obtaining business loans from local banks would be easier if local farmland could be used as collateral - this, however, remains a pipe dream due to the delayed introduction of a free land market[16].

The ten largest Ukrainian agricultural holdings currently control more than 3.1 million hectares of land, or more than 15% of Ukraine’s total farmland, which is cultivated by more than 50,000 businesses operating in the sector (see Appendix 3).

The never-ending reform, or the progressive collapse of the countryside

With growth as their primary objective, Ukraine’s agricultural holdings are often the only source of investment in rural areas. The investment is typically linked to production (human resources, technical infrastructure and logistics – grain handling terminals, granaries, etc.), but sometimes also to the construction of social and other rural infrastructure. These are often businesses whose owners have family links to particular towns and villages. For example, the controversial gas and chemical tycoon Dmytro Firtash has used his agricultural holding DF Agro to invest in his hometown of Synkiv, Ternopil Oblast, where he has constructed a large complex of greenhouses that will make the town one of the most cutting-edge vegetable producers in Europe. Meanwhile, Ivan Huta - a former chairman of a collective farm in his home village of Vasylkivtsi, Ternopil Oblast - has used his family farm to build one of the largest agricultural companies in Ukraine: Mriya Agro Holding (from 50 hectares of land in 1992 to almost 300,000 hectares today). Although the company is now managed from Kyiv, Mriya Agro Holding has kept its headquarters in Vasylkivtsi. The company has financed the construction of local roads, and – just like DF Agro in Synkiv - it has built schools and preschools. By doing so, the agroholdings significantly lighten the burden on the government in Ukraine’s rural areas, which have witnessed a dramatic decline in government funding since 1991.

Nonetheless, the activities of some of the agricultural holdings frequently boil down to the maximal use of resources within the term of the lease. This often leads to soil degradation and the devastation of local resources.

The rapid development of a new, narrow class of agricultural entrepreneurs, in times of the progressive impoverishment of the majority of Ukraine’s rural population, has exacerbated income inequalities and exposed what in effect is a re-feudalisation of social relations in the Ukrainian countryside. The rise of agribusiness has often led to the disenfranchisement of large numbers of the nominal land owners and has resulted in them becoming almost entirely dependent on the leaseholders. That is because the companies are often able to offer the impoverished pai owners not only a steady income but also the only possibility of local employment. Many residents - especially the elderly and the inexperienced, without sufficient financial resources or farming technology, unable to run a farm or uninterested in doing so - have been forced to lease their pais to agricultural entrepreneurs or to the owners of private farms[17]. Some studies suggest that up to 80% of pai owners agree to lease out their land, and many of them (32.3%) have never physically seen their pai[18].

The low prices of agricultural production[19], coupled with a crisis in all sectors of the economy after 1991, has markedly reduced the income of the rural population of Ukraine. Declining living standards and the rapid degradation of the countryside - for example, its technical and social infrastructure - has translated into a more pronounced demographic crisis than in urban areas. Between 1991-2013, the rural population of Ukraine decreased by as much as 15.9% (2.7 million people), while the population of urban areas declined by "only" 10.6% (3.7 million people). These figures represent the outcome of both negative population growth and large-scale migration to the cities, especially among young people looking for work. Over the past twenty years, more than 640 villages and hamlets have disappeared from the map of Ukraine[20].

The prospects for Ukraine’s agriculture

It was a common belief that after Viktor Yanukovych came to power in 2010, Ukraine would finally introduce a free land market and complete its land reform. The changes seemed likely because of the monopolisation of power the Yanukovych camp had and because the agrarian reform (including the introduction of a free land market) was part of the presidential reform programme for 2010-2014[21]. In addition, the parliament passed the cadastre bill and agreed to debate the controversial law on a free land market[22]. On 12 November 2012, however, the Verkhovna Rada (Ukraine’s parliament) extended the existing moratorium until at least 1 January 2016. Consequently, Ukraine has retained the current lease-based system for the development of agriculture. This will slow down any potential increase in investment in the sector, as business owners - who do not own the land they cultivate - are constrained by the investment horizon set by the term of their lease agreement. Under these conditions, long-term investment increases the risk of losing the very basis of the business, for example due to problems with lease renewal, which could be caused by hostile competitors trying to take over an existing business - a phenomenon that has become increasingly common in Ukraine in recent years.

Both the government and the owners of large agricultural estates in Ukraine were pinning their hopes on the prospect of signing the EU agreement on a Deep and Comprehensive Free Trade Area (DCFTA). Back in October of last year, Mykola Prysyazhnyuk, Ukraine’s Agriculture Minister, argued that the liberalisation of trade between Ukraine and the EU would allow for an immediate increase in agricultural exports to the EU markets, worth the equivalent of US$0.5 billion, which was particularly important because of Ukraine’s export-orientated agriculture. In reality, the agreement with the EU would not have created better export opportunities for Ukraine’s agricultural products, but could rather have increased investment in agriculture locally and accelerated the modernisation of the industry and this is essential if Ukrainian businesses are to compete against foreign companies on Ukraine’s slowly growing domestic market. Subsequently, however, the Ukrainian government announced that it would instead pursue closer cooperation with Russia and Kazakhstan[23] - Ukraine’s competitors in the global grain market.

In practice, however, Kyiv has been trying to develop closer links mainly with China. In October 2012, the State Food and Grain Corporation of Ukraine (SFGCU) and China National Complete Engineering Corporation (CCEC) signed a long-term contract for the export of Ukrainian grain to China. Under the agreement, the SFGCU received a US$1.5 billion loan from China’s Exim Bank (guaranteed by the Ukrainian government) for the purchase of grain from Ukrainian producers. The parties agreed that in the current marketing year (July 2013 - June 2014) the SFGCU would supply up to 4 million tonnes of grain to China (mainly, corn and wheat; although the preparations for the export of soybeans and barley are already underway). Next year, Ukraine’s grain exports to China are expected to rise to 6 million tonnes. Granting Ukraine unprecedented access to the Chinese market (as one of the very first grain exporters), as well as the scale of this cooperation, has translated into record growth in Ukraine’s grain exports in the current marketing year. Furthermore, due to the SFCGU-CNCEC deal, Ukraine will benefit from an increase in the import of Chinese technology and production (including, pesticides and fertilisers) and from potential investment. This, however, raises concerns about the long-term effects of this cooperation (which could, for example, displace the Western technologies and pesticides preferred by Ukrainian agroholdings). Finally, it seems that the Ukrainian mega-farms – which are being pressured into participating in the SFCGU’s Chinese projects - would prefer to establish their own export links with China[24].

This means that the agriculture industry is now forced to continue its current model of development, in which competitiveness is determined by low production costs (including lease fees and wages) instead of seeing the modernisation and efficiency improvements offered to Ukrainian agriculture by the DCFTA. Furthermore, Ukraine’s low output per hectare[25] will be compensated through economies of scale and extensive production; for example, of crops with a high rate of return, whose cultivation - coupled with short lease terms - will lead to a further degradation of soil.

The ambitions of the government and of the managers of large agricultural estates, combined with Kyiv’s need for foreign currency, are putting pressure on the sector to ensure rapid sales growth, without regard for the resulting costs (a decline in the price of exported produce and producers’ losses). Kyiv’s current priority is to make quantitative changes to the economy rather than qualitative, thus reinforcing the current model of development, which concentrates production within large-scale agricultural holdings.

Appendix 1. Ukraine’s agriculture in Europe and globally - selected produce

|

Type of produce |

Production volume |

Rank in Europe/ globally |

Export volume |

Rank in Europe/ globally |

|

Corn |

22.8 million tonnes |

Europe: 1 Globally: 7 |

7.8 million tonnes |

Europe: 1 Globally: 4 |

|

Wheat |

22.3 million tonnes |

Europe: 4 Globally: 11 |

4.1 million tonnes |

Europe: 4 Globally: 8 |

|

Barley |

9.1 million tonnes |

Europe: 3 Globally: 5 |

2.1 million tonnes |

Europe: 3 Globally: 5 |

|

Rye |

0.6 million tonnes |

Europe: 4 Globally: 4 |

|

Europe: Globally: |

|

Rapeseed |

1.4 million tonnes |

Europe: 4 Globally: 9 |

1.0 million tonnes |

Europe: 2 Globally: 4 |

|

Sunflower seeds |

8.7 million tonnes |

Europe: 2 Globally: 2 |

0.4 million tonnes |

Europe: 3 Globally: 3 |

|

Sunflower oil |

|

Europe: 2 |

2.7 million tonnes |

Europe: 1 Globally: 1 |

|

Potatoes |

24.2 million tonnes |

Europe: 2 Globally: 2 |

|

|

|

Sugar beets |

18.7 million tonnes |

Europe: 4 Globally: 5 |

|

|

Source: FAO [data for 2011]

Appendix 2. Global price indices for food and grain between 2000-2013 (%)

Appendix 3. The largest agricultural holdings in Ukraine

|

|

Name/ Abbreviation |

Owner/ Main shareholder |

Land bank (thousands hectares) |

Main business activity |

|

1. |

UkrLandFarming |

Oleg Bakhmatyuk |

670 |

Production and export of grains, meat, eggs and egg products, milk |

|

2. |

Kernel Holding |

Andrey Verevskiy |

422 |

Production and export of grains, sunflower oil |

|

3. |

NCH |

George Rohr, Moris Tabacinic |

400 |

Production of cereals, sunflower, soy, animal husbandry |

|

4. |

Myronivsky Hliboproduct |

Yuriy Kosiuk |

320 |

Breeding poultry, grains, meat products |

|

5. |

Mriya Agro Holding |

Ivan Huta |

298 |

Production of grains, sugar beets, potatoes |

|

6. |

Ukrainian Agrarian Investments |

Renaissance Group |

261 |

Production and export of grains |

|

7. |

Astarta |

Viktor Ivanchyk |

245 |

Production of sugar, grains, milk |

|

8. |

HarvEast |

Rinat Akhmetov (and Vadim Novinsky) |

197 |

Production of grains, feeds, seeds, dairy |

|

9. |

Agroton |

Yuri Zhuravlev |

151 |

Production of sunflowers, wheat, food, farming |

|

10. |

Sintal Agriculture |

Mykola Tolmachev |

150 |

Production of grains and sugar |

Source: latifundist.com

[1] And twice as high as in Russia or Poland, see: http://data.worldbank.org/indicator/NV.AGR.TOTL.ZS

[2] Four product groups: (1) farm animals and animal products, (2) products of plant origin, (3) animal and vegetable fats and oils, (4) ready food products.

[3] In 2012, Ukraine’s steel exports were worth US$18.9 billion and accounted for 27.5% of total exports.

[4] Livestock production was particularly badly affected. Between 1991-2012, the population of horned cattle decreased by over 81% (from 24.6 million to 4.6 million), pigs - by 61% (from 19.4 million to 7.6 million), sheep - by 86% (from 7.9 million to 1.1 million), poultry - by 13% (from 246 million to 214 million).

[5] http://land.gov.ua/zemleustrii-ta-okhorona-zemel/103703-derchzemagentstvo-za-2012-rik-v-ukrayyni-vydano-62-tys-derchavnyh-aktiv-vzamin-sertyfikativ.html

[6] Of which 27.1 million hectares was arable land (83.5% of all arable land in the country).

[7] 38.1% of Ukraine’s agricultural land is managed by family farms, 1.5% by other users, while 10.6% was made up of state owned so-called “reserve land” (not sold or granted for so-called “permanent use”). Source: www.ukrstat.gov.ua

[8] http://land.gov.ua/ru/component/news/?view=item&id=104013:tyzhnevyi-zvit-diialnosti-holovy-derzhavnoho-ahentstva-zemelnykh-resursiv-ukrainy-serhiia-tymchenka-1-4-kvitnia-2013-roku&catid=120:top-novyny

[9] Aгрохолдинги в україні: добре чи погано?, Німецько-Український Аграрний Діалог, Iнститут економiчних дослiджень та полiтичних консультацiй, Київ, серпень 2008, http://www.ier.com.ua/ua/publications/consultancy_work/?pid=1497

[10] The fixed agricultural tax affected those companies whose sales of agricultural products accounted for at least 75% of the total value of sales. The tax effectively reduced the fiscal burden on the companies, and several other taxes, including Corporate Income Tax.

[11] Aгрохолдинги в україні: добре чи погано?..., p. 7.

[12] L. Shavalyuk, “The Ukrainian Myth – the Breadbasket of the World”, The Ukrainian Week, 9 Sept 2013, http://ukrainianweek.com/Economics/88895

[13] I. Kobuta, O. Sikachyna, V. Zhygadlo, Wheat Export Economy in Ukraine, FAO Regional Office for Europe and Central Asia. Policy Studies on Rural Transition No. 2012-4, July 2012, p. 6.: http://www.fao.org/ fileadmin/user_upload/Europe/documents/Publications/Policy_Stdies/Ukrain_wheet_2012_en.pdf

[14] “China looks to Ukraine as demand for food rises”, Financial Times, 5 Nov 2013, http://www.ft.com/intl/cms/s/0/a9c0db18-4554-11e3-b98b-00144feabdc0.html#axzz2qgWmrumM

[16] Currently as many as seven Ukrainian agricultural companies are listed on the Warsaw Stock Exchange, including Ukraine’s leading “agro-holdings”, such as Kernel and Astarta Holding.

[17] For example, of the 4.6 million pai lease contracts signed in 2011, as many as 2.4 million (52.6%) were entered into by the owners of the pais - the rural pensioners. Source: A presentation by М. Кобець, Становлення ринку сільськогосподарських земель в Україні: зміни, тенденції та світовий досвід, Земельна Спілка України, Львів, 15 July 2011

[18] See http://zsu.org.ua/index.php/publikatsii-smi/9357-arendnye-otnosheniya-nuzhdayutsya-v-reformirovanii

[19] For example, between 1991-2001, the cost of agricultural production in Ukraine increased 6-fold, compared to a 17-20-fold increase in the price of industrial goods (the price of fertiliser, agricultural technologies and fuel has been rising rapidly) - see.: НАЦІОНАЛЬНА БЕЗПЕКА І ОБОРОНА № 1, 2012 ЦЕНТР РАЗУМКОВА, pp. 27, www.razumkov.org.ua/ukr/files/category_journal/NSD130_ukr.pdf

[20] This figure includes the 113 villages which have been merged with other villages or towns. At the beginning of 2013, there were 28,400 villages in Ukraine. Source: http://tyzhden.ua/News/77330

[22] It envisages, among other things, restricting the right to purchase land to Ukrainian citizens only, and capping transactions at a maximum of 100 hectares. These proposals have come under criticism from the market. The bill does not however contain an earlier proposal to introduce limits on the maximum acreage of leased land.

[23] For the past few years, Russia, Ukraine and Kazakhstan have been holding talks on the creation of a grain cartel, which could impact global agricultural trade.

[24] see http://korrespondent.net/business/economics/3206361-nakormyt-kytai-pekyn-prevraschaetsia-v-krupneisheho-potrebytelia-ukraynskoho-zerna

[25] This is higher on large farms, but has remained virtually unchanged for 20 years at the national level, and is currently half that in Western Europe.